- We can’t ignore the two big domestic decisions out this week. First, the RBNZ’s monetary policy statement on Wednesday (where we expect they will hold the official cash rate steady at 2.25%). Second, the Budget out on Thursday. We wait to see if there are any hidden lollies buried amid anticipated cuts.

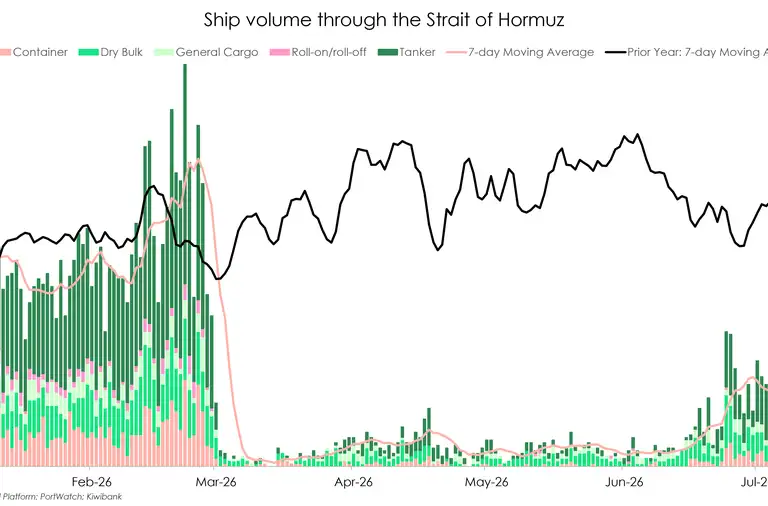

- Markets are reacting with volatility on the apparent good news of peace negotiations going well in the Middle East. We have whiplash. It’s hard to take good news seriously after so many weeks. Once the Strait of Hormuz is open, it will take months for transit to re-start and a new normal to be reached. Until then, we wait…

- Our view is unchanged. We need a concrete peace and oil prices to come down before we can assess the damage. Inflation is spiking now, but demand is being destroyed in the process. There is no need for rate hikes this year, at least not on the data we have so far. Patience is key.

We have a big week domestically, the May MPS is out on Wednesday. We don’t expect recent headlines to play much, if any, part in the RBNZ’s thinking in this meeting. We expect them to hold the OCR steady at 2.25%.

We follow that up with the Budget on Thursday. We’re not expecting a lolly scramble, most talks have been of cuts, cuts, and more cuts. But we won’t rule out the chance of some up-side surprises. It is an election year, and it will take some offsets to the proposed cuts to appeal to voters.

It seems that the war in the Middle East is almost over… but we’ve heard it all before. It’s hard to take the latest Trump tweets seriously. There are still significant gaps between the two parties’ positions and the expectation is that 30 to 60 days of negotiations are still needed. The two major sticking points being the free passage of all vessels through the Strait of Hormuz, and Iran relinquishing its enriched uranium and never pursuing nuclear weapons.

The price of brent crude took a small tumble at the end of the week from$110USD to $104USD per barrel, on news of potential peace. But there’s been volatility in that price since. The 10 and 30-year US bond yields which took off two weeks ago, have been slowly declining again – while the S&P 500 (the key index Trump follows) is climbing back up, and is likely to reach new record highs if peace talks go well.

What does that mean for us? A resolution to the conflict will push oil prices down – and we would likely see petrol prices follow not long after. But we would need concrete proof of peace confirmed before the Reserve Bank will act in response. Even once the Strait of Hormuz is open, it will take months (some estimates say 6 months) for transit to re-start and a new normal to be reached. Insurance costs for ships passing through the Strait will likely remain elevated long after the war ends, adding a stickiness to some of the inflated oil and gas prices we’ve seen.

So, we won’t know the full impact on the Kiwi economy and the amount of scarring or inflation stickiness until the end of the year at best, but potentially even into 2027. It’s clear that the economic impacts of this crisis will have ripple effects that will last a long time. We’re starting to think a recovery may just be a mid-2027, early-2028 story now.

In our COTW we discuss why wholesale market pricing doesn’t dictate that the RBNZ will need to hike the OCR this year. Short term inflation, off the back of an international oil shock, is not something interest rates can fix. Especially when demand destruction is the result. An economy threatening to flat-line while fuel prices are elevated will need resuscitation, not further dampening.

Hiking early will only kick the economy while it’s down. The fear that this will be another Covid situation is unwarranted. We weren’t the early bird catching the worm back then… but we can be the mouse that gets the cheese this round. If only the RBNZ will have the patience the market doesn’t.

Financial Markets

The comments below were provided by Kiwibank traders. Trader comments may not reflect the view of the research team.

Rates – RBNZ week…

Last week offshore events and data applied a little more direction to local markets, leading to a see-saw market over the week, while local data (though predominately survey-based) did add to the view surrounding the upcoming RBNZ decision

Monday saw rates open higher following international moves after our close on the Friday. The Performance of Services Index release mid-morning did apply some further weight and while still sub-50, did see improvements in subcategories such as new orders. The May meeting implied rate continued to track around 30% though year-end and beyond. And saw priced tightening tick higher with the curve applying a steepening bias with the front anchored, to a degree, by the low-priced May probability.

