“The Committee judges that the balance of risks is to the upside for inflation and to the downside for growth.” - RBNZ

- The RBNZ kept the cash rate on hold at 2.25%. But the RBNZ’s policymakers had a 3:3 split decision. Half the MPC, the external half, wanted a hike today. And, the trajectory for future rate rises was much more hawkish than we had expected.

- Rate hikes are coming sooner than we forecast. We now expect the RBNZ to start hiking in July, (not February ’27) as the MPC goes into July’s decision with a 50/50 split. There’s not a lot of data out between now and July to help either side of the split.

- “All Committee members agreed that increasing the OCR at upcoming meetings would likely be necessary to ensure higher near-term inflation does not feed through to higher medium-term inflation.” – RBNZ We disagree… but this is the view of the MPC. Rates have risen in anticipation of hikes, and rates will keep rising as hikes are delivered. Take the medicine now, which will hurt the patient, in order to keep them off the operating table.

Future inflationary pressures are dominating the discussions with the RBNZ. “Considerably higher cost pressures” are outweighing the downside risks to growth. And the bank looks set to hike to weaken already weakened demand through fear of the inflation beast reappearing.

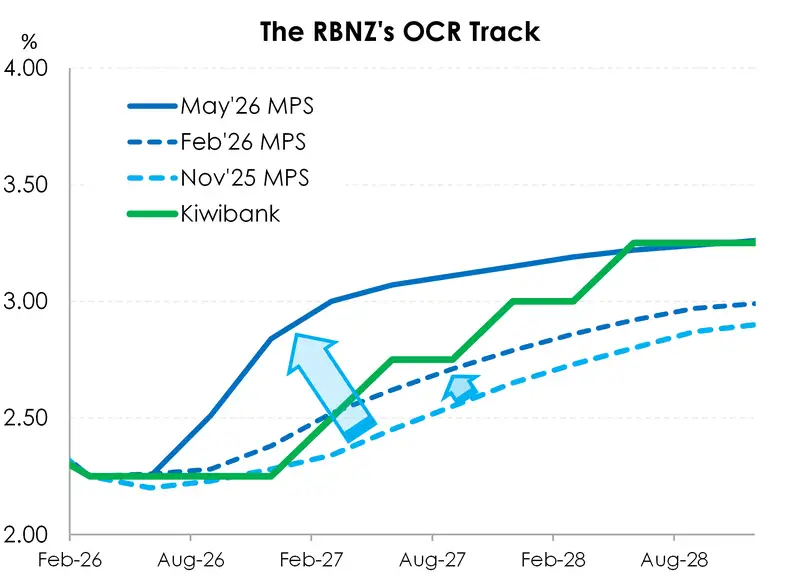

Everything comes out in the OCR track. And the OCR track was lifted nearly 50bps over the next year. It came off a low base, but has risen above our expectations. The end point of the track had another hike thrown in there for good measure, from 3% to 3.25%. As a result, we have to say what we think the RBNZ will do (hike ‘til it hurts)… not what we think they should do (pause to assess). The RBNZ’s decision in July starts at a 50/50 split (from today). The data out between now and July is likely to be inconclusive at best. But it’s another step towards agreed rate hikes.

September’s MPS decision is pretty much a done deal. Of the three scenarios presented by the RBNZ, there were two to the upside (twice the risk), and only one to the downside (there are obviously many paths possible).

“We will see average mortgage rates going up in coming months”- Anna Breman

Given the balance of probabilities, above and below the central trajectory, the RBNZ are more wary of persistent inflation than weak growth. Again, we disagree with the balance of risks. But we must play the institution, not the ball.

Our first chart highlights the shift in the RBNZ’s OCR track, compared to our old forecast, and prior RBNZ statements. It’s the bulge at the end of the year that surprised. We end up at the same place, but the RBNZ now gets there much sooner.

We believe the RBNZ is risking a lot to gain a little. Our analysis and liaison with businesses suggest much more subdued price setting behaviour, and deeper demand destruction.

