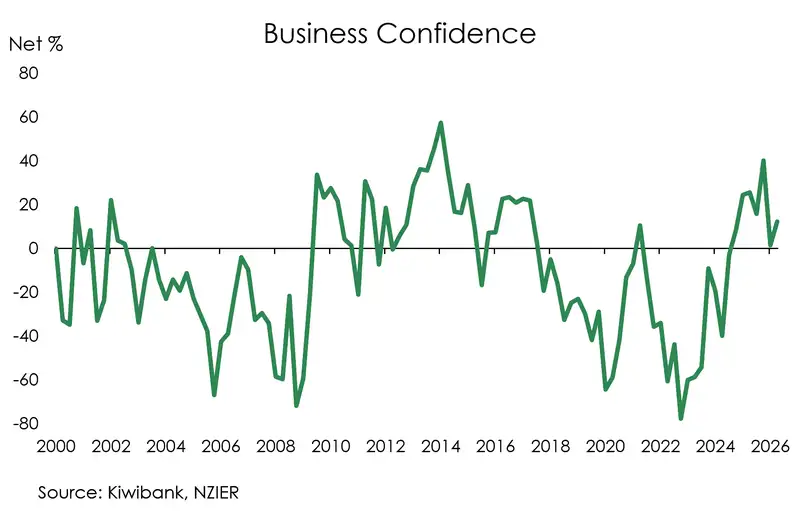

- Business confidence is on the mend. Businesses appear cautiously optimistic that the worst of the Middle East conflict is behind us and that better times await. However, domestic activity remains tepid. International events appear to be the biggest determinant of business confidence in New Zealand.

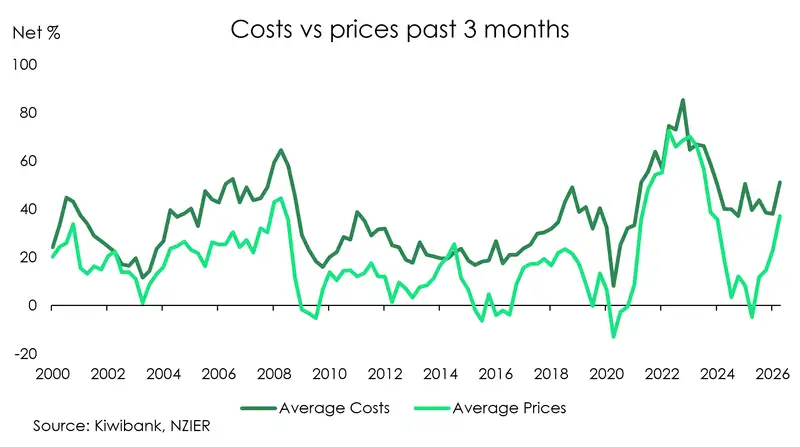

- Most sectors have passed on higher costs in the form of higher prices, except for construction. The extent to which high prices are sustained will depend on the recovery of domestic demand and geopolitical volatility.

- Businesses are reporting that it is much harder to find skilled workers compared with unskilled workers.

All figures are seasonally adjusted unless otherwise stated.

Business confidence has broadly improved in the June quarter, with a net 12% of businesses expecting better conditions in the coming months. This stands in stark contrast to the 1% of businesses expecting better conditions ahead in the March quarter. This is according to NZIER’s July Quarterly Survey of Business Opinion (QSBO) covering the June 2026 quarter.

he higher confidence levels reported for the June quarter appear to be driven almost entirely by international factors. The survey was fielded between 10 June and 7 July 2026. The Memorandum of Understanding (MOU) between the US and Iran was signed during that time, on 17 June 2026. Businesses who responded to the survey before the MOU was signed exhibited lower confidence levels compared to those that responded after. Higher confidence in the June quarter is also reflective of lower oil prices.

