- The Reserve Bank has hiked the cash rate to 2.5%, against our view. Consensus was mixed coming into the decision. And the wholesale rates market was about two thirds priced for a hike. But the rate hike was decidedly delivered by a unanimous RBNZ Committee.

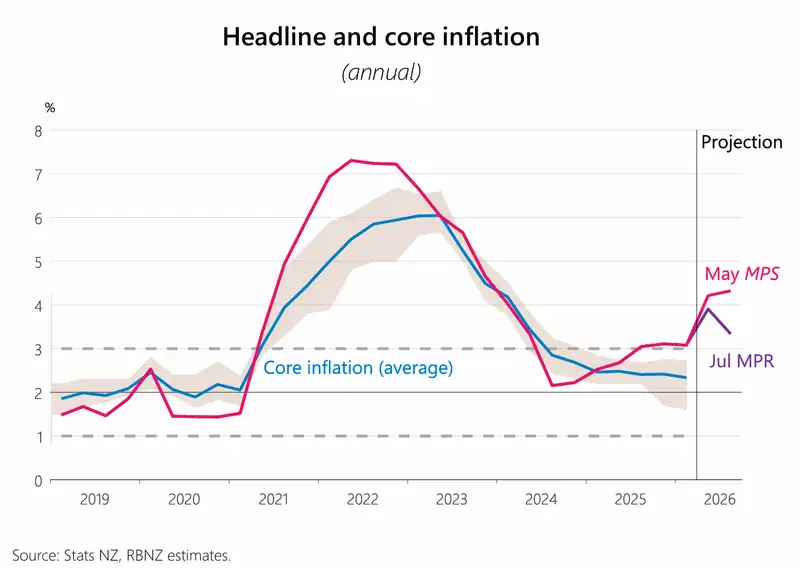

- The decision emphasised risks to medium term inflation, especially from second-round effects and price-setting behaviour. We disagree that the risks are to the upside. The medium-term outlook for inflation is already tame, with a weak labour market and uneven recovery.

- Stronger global growth also played a role in the Committee’s decision to hike now, rather than later. Ultimately, the risk is that the global economy is more resilient and will rebound faster than we expect.

- The Reserve Bank seems set on not taking a chance. We expect, but not want, another two hikes this year.

The Reserve Bank has increased the official cash rate by 25 basis points, to 2.5%. While we agree that a move up in interest rates was going to happen eventually, we disagree on the timing. Economists were mixed coming into the decision. But it was a rate hike that was decidedly delivered. The Monetary Policy Committee was unanimous.

In May, the Committee was divided 3:3, with external members voting for a rate hike. This time, the Committee reached a consensus. Four of six members were of the view that risks to medium term inflation are “broadly balanced”, and two saw risks as skewed to the upside. We disagree.

The accompanying statement emphasised the threat to medium term inflation, noting “Although energy prices have decreased, the effects of the shock will linger for some time and the outlook for medium-term inflation pressures remains uncertain.” And that’s where we differ. We argue the medium-term outlook for inflation is already tame, with a weak labour market on the other axis of the famous Bill Phillips’ curve.

The morning of the decision was full of volatility, with the US and Iran exchanging fresh fire in the Middle East. The two steps forward, one step back, pace of the conflict is wearing us down. The added uncertainty should have given the Committee more reason to pause. When the Committee decided to hold in May, it bought them time to see the sharp decline in oil prices.

