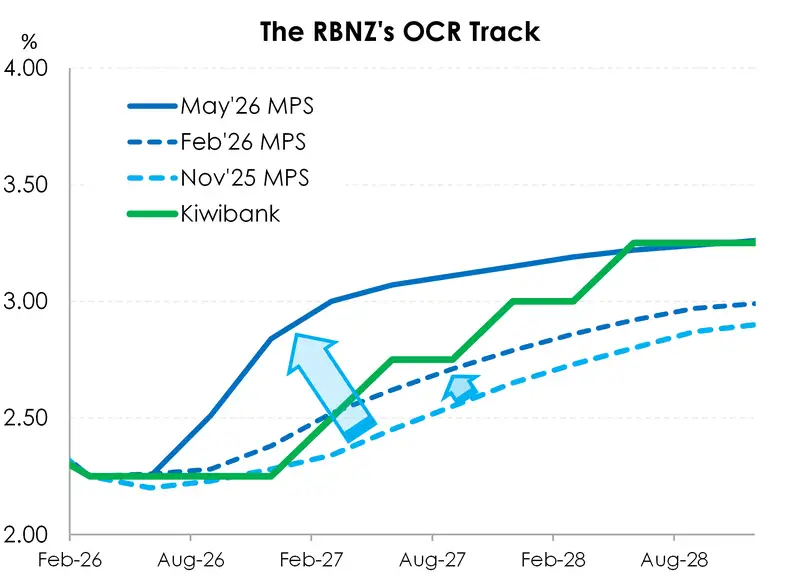

- The RBNZ gave us a lot to think about, we had a split vote 3:3 to hold the OCR at 2.25% and an updated OCR track. Rate hikes are coming sooner than we forecast. We now expect the RBNZ to start hiking in July, (not February ’27) as the MPC goes into July’s decision with a 50/50 split.

- Rates have risen in anticipation of hikes, and rates will keep rising as hikes are delivered. Take the medicine now, which will hurt the patient, in order to keep them off the operating table. We don’t agree that’s what’s needed. But the RBNZ seem fixated on cost pressures… outweighing demand destruction.

- Our core view is unchanged. Oil price related spikes won’t be dampened by interest rates. It comes down to when the Strait of Hormuz opens. Kiwi consumers are being squeezed over and over and over again. Many Kiwi households will be struggling to afford the strict necessities, slashing spending on anything nonessential.

A lot has happened in the last week. We had the RBNZ’s decision on Wednesday, followed by the Government’s Budget on Thursday.

The RBNZ’s decision, with forecasts, gave us a lot to think about. We expected a hold, but the RBNZ’s view of the economic risks turned out a lot more hawkish than expected. They want to hike interest rates, as soon as next month. There was a split vote, 3:3, with the externals on the committee calling for hikes. And the internals opted to hold (including the Governor’s casting double vote making it 4:3). Rate hikes are coming sooner than we initially forecast.

The wholesale market is pricing in a very convincing +90% chance of a hike in July. Indeed, we now think it’s more likely than not. There are three hikes priced in by the end of the year (to 3.02%, up 77bps), and the market is anticipating a swift move up past 3.5% in 2027. We’re not sold on a move beyond 3%, but the market will keep it priced until told otherwise. The RBNZ’s new OCR track was lifted to 3.25%, so market pricing is not far away.

Future inflationary pressures dominated the RBNZ’s discussions. “Considerably higher cost pressures” are outweighing the downside risks to growth. And the bank looks set to hike to weaken already weakened demand through fear of the inflation beast reappearing.

Everything comes out in the OCR track. And the track was lifted nearly 50bps over the next year. It came off a low base, but has risen well above our expectations. The end point of the track had another hike thrown in there for good measure, from 3% to 3.25%. As a result, we have to say what we think the RBNZ will do (hike ‘til it hurts)… not what we think they should do (pause to assess). Hiking with such a large output gap (underperformance) may prove to be too aggressive.

Our view is that the RBNZ is risking a lot to gain a little. Our analysis and liaison with businesses suggest much more subdued price setting behaviour, and deeper demand destruction. The economy hasn’t recovered from the deep double dip recession of 2024-25. 2026 was meant to be the year of the recovery… and then the war broke out. Kiwi businesses and households have been put on the back foot again… asked to absorb increasing costs again… and forced to restrain spending again. Interest rate hikes will only increase another cost in a cost of living crisis.

The other big news last week was the Government’s 2026 Budget, which delivered no real surprises (other than a bank levy). As expected, set on the backdrop of a global uncertainty, the Budget revealed a short-term downgrade to the economic outlook. However, Treasury forecasts a strong rebound (much stronger than our own forecasts).

“Treasury forecasts show the operating balance returning to surplus in 2028/29 and the government debt curve stopping its rise and heading downwards.”

The OBEGALx (Operating Balance Before Gains and Losses, excluding ACC) is expected to remain in deficit until 2028, and is expected to reach a surplus regardless of the forecast scenario. Read more in our special topic.

Financial Markets

The comments below were provided by Kiwibank traders. Trader comments may not reflect the view of the research team.

Rates – RBNZ week done

Last week was RBNZ week and ahead of the MPS some rates markets traded firm. Reports that there had been some traction on US-Iran talks, despite some headlines indication that the situation in the Strait was not yet stable, alongside an Australian market that had continued to firm post RBA minutes and employment data, saw the local market supported. Receiving interest was noted at the front of the curve, with the implied year-end OCR tracking in the low 2.90%’s. The curve was seen circa 11-points lower in the 2-year and 8-points lower in the 10-year since the Friday close.

