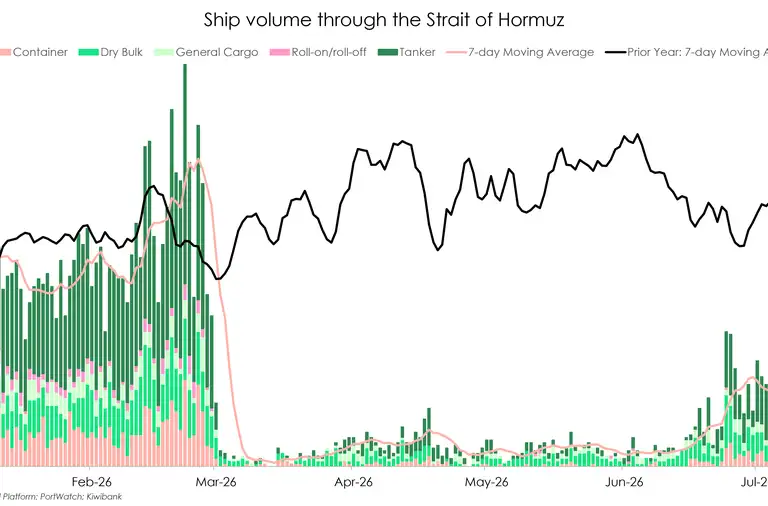

- The war in the Middle East is keeping us in suspense. The negotiations appear to be back on between Iran and the US. We expect to see a lot more back-and-forth on that front. The price of Brent Crude is fluctuating at speed – trying to keep up with headlines. The S&P 500 and Nasdaq hit record highs, the US market is booming.

- Domestically, the NZX50 saw an upward swing last week too. Governor Brenman’s speech in Hamilton on Wednesday was read as dovish, and wholesale interest rates have come down slightly, but still pricing in a full hike in July.

- Labour market data out this Wednesday, but any up or down-side surprises won’t spook us or the RBNZ. The true impact of the war will be in how businesses fare. And they’re cutting back, not hiring new staff, not expanding their operations. We will feel the consequences of this contraction in 6 to 12 months – and that’s the horizon the RBNZ should be looking at too.

Oil prices have been up and down and up again. Last week, the price of brent crude reached a high for the year, of $126USD. The spike was short-lived, and the oil price fell back down on news that Iran had delivered a peace deal to the US through Pakistan. That brought crude prices down, we are sitting at $108USD per barrel this morning – and we expect more fluctuations.

The S&P 500 and Nasdaq hit record highs despite the war and uncertainty – the US economy is weathering the crisis well, decreasing the chance that Trump will pull out of the war any time soon. The VIX index, still subdued – back down to pre-war levels believe it or not! It’s like nothing is happening.

Domestically, wholesale interest rates have fallen back over the week - pricing in one 25bps rate hike in July, and 86bps by December. Pricing is still too aggressive, but moving in the right direction. We see the need for no rate hikes. And even the most aggressive economics team is calling for 75bps (not 86). The two-year swap rate has also started coming down since Wednesday. Interest rates fell off the back of Governor Brenman’s speech in Hamilton on Wednesday, which the market read as slightly dovish.

This week, we have labour market data for the first quarter on Wednesday. We aren’t expecting big moves in the unemployment rate, we expect it to stay between 5.3%-5.4%. On the day, upside or downside surprises won’t change the story much for us. We need time to assess the damage, and that’s why we’re in the no-hike camp.

Kiwi households are cutting back on spending where they can. The cost of essentials like electricity, food, rates, premiums… have all gone up, and now we have petrol on top. Kiwis have less and less left over at the end of each week to spend on anything non-essential.

Kiwi businesses are also feeling the cost crunch. The cost of running machinery, shipping and packaging has gone up due to the war in the Middle East. And the demand for their goods and services has gone down because households have less free money to spend. It follows that businesses are cutting back on their own spending, not hiring new staff, not expanding their operations, not giving out bonuses or pay increases. So wage growth will be stifled, and unemployment and underutilisation will remain relatively high, if not increase.

These effects don't happen overnight. In 6 to 12 months, we will see more of the impact of the war on the wider economy. That's the horizon the reserve bank is looking at. We don’t expect the Q1 labour market data to really nudge expectations for interest rate hikes much in either direction. It’s still a wait and see situation.

Financial Markets

The comments below were provided by Kiwibank traders. Trader comments may not reflect the view of the research team.

Rates – Inflation, sentiment and ‘hawkish holds’

With the abbreviated week and seemingly no progress towards achieving a breakthrough in negotiations for peace in the Mid East, the market continued to turn its attention to market related data and events for direction. With the week providing for a solid mix of hard data, reads on sentiment, and central bank decisions.