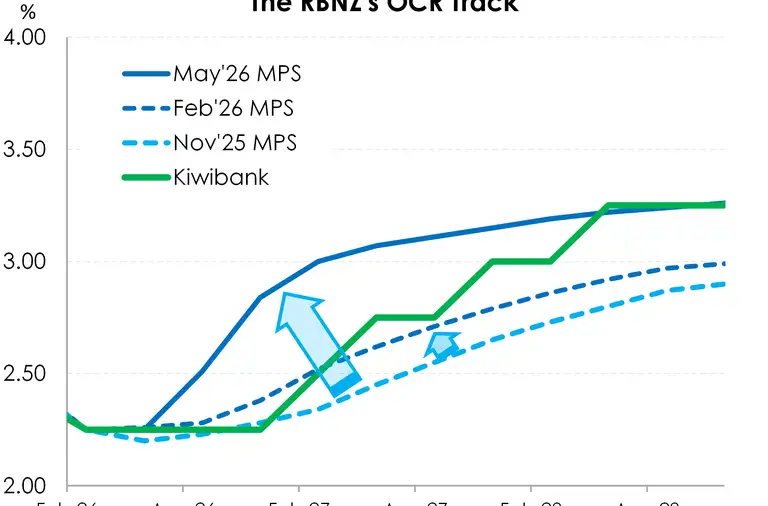

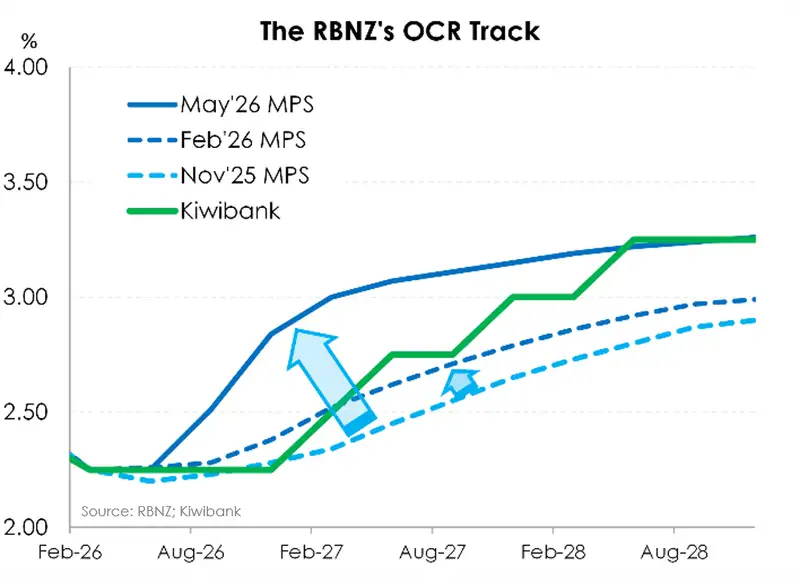

The OCR track presented in May, before the oil price plummeted, showed the cash rate heading to 3% by year end. BUT, pressures have eased. The RBNZ noted “The forecast for near-term inflation has declined, given that current oil futures pricing is now significantly lower than assumed in the May Statement… The lower forecast relative to the May Statement largely reflects smaller direct price effects due to lower oil prices, as well as reduced pass-through to other consumer prices”.

Leading up to the decision, the wholesale market was pricing in a hike as more likely than not, with 17bps of a possible 25bps (~68%) priced in. That moved up to 20bps (~80%) come midday on Wednesday.

But wholesale rates had decreased further out the curve. It’s important to note the recent fall in wholesale interest rates led to a slight fall in business lending rates and mortgage rates. That move played into the decision. The RBNZ was guarding against further falls. “The Committee noted that financial conditions had eased in recent weeks. This follows a material tightening in financial conditions earlier this year. Increasing the OCR at this meeting is intended, in part, to avoid an unwarranted further easing in financial conditions.” We expect the cash rate rise to reverse the recent fall in interest rates.

The influence of a weaker currency is one development that’s both a positive and negative. A weaker currency helps the affordability of our exports to the world. And at the same time, a weaker Kiwi dollar makes our imports more expensive – adding to inflation. One of our FX traders, Mieneke Perniskie, described the Kiwi as “a gingernut dunked in the tea too long”. To any foreign readers, that’s soft.

One of the bright spots in the announcement was the reference to stronger than expected global growth, thanks to a restoration in business and consumer confidence.

At this stage, we expect to see another two 25bp hikes by year end. There’s a desire to return policy to a neutral setting. We don’t know where that is… it’s guesstimated to be around 3%. But Prassana Gai is arguing it could be higher. A move to 3% looks most likely, but timing is still in the air.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.