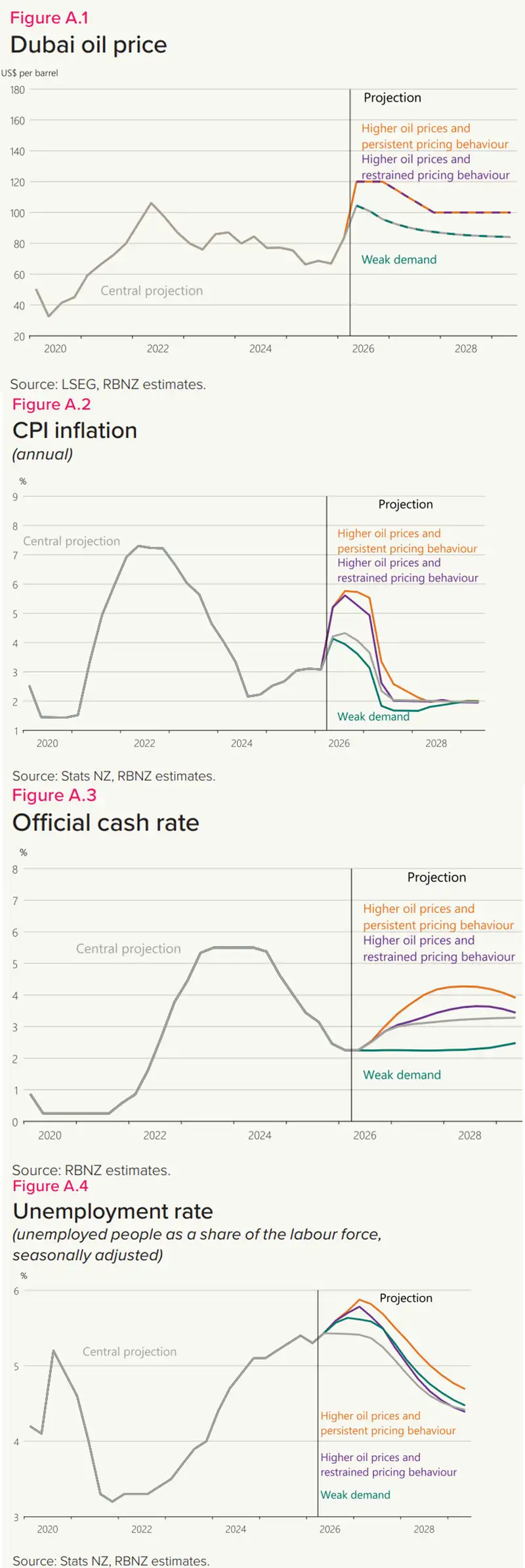

Scenarios: it goes like this the 4th the 5th…

We applaud the (re)use of scenarios in the document. Even if we don’t like what we see.

The RBNZ gave us four possibilities for the Kiwi economic outlook and inflationary pressure. We’d like to add a 5th.

The four given scenarios play with a mixture of oil price variations and inflation stickiness. Let’s review:

First, the most hawkish scenario assumes higher oil prices and persistent pricing behaviour, with “Firms’ price‑setting behaviour becomes more sensitive to higher inflation, resulting in stronger second‑round price effects”.

Second, we have a mixture of high oil prices, but firms absorbing more of the costs. In this instance “Higher inflation does not become embedded in price- and wage‑setting behaviour over the medium term”.

Third, we have the Middle East conflict resolving, and the predicted oil price falling. The most dovish stance sees weak demand despite oil prices dropping. With a “larger negative impact on global and domestic demand”.

Fourth, the central scenario is the RBNZ’s best guess for the future of the Kiwi economy. This track also assumes oil prices will normalise, with inflation falling in the medium term. The scenario notes that “Significant spare capacity in the domestic economy is continuing to dampen underlying inflationary pressure and is expected to limit firms’ ability to pass on higher costs”.

Fifth, our view sits close to the RBNZ’s central scenario. We know that the oil price, while it continues to stay elevated, will push inflation up. Mechanically. Once the oil shock is finished reverberating through the Kiwi economy, we’ll feel the full impact of the demand destruction happening right now.

We expect the spare capacity in the economy will lay a heavy hand on inflation in the medium term. With core inflation likely to stay within the RBNZ’s target band. We aren’t keen on the view that the economy needs any more medicine.