Tuesday saw the release of the RBA meeting minutes which added to an initial firm tone for the market which had largely shrugged off some Fed-speak on inflation and a US market that had been re-rating the chances of a 2026 tightening. Post release, Australian rates pressed ahead with further gains as the minutes were viewed as offering a hint of pause in the outlook. With conditions viewed as restrictive by the committee, and this sentiment flowing into our curve, though flattening on the rally. Our 2-year moved -6.5-points and 10-year -8.5-points on the day, while the implied path continued to take the opportunity to remove a point or so off.

Wednesday, the see-saw pattern continued as the curve opened higher following similar moves internationally, though with another RBNZ survey of inflation expectations to provide interest. This time it was the Household survey, with this showing some sharp jumps in perceptions of one and two-year ahead inflation, though the reduced history of the some of the aspects of the survey and the wide variance between mean and median (lower) figures did see caution applied, with this same caution likely applicable to the similar Business survey released Thursday that showed a jump in one-year ahead though relatively anchored, sub 3%, expectations from two-years outward.

The main event of the week however proved to be Australian employment data released on Thursday. This series can at times be a volatile one, with often a flip between full-time and part-time jobs providing opportunities for any particular view to press its point. However, with falls in full-time and part-time employment, a jump in the unemployment rate and a decline in participation, all against expectations for a stable if not solid print, resulted in a strong rates rally and a fall in the AUD. On this point, only time will tell if this was or could be the point at which the seemingly one-way traffic on the NZDAUD cross slows or potentially reverses, or if it is merely a pause in the longer trend. The Australian short-curve did move to reduce the priced terminal cash rate by around 15-points post data. The rally sentiment spilled over to our market, with this adding to initial early gains. The curve finished lower and flatter on the day, with 2-year -7.25-points to 3.565%, 10-year -10.75-points to 4.35% while the implied path continued to slowly reduce near-term tightening expectations. Friday saw some paying interest at the front of the curve though the market appeared to absorb that well, trading in a narrow range. T

The weekly GDP nowcast predictor model by the RBNZ again declined, with the modelled predictor now indicating near zero for Q2 GDP. For the week, we saw 2-year IRS close Friday at around 3.57% and 10-year at 4.34% - both around 7-points lower on the week. The implied path continued to price a May meeting move at around 25%, with the year-end at just above three 25-point tightenings.

For the week, RBNZ is the key event, with the market attempting to price the balance between what it believes the RBNZ will do given the framework of the Act and the remit and the dataflow and expectations around inflation. Considering new information on the week for the committee, this will likely include some of the international meeting releases – the indications the US Federal Reserve may be more predisposed towards tightening and that the RBA may not, and the RBNZ’s own GDP nowcast weekly update that has taken a sharp turn lower of late. The newer period-ahead inflation expectations on the Business and Household surveys probably do not yet hold the same weight as the prior week’s survey of expectations, though may still be useful. Regarding the policy framework, the RBNZ Act and the Monetary Policy Committee Remit also note other considerations when implementing policy alongside inflation targeting; notably discounting disturbances to inflation expected to be temporary and also having regard to seeking to avoid unnecessary instability in output, employment, interest and exchange rates. How these are all weighted and considered by the committee against the forecasts and risks will be the determining factor. Given the pricing and steepness of the implied path, markets would appear to be siding with the no-change outcome. Graham Hughes, Trader – Financial Markets.

In currencies - All Eyes on Wednesday: Kiwi Poised as Macro Risks Collide

It’s shaping up to be a big week ahead. An Iran deal appears on the precipice, while we have important April inflation readings out of Australia and the US, Budget 2026, and the highly significant RBNZ MPS on Wednesday.

Last week largely saw consolidation for the Kiwi, as participants navigated ongoing—but generally constructive—headlines around at least some form of resolution to the Iranian crisis. Furthermore, a repricing of longer-term inflation risks - via below, or contained-expectation CPI prints in the UK, EU, and Canada, softer Aussie jobs data, as well as a “not scaring the horses” beyond 1-year RBNZ business expectations print - helped take some heat out of NZ OIS pricing ahead of the MPS. Markets are now pricing just a touch over 3 x 25bp cuts by the end of 2026. We open this week with a likely positive bias. For NZD/USD, the week ahead likely sees the pair trading within either a 0.5800–0.5890 or 0.5890–0.5990 range, depending on the timing and outcomes of the key risk events. A number of combinations and permutations could play out, but the broader 0.58–0.60 range remains the focus - ultimately hinging on how the RBNZ positions its OCR track from July onwards.

NZD/AUD also enjoyed a largely positive week—something of a rarity in recent months. Australia’s April jobs data and the minutes from May’s RBA meeting both contributed to some AUD softness. The key levels to watch this week are 0.8170–0.8250; a break on either side will likely be pivotal in determining the medium-term direction for the cross. Wednesday shapes as the key day of the week, with the April Aussie CPI print dropping just 30 minutes ahead of the RBNZ announcement. Hamish Wilkinson – Senior Dealer, Financial Markets.

The Week's Key Events:

- Domestic events this week include the RBNZ monetary policy statement on Wednesday, and the much anticipated Government Budget out of Thursday.

- The war in the Middle East is still going. We have whiplash after weeks of good news turning bad, turning good again. Time will tell if the current peace negotiations lead anywhere...

- International data to watch. European area consumer and economic confidence data is out this week. Same with the US, as well as personal income and spending, house prices, Q1 GDP.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.