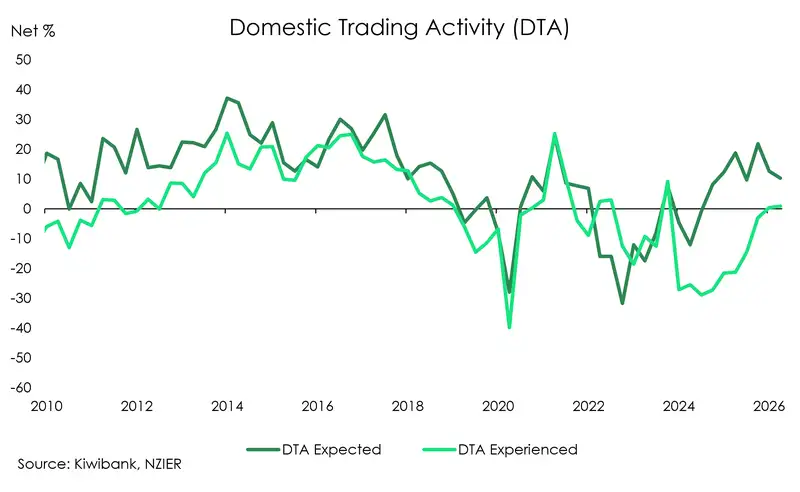

Domestic trading activity remained weak. Only a net 1% of businesses reported an increase in own activity in June, up from 0% in March. Expectations of domestic trading activity has fallen. A net 10% of businesses expect an increase in activity over the coming months, down from 13% in March. This suggests underlying domestic demand is weak. Again, international developments are the key right now.

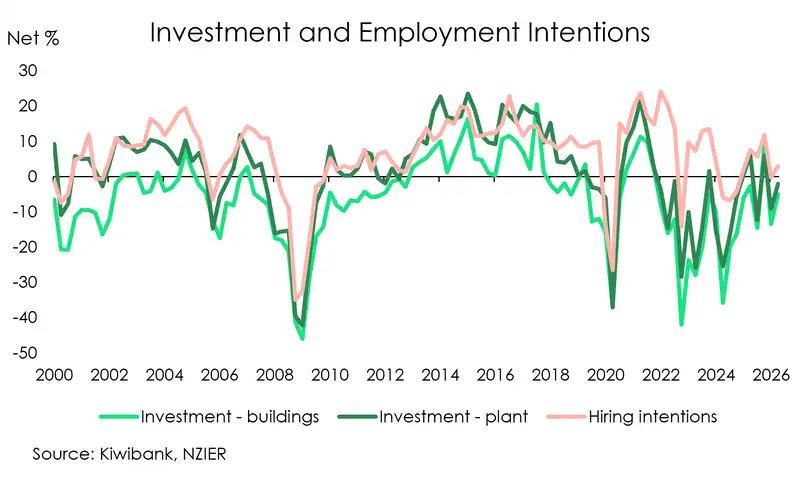

While conditions in the Middle East improved in the June quarter, volatility still reigns supreme. Geopolitical volatility and election uncertainty has had a chilling effect on investment. A net 3% of businesses plan to reduce investment in buildings, plant and machinery over the coming months (not seasonally adjusted). Manufacturers remain more optimistic than builders.

Cost pressures are mounting. In most sectors, increased costs are being passed onto customers through increased prices. The exception is building, which saw a significant increase in the net proportion of respondents with higher costs yet a decrease in the net proportion of respondents increasing raising prices.

With many businesses raising prices, it begs the question of whether this will lead to a sustained or simply a temporary spike in inflation. Above-band inflation is a given for the June quarter. It is likely through to the end of this year. However, underlying domestic demand is weak and the interest rate hiking cycle underway. Oil prices, though volatile, were lower than we saw earlier this year (although that’s reversing quickly this week). But a lower net percent of businesses were expecting higher costs over the next 3 months.

Difficulty in finding workers is most acute for skilled workers. Businesses are finding it relatively easier to find unskilled than skilled. A net 20% of businesses reported finding it easier to find unskilled workers, contrasted with a net 8% of businesses finding it harder to find skilled workers. The implication is that unskilled workers have less bargaining power in employment negotiations. This will likely lead to slower wage growth for lower skilled workers.

The chart above shows that the net percentage of businesses planning to increase costs over the next three months is at historically elevated levels. These intentions mean that the Reserve Bank may feel a bit vindicated after increasing the official cash rate last week.

In a speech given this week, RBNZ Chief Economist Paul Conway, noted that inflation pass through is affected not only by demand and labour market pressures, but also by the speed with which firms update their pricing. Research shows that Kiwi firms are updating their prices faster – leading to higher pass-through rates from the oil crisis.

Firms that rate non-labour input costs, demand conditions, stock levels, or competitors’ prices as important generally review and change prices more frequently; compared to firms that rate labour costs as important. This means an un-even pass-through, with cost pressure transmitted through non-labour channels associated with more frequent price adjustment.

Combined with recent pricing intentions, it is clear that the RBNZ is worried that inflation will persist beyond the supply shock and become embedded. This doesn’t take away from the fact that moving to a neutral interest rate (debated to sit around 3.25% - 3.5%) is going to hurt.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.