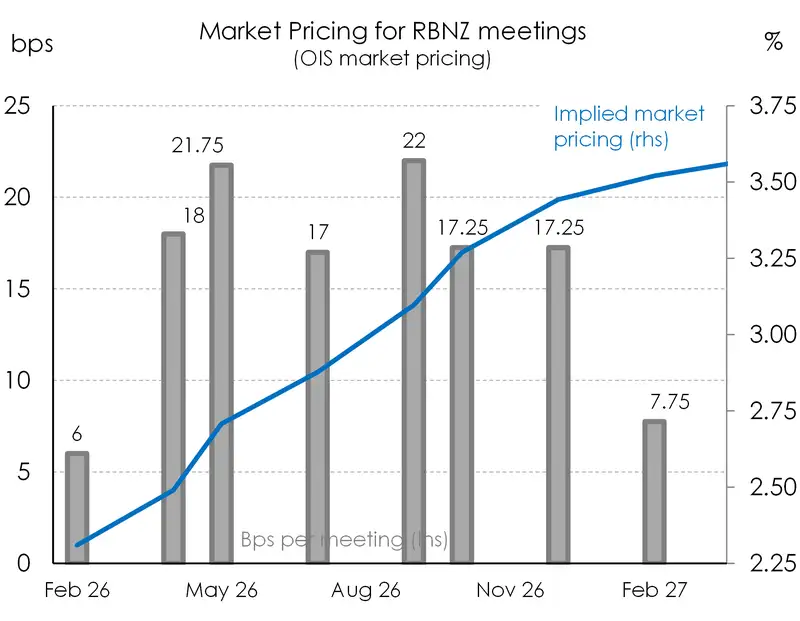

Wholesale rates were ahead of the game.

Wholesale rates have been well positioned for today’s (in)decision.

Before the RBNZ’s announcement, the market had 4bps (16% chance) for today’s meeting, 17bps for July (68% chance), 72bps by December (nearly 3 hikes), and a swift lift to 3.5% (125bps) by this time next year. See our OIS rates graph.

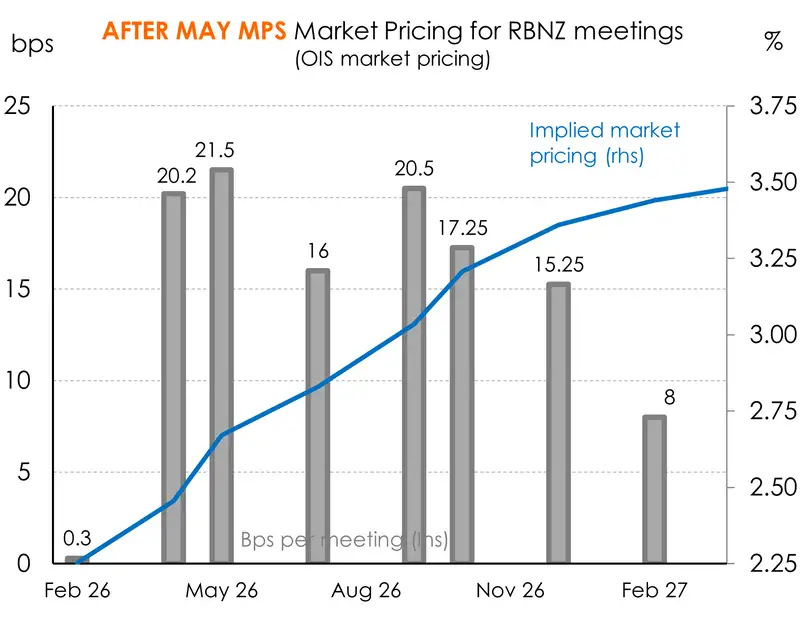

Following the RBNZ’s indecision, the 4bps priced in July (not a bad bet in hindsight) rolled into July, and we’ve seen a tightening up of rate hike expectations… but ultimately ending at the same point (3.5%).

To quote one of our traders, “it feels like an insurance move. Hike early. It hurts. Then hold. They probably only have to hike twice before they’re done”. Thanks Rosco. You make a good point.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.