- The RBNZ will hold the OCR at 2.25% this week and remain cautious through 2026. Wholesale rates are pricing too much relative to the realities playing out in the Kiwi economy.

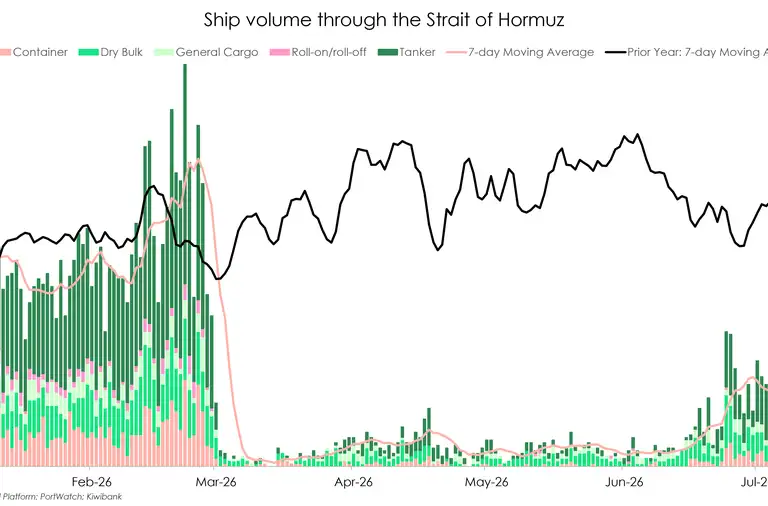

- Demand destruction, a weak labour market, weakening business appetite for risk. All putting simultaneous downward pressure on growth and inflation. Add to that the oil shock and you have an economy wearing concrete shoes.

- Our view is unchanged; rate hikes are not warranted in 2026. Hiking rates when the economy is already tanking, risks worsening both growth and employment outcomes without materially lowering inflation.

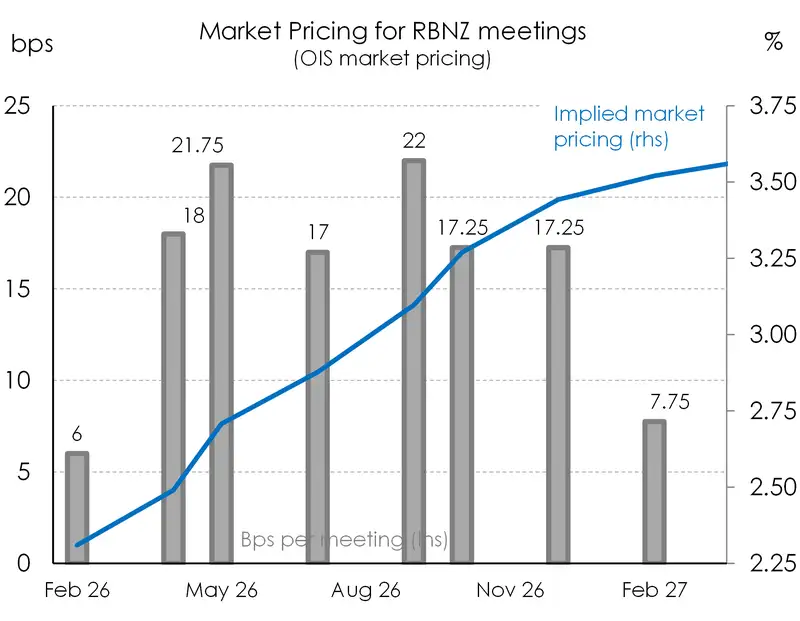

A big week ahead in markets, particularly the overnight index swap (OIS) market. Wholesale rates are getting ahead of themselves. Again. Short‑end rates are sitting well above the Reserve Bank’s current 2.25% official cash rate, with the front of the curve implying a degree of tightening that doesn’t sit comfortably with the economic reality.

Demand destruction, a weak labour market, weakening business appetite for risk. All putting simultaneous downward pressure on growth and inflation. Add to that the oil shock and you have an economy wearing concrete shoes.

In theory, OIS is the cleanest read on where markets think the official cash rate is heading. In practice, in NZ, it’s anything but. These wholesale rates are the financial market instrument of choice for banks to hedge against changes in the Reserve Bank’s rate. But OIS pricing is constrained by thin liquidity and structural frictions. The market is small and concentrated. A handful of local banks dominate pricing, and outside of key event dates there isn’t a lot of genuine two‑way flow. On top of that, there are the usual technicals. Bank balance sheets, mortgage hedging, and regulatory settings all shape flows.

Even the most hawkish bank economists, the ones calling for three hikes (75 basis points), can’t keep up. That would bring us from 2.25% to 3% OCR by the end of the year. The market has three and a half hikes (to 3.10%) priced in by December. Then a continuation to 3.5% by mid-2027. That’s well above the consensus. If the hawks are right, and they hike to 3%, short-dated rates are 50bps overcooked. If we’re right, short-dated rates are a long way from home. But that only lasts for so long. If we get clearer guidance from the RBNZ on Wednesday, we could get some of the larger offshore players (hedge funds) re-entering the market to scoop up all those beautiful bps on the table.

Our view is unchanged; rate hikes are not warranted in 2026. Hiking rates when the economy is already tanking, risks worsening both growth and employment outcomes without materially lowering inflation.

Bottom line:

Wholesale markets are sending a strong signal, but it’s not a clean one.

OIS pricing is being pulled around by thin liquidity and technical factors, while global volatility is adding noise on top. The result is a curve that looks more aggressive than the underlying story justifies.

Meanwhile, the economy is cooling. Inflation will spike in the second quarter. True. But its source is off-shore and highly likely will be transitory. It’s too soon to pull the trigger and call it sticky. That combination argues for patience.

For now, the RBNZ looks firmly on hold and likely to stay there longer than markets are pricing.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.