Our rates market opened on Tuesday after the long weekend with a parallel shift higher by around 1 to 2-points, broadly matching a similar sized move in Australian 3 and 10-year futures and shrugging off a US curve over the same timeframe which was a net 2-points lower in yield. Price action continued to grind higher in the lead up to the BoJ rate decision, the first of many central bank decisions due over the week. The BoJ, while delivering an unchanged decision, perhaps provided the playbook for the likes of the Fed, BoC, ECB, and BoE to deliver ‘hawkish holds’. The messaging around balancing the uncertainties around the impacts on growth and inflation for policy, supplemented by ‘dissenters’ to the final decision to remind if inflation expectations were to become embedded. The day finished with the curve higher and flatter, 2-year at 3.53%, 5.5-points higher, and 10-year at 4.325 (+4.5), while the implied OCR path indicated 125-points of tightening over the next 12-months.

Wednesday delivered key events for the local market with Australian CPI and the prospect of a comment from the RBNZ Governor. The Treasury also released its fortnightly economic summary, which again erred on the downbeat, highlighting a loss of momentum for the economy, lower confidence, and card data indicating fuel spending crowding out discretionary spending. Data saw Australian CPI printing below expectation, including the trimmed mean, with this coinciding with the publication of notes from the RBNZ Governor’s community engagement in the Waikato, taken by the market as being on the dovish side, combined this resulted in the curve backing off yield highs to finish lower on the day. The implied OCR track which had earlier moved to price the chance of a May meeting hike at around two-thirds probability, pared this back to below 50%, while the swap 2 to 10-year swap curve finished -4 in a broadly parallel move. The engagement notes appeared to reiterate previous themes, noting the disruption, the medium-term focus on inflation while ensuring that temporary increases in inflation don’t embed. But added that while headline was above band, core measures had remained stable within band, noting the Bank remained focussed on balancing inflation control with supporting economic recovery. Rates continued to see-saw through the remainder of the week. Thursday higher as the US Fed, while unchanged made use of the dissenter theme, and Friday lower, with the local market starting to see receiving interest outweigh. Pessimism on the economy starting to build as the prior sessions' sharply weaker business outlook survey was followed by a sharply weaker consumer confidence survey. With weaker building approvals data thrown in for good measure, cumulatively starting to weigh on thinking. By the close, the NZ curve was seen near unchanged on the week, with 2-year marked at 3.535 (+0.5) and 10-year 4.3175 (-0.75), while the OIS curve looked to pare back some of the aggressive front-loading that had occurred. May probability closing at or around 30% with around 3 ½ 25-point moves by year-end.

For local rates markets, taken in isolation, inflation, despite the noted slowing in core, may be supportive of the tightening argument. However, noting the rapid deterioration in consumer and business sentiment, reported paring back of discretionary spend, as well as the patient ‘hawkish hold’ approach adopted by other central banks, the current aggressive five tightenings in seven meetings rate path pricing may be vulnerable to a similar approach by the RBNZ. In this regard, the upcoming RBA decision may see a greater degree importance placed upon it from our point of view. While we would note that the path for rates is likely higher, moving away from the current 2% setting, the current uncertainty probably sees any such move contingent on confirmation of either that there are signs that pricing has spilled into second-round cost increases, or that the economy can sustain an increase in rates – a balancing that was noted in the latest Governor comment. Under this scenario, a continuation of accrual supporting the front, with the broader range trade in shorter rates persisting, 2-year in that 3.30% to 3.70% range as we have witnessed lately, will probably continue to play out with perhaps a bias to a mildly steepen the short to mid-curve. Graham Hughes, Trader – Financial Markets.

In Currencies - Groundhog Day:

Last week in currency markets, the main event of note was intervention in the Yen. On Wednesday USD/Yen traded from 160.60 down to 156.35, after Japanese officials issued a final warning. The US dollar index subsequently headed lower, from 99.00 down to 98.10. Otherwise, the distinct lack of volatility remained the backdrop for currencies.

The Kiwi dollar stuck close to the 0.5900 level early in the week. Comments from the RBNZ’s Dr Breman saw an unwind of some of the hikes priced into the front end of the curve, and the Kiwi dollar fell back to 0.5830. This was prior to Yen intervention, and the softening in the US dollar saw the Kiwi reverse the majority of the move lower, heading back to the 0.5900 level again to close the week. Essentially a round trip for the Kiwi dollar over the week. NZDAUD fell below 0.8200 again last week, largely on the back of the RBNZ comments, trading from 0.8230 down to the week’s low of 0.8179.

Overall, it was still a familiar range for the cross, but the story of divergence between RBNZ/RBA tightening outlooks may continue to see a move lower in the week ahead. This week the domestic data print of note is the Kiwi labour market, which could potentially provide a catalyst as could the RBA tomorrow. Mieneke Perniskie– Senior Dealer, Financial Markets.

The Week's Key Events

- We have some domestic data to look forward to this week. The March quarter labour market data will give us a better idea of the slack in the labour market at the onset of the war in the Middle East. We also have the Financial Stability Report from the RBNZ on Wednesday too.

- Lots of monthly data out for Australia, MI inflation, job adds, building approvals and household spending. But most are looking to the big RBA cash rate decision on Tuesday. A hold there might dampen wholesale markets here, but most are expecting a hike.

- The war in the Middle East is still top of mind - peace negotiations seem to be picking up steam. We continue to watch this pace.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.