- Price tells the story. And the oil price tells us that the war in the Middle East is not ending soon. Last week we predicted that oil would plummet or take off, and it’s blasting off (again). Despite the chin-wagging from the White House and other world leaders, the Strait of Hormuz is still closed, and we are still waiting…

- Domestically, Kiwis and Kiwi businesses are doing it tough. The grocery bill is growing faster than most others, while wages are tracking sideways. Filling up the car is still exorbitantly expensive, and most businesses are cutting rather than adding jobs. The situation is clear. The economy is contracting.

- Our view is unchanged. Inflation expectation data out last week paints a picture. Inflation is spiking now (in this year and one year ahead) and coming down in the long term. This supports our view. No need for rate hikes. No need for panic. The economy is not going to boom when this is over, but will more likely need resuscitation.

Oil prices tell the story… and they’re on the up and up (again). The price of Brent Crude is up to $109USD per barrel. It’s been creeping slowly back up from the $90USD per barrel lows we saw in mid-April. That’s indicative of the situation in the Middle East. The cease-fire is feeling stretched. Fragile. The US is trying to pull in other players to help open up the Strait of Hormuz. Despite the chin-wagging, no one is biting. So that leaves us… stranded.

Domestically that means another week without price relief at the pump. Another week of business costs remaining elevated and putting pressure on strained Kiwi consumers. And it’s slowly showing up in the data.

Businesses are feeling the strain more and more. They’re pulling back on spending, and they’re cutting back on jobs. Some are cutting hours, some are cutting staff. And we expect more restructuring as the situation drags on. That’s bad news. Fewer jobs and higher unemployment put significant downward pressure on growth. The economy is stalling, and may need resuscitation when this is all over.

Lower economic activity and higher unemployment also put downward pressure on inflation. Prices may go up mechanically as a result of the petrol prices, but there’s a limit. There’s only so much a strained consumer can take, before they slash spending. And the consumer pull-back on spending has started to show. We expect to see the Kiwi economy contract in the second quarter of this year. We’re feeling it already.

Last week we saw the food price index print higher. We dive into the data in our chart of the week. Groceries are getting more expensive, faster than other goods and services, and much faster than wages. That hurts vulnerable Kiwis more. Disproportionately, poorer households face heavier burdens. And more Kiwis are being put in the heart-breaking position of choosing between food and other necessities like heating their homes in winter.

One shred of good news did come out of the data last week. The inflation expectations survey was released by the Reserve Bank. The average one-year-ahead inflation expectation was 3.41%, well above the RBNZ’s target band. But we expected that. The two-year-ahead expectations averaged 2.53%, well within the band. And we agree with the disinflationary outlook over the medium term. The consensus is clear. There’s no need to panic. Inflation will spike in the short term and come back down in the medium term. The RBNZ has time. Because the data supports looking through this inflationary period, especially given the economy is currently contracting.

The domestic wholesale rates market has come down slightly (still pricing in a full rate hike in July). We stand by our view. There’s no need to hike rates. It’s too early and uncertain. Rate hikes now would only add pain without any commensurate gain.

Financial Markets

The comments below were provided by Kiwibank traders. Trader comments may not reflect the view of the research team.

Rates – Domestic data flow and the RBNZ

Last week, despite thoughts that conflict related headline may be due to insert themselves more forcefully into markets it was local data that delivered what could be a key data points ahead of the RBNZ May policy review in the form of the RBNZ survey of expectations and Statistics NZ’s selected price indexes data.

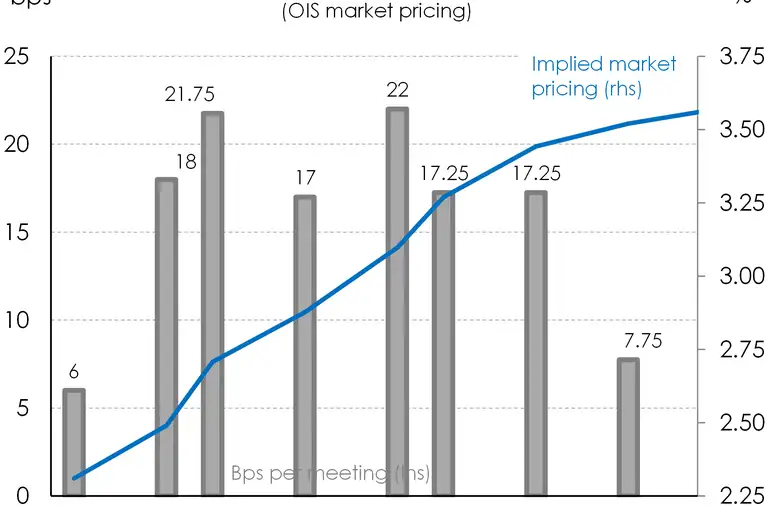

Monday saw the IRS curve open unchanged despite firmer US markets, drifting higher throughout the session. Treasury released its regular economic update noting the risks to the outlook posed by weaker consumer and business confidence, though the curve continued to see pressure up the front, pivoting around the 5 to 6-year area, finishing around 1.75-points higher up the front and 1.75-points lower at the back. By Tuesday, deteriorating prospects around the peace negotiations saw rates markets sharply weaker, the US Treasury curve was marked higher by around 7-points seeing the NZ curve on the back foot from the open, initially around 2-points higher 2 to 10-years, then further weakening as the ability for the local market to absorb some larger risk flow was tested. The front of the swap curve trading the heaviest and notably diverging from a relatively flat Australian market on the day. The implied OCR path continued to ratchet with the May RBNZ meeting priced at 50:50, with near 100-points of tightening priced by year-end.