Wednesday provided the key releases for the week with Australian CPI and the RBNZ. Our curve opened around 1.75-points higher in a largely parallel move after some overnight weakness in global rates before a weaker than expected headline CPI print a half hour ahead of the RBNZ. This move largely retraced as the Australian curve moved lower, with the priced terminal cash rate moving lower into the mid 4.50%’s. As we had indicated was likely, the RBNZ delivered an unchanged OCR while indicating concern over the risks around inflation. Generally, the statement noted the global uncertainty, the balancing between observed weaker confidence, demand, elevated unemployment and the dampening effect this may have against the near-term inflationary reaction and risks to medium-term expectations if this were to embed. They also noted that the rate path was likely higher and sooner than that set out in the February MPS, with this recognised in the projected cash rate path. They also referenced seeking to avoid unnecessary economic volatility, which we had remarked previously is a consideration in the remit. The decision was a 3-3 split with the internal MPC members siding with no-change, externals looking for a hike, with the split decision a feature of a number of recent central bank decisions of late that emphasised generalised inflationary concern by some members. On to the numbers, the RBNZ’s projected path looked to meet the market for 2026 with the published Q3 and Q4 OCR averages seen at or around the market pricing immediately prior, while Q1 and Q2 2027 were seen around 10 and 20-points below. Reaction on the day saw the curve lift and flatten, with the curve around 3-points flatter 2 to 10-year.

Thursday and Friday activity saw rates trade higher, then lower as the implied OCR pricing continued to incrementally bring forward tightening. There were some headlines around consideration given to 50-point from an MPC member that saw a brief reaction, though a full read indicated the comment may have been part of a wider discussion around certain scenarios, with these later

followed by further headlines from Governor Breman reinforcing the commentary from the statement that while there was some uncertainty around inflation rates were likely to rise. These seemingly imparting more of a reaction to the NZD, with this drawing some support from the reporting, and tracking higher against the USD and the AUD with the cross into 0.8340s on Friday as it appeared that the respective rate paths were now diverging. We had touched on catalysts that may indicate a potential turning point in the NZDAUD with the current environment perhaps something to watch around this. Later in the session the RBNZ GDP now indicator was released which saw the model nudge closer to forecasting a zero print for Q2 GDP – perhaps providing something to watch around rate path.

Currently the implied curve continues to pull forward the rate path, with year-end pricing seen through 3% OCR, with the Q3 and Q4 path largely matching the RBNZ’s forecast averages, market seeing these at 2.53% and 2.86% against the forecast path of 2.51% and 2.84%, while 2027 sees a divergence with the market over the MPS forecast averages by around 15 and 30-points respectively for Q1 and Q2 2027. For the week, with the bring-forward of the forecast OCR path we saw the IRS curve lower and flatter, with the 2-year marked at 3.51% (-5-point w/w) and 10-year at 4.20% (-13-points w/w). Graham Hughes, Trader – Financial Markets.

In currencies - the Kiwi got a boost from a change in tone from the RBNZ:

Last week, the Kiwi dollar opened in familiar territory around the 0.5875 level. Wednesday’s MPS proved to be a game changer, with the RBNZ now appearing likely to hike in either July or September. While the exact timing remains uncertain, the central bank’s messaging was clear: it intends to err on the side of caution and stay ahead of inflation.

The Kiwi subsequently strengthened against the major crosses, moving from a weekly low of 0.5868 against the USD to an initial high of 0.5900, before extending further to 0.5990 by Friday. Ongoing negotiations between the US and Iran helped support positive risk sentiment into the week’s close, providing additional support to the currency. While the broader 0.5800–0.6000 range remains intact, there is scope for further upside from here; however, given persistent global risks, gains are unlikely to be linear.

Over the weekend, US–Iran negotiations continued, but discussions stalled overnight. As has become familiar, markets have reverted to a risk-on/risk-off dynamic, with the Kiwi trading lower at 0.5935 this morning.

Another key Kiwi cross to note is NZD/AUD. After trading near a weekly low of 0.8140, the MPS prompted a sharp move higher, reaching an initial high of 0.8285 and extending to 0.8340 by week’s end. The interest rate differential narrative has narrowed, with the RBNZ now seen as more likely to tighten further, while the RBA may be nearing the end of its hiking cycle after earlier rate increases. This shift in rate differentials is currently supportive of the Kiwi.

Australian CPI data for April, released alongside the MPS, was in line with expectations, with headline inflation at 4.2% y/y, down from 4.6% y/y in March. This further reinforces the relative RBNZ vs RBA policy outlook in favour of the NZD. Looking ahead, Australian Q1 GDP is due for release tomorrow. Mieneke Perniskie – Senior Dealer, Financial Markets.

The Week's Key Events:

- It’s a quieter week on the domestic data front this week. We expect to see international trade data for Q1 of 2026 on Wednesday, building work data on Thursday.

- The war in the Middle East drags on. The tenuous negotiations making headway last week appear to have stalled. We aren’t expecting a swift resolution, but we still hold on to hope regardless.

- Internationally, we have some Aussie data out today including consumer confidence, building approvals and balance of payments data. May CPI for Eurozone is out today as well. Tomorrow, Australia also releases its Q1 GDP data. US data on non-farm payrolls is out on Friday, along with Japan labour cash earnings.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.