Rates remained pressured into Wednesday ahead of the RBNZ survey of expectations, with the market again struggling to find receive side flow to offset despite another Australian bank pointing to the likelihood of a Q2 contraction, 2-year marked higher by 8-points and 10-year +7, while the implied path traded May RBNZ probability at near 60% with 3.50% OCR priced by March 2027. The release of the survey sparked a swift reversal as the closely watched 2-year ahead expectation at 2.53 against 2.37 previously was viewed more favourably by the market, with the gap between the 1-year ahead and 2-year ahead potentially signalling that the near-term inflationary impulse was not seemingly embedding into longer term expectations, particularly with declines noted in the longer five and 10-year ahead expectations. This was seen as adding weight to the patient, albeit hawkish, scenarios for monetary policy – an approach spoken to in recent policy statements where the balancing of responding pre-emptively to the risk of higher medium-term inflation was weighed against the cost of unnecessarily stifling the economic recovery was noted. By the end of the day the curve had re-traced much the mornings move higher, particularly the short dates, with the 1-year IRS back at unchanged on the day at 3.23%, 2-year +2.5-points at 3.655%, 5-year +4 at 4.06%, and 10-year +4 at 4.405%, while OCR path expectations were marked lower, with May meeting odds at less than 50%.

Friday’s release of the SNZ selected price indexes provided the second read around potential price pressures in the economy, with the curve seen largely unchanged headed into the release having managed some small gains on Thursday. The April price index data appeared to indicate that outside of fuel/energy transport group, that prices appeared contained – even for those regular positive contributors – alcohol and tobacco. Rates managed some slight gains on this, though faded as international rates markets tracked higher, seeing curve moving higher alongside. The weekly RBNZ GDP nowcast release late Friday did see a small bid into futures towards the close – enough to see 1-year back to near unchanged on the day, as the current Q2 predictor fell sharply to +0.1% from +0.6% at the start of May. For the week, 2-year IRS was seen closing at 3.64% (+9), 5-year 4.06% (+10), and 10-year 4.41% (+7).

With the RBNZ meeting due next week, the thought process around positioning starts to come down to how you think the RBNZ will respond, not necessarily how you think they should respond. We know that inflation is likely to track higher with a fair degree of certainty, though as to whether this will pass through and embed permanently is still open. Certainly, the past weeks measures around expectations did temper some concerns over embedding, and the selected price index data did appear to see a degree of containment, though this is less than certain going forward. We also noted modelled expectations slipping around the prospect for Q2 growth from the private sector and the RBNZ’s own models as rapidly declining sentiment starts to impact. Previous statements from the RBNZ would tend to indicate that they are open to using the flexibility afforded to them via the ‘medium-term’ language in the remit in order to satisfy secondary parts to the operational objectives, principally here, seeking to avoid unnecessary instability in output, employment, interest rates, and the exchange rate, but how this is all balanced in the final decision is the unknown. However, also into the mix will be the heavy international rates sentiment, with US officials in the past week seeming more inflation focussed in their talk, as in general the economic data continues to print firm, pressuring rates including the short-end pricing where priced probability is now leaning towards the chance of a 2026 tightening. With the May meeting priced probability around one third, and with rates markets biased towards higher, there will be volatility in our markets either way. Graham Hughes, Trader – Financial Markets.

In currencies - When you are on top, there is only one direction…

The broader rout in global bonds on Friday looks set to dominate early-week sentiment, with markets increasingly grappling with the implications of structurally higher yields. There’s been little in the way of positive catalysts either — the US/China meeting underwhelming and the Iranian situation adding another layer of geopolitical tension — leaving risk assets back under pressure. Steepening curves are now starting to lean against the recent equity rally, and that tension feels like it has further to run. Closer to home, the front end outperformed into the end of last week. A run of local data — hot, but not too hot, across inflation expectations, food prices and the SPI, alongside softer manufacturing prints — has given the RBNZ something to think about. The market response was a modest push lower in OIS pricing, tempering some of the more aggressive hiking expectations and, in turn, weighing on the Kiwi.

From top G10 performer the week prior, NZD slipped to ninth place, with the USD reasserting itself — particularly into Friday’s close — on the back of strong US data. That strength saw markets further pare back any lingering expectations of US hikes this year, reinforcing USD support through the back end of the week. Technically, NZD/USD is back trading around its 200-day moving average, gravitating toward the familiar 0.5840 zone to kick off the week. Meanwhile, NZD/AUD extended to fresh 13-year lows on Friday, touching 0.8165, driven by a combination of local data and broader risk aversion. The cross has opened slightly firmer this morning, so for now those lows remain intact — just. The 0.8170 level remains pivotal in the week ahead, with Aussie employment and Q1 NZ retail sales the key local drivers to watch. Hamish Wilkinson – Senior Dealer, Financial Markets.

The Week's Key Events:

- Domestic data out this week include some monthly series: retail sales survey, trade balance, credit card use data, and the performance of services index, which is a monthly survey of the New Zealand services sector providing an early indicator of activity levels. Importantly, data the RBNZ will be watching includes quarterly data on the Producer price index (PPI), which is out Tuesday.

- The war in the Middle East has no end in sight, unless you believe the chin-wagging from the While House. We don’t. The ceasefire agreement is holing but more fragile than ever. We are still anxiously watching and waiting.

- International data to watch this week includes Australia’s monetary policy meeting minutes released Tuesday, as well as a speech from RBA Assistant Governor. The UK has Average Earnings Index out the same day. China has some retail and industrial production data out and Japan has GDP data out this week too.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.