- We just can’t seem to go more than a few days without regressing to a state of war. Last week’s headlines were filled with optimistic talk of ceasefires and negotiations. And then the bombs hit, again. The talks are still ongoing, and will likely take every day of the 60 proposed days to get there (properly). It’s not enough to derail the optimisim displayed in most financial markets, however. Oil is trading at $80. There’s no stress in that price. Buit there could be, if talks fail.

- The Kiwi economy’s first quarter report card was released last week. 9 out of 14 industries recorded an increase in output. That’s good. And there was a sense of AI related investment taking place, with a strong boost in equipment, and technology upgrades across the board. Strong investment in computing was a key driver of the quarter.

- The starting point coming into the oil crisis was solid, but not so strong to worsen inflation fears. The RBNZ is all too aware of how dated the numbers are. The potential damage to demand from the increase in oil prices still outweighs the lift in inflation, in our view.

So, the war in the Middle East is back on. We had a short break from all the doom and gloom but we’re back to feeling rather annoyed at the world. Both risk and low(er)-risk assets are up. We have a low volatility index, meaning markets are barely reacting (as has been the story all year). But when markets open for the Northern hemisphere, we might see more action.

Of late, we don’t know where markets get all of their optimism from, especially the oil market. We’ve seen a slight jump in the oil price this morning, it’s up just over $80USD per barrel for Brent Crude… that price doesn’t reflect the reality of oil supply and demand. Fundamentally we have over 1 billion barrels of oil lost this year because of the war in Iran. That’s a massive under-supply that global oil-reserves (as well as price) has managed to buffer us against. But global oil reserves are getting low. We are at a tipping point. Once the reality of the oil shortage starts to be reflected in the oil price once again, we could be facing those worst-case scenarios of $150-$200 USD per barrel prices. Domestically that means uncertainty is back on the menu. With the war back on and an election looming, businesses have to be resilient to get through the rest of the year.

We had solid GDP results from the first quarter of the year, out last week. We got a 0.8% growth in the March quarter. We also had a revision to the 2025 December quarter (up to 0.5% from 0.2%), placing the economy in a strong position. Economic activity lifted 1.5% over the year. But that was before the oil crisis. Most of the strength has been driven by demand for machinery and equipment. Some of that being computing equipment. There may be some AI related activity beginning to show here.

It would have been a beautiful start to the year – if not for the war in Iran destroying some of this progress. The biggest drag on the economy is construction. Down 1% qoq, and driving 0.1% of the overall GDP down with it. No surprises there, given the rhetoric we’ve been hearing from the construction industry.

The question now is, how much of this momentum can be sustained through the crisis? The data from the second quarter of this year will give us a good indication. The GDP now-cast has been on a down-trend until last week, indicating some strength remaining.

Last week, 4 out of 5 Central banks internationally held their rates steady, including the Fed. Japan hiked their interest rates by 25bp, showing resolve. No domestic data out this week. We’ll watch for the CPI data out of Canada, Australia and Japan this week. S&P Global PMI out tomorrow as well, alongside lots of activity data out of the US late in the week.

Financial Markets

The comments below were provided by Kiwibank traders. Trader comments may not reflect the view of the research team.

Rates – Soothing words for the hawks

It was a wide-ranging week for rates, driven by data, geopolitical developments, and key central bank decisions.

Monday saw yields trade lower amid headlines around a US–Iran deal and softer domestic services data, pushing the implied OCR path and term rates lower. This move received was supported by US rates futures, which opened firmer in their first session of the week, particularly Fed Funds futures, moving to slightly reduce the priced expectation of a tightening. By day’s end, the December implied cash rate approached 2.85%, supporting the front end (2‑year IRS -7bps, 10‑year -5bps).

Tuesday saw attention on domestic data and the start to central bank releases. Selected prices indices were released alongside the food price index, again broadly showing a degree of containment in price inflation, supporting the front of the curve. Focus then shifted to the start of the central policy decisions, with the BoJ, as expected, lifting rates, followed by the RBA after our close remaining unchanged also as expected. The RBA, while tipping their hat to hikes so far and the subsequent tighter conditions slowing the economy, continued to warn on inflation, reinforcing that the Board remained focussed on ensuring that inflation would not become embedded. The commentary was broadly expected given the recent remarks from various Monetary Policy Board members including the Governor herself on the risks of embedding, with their curve rallying post-statement.

Wednesday saw our curve open firmer, playing catchup to Australia, with current account data on the schedule but taking a bit of a back seat to the upcoming Fed decision and Q1 GDP. The implied OCR path continued to price lower, with the market path further through the forecast as per the May MPS, with the December implied OCR sinking to around 2.79%, or just over two 25-point tightenings. The average Q4 2026 and Q1 2027 cash paths consequently indicating deviation from the MPS, with these some 15 and 11 points below the MPS – perhaps leaving these vulnerable to retracement. Swaps traded lower, with 2-year to the mid-3.20%s with some paying interest emerging around those levels.

Thursday morning was the action point for the week, with the Fed decision and domestic GDP. While there was expectation for an unchanged Fed, risk lay with the accompanying statement being less doveish than would be expected from newly appointed Warsh. As it unfolded, it was seen as hawkish and rightly so, a shorter statement finishing with the soothing words that “the Committee will deliver price stability.” The associated ‘dot-plot’ also scared the horses with the updated FOMC participants’ assessments of appropriate monetary policy sharply higher for the 2026 and 2027 years, seeing priced expectations for a 2026 tightening jump through 100% for +25-points, with Treasuries higher in yield, 2-year for example around 15-points higher at around 4.21%.

This was followed by an okay +0.8% Q1 GDP print, that combined with prior period upward revisions likely saw the economy in a firmer starting position ahead of the outbreak of the conflict. With the domestic market perhaps already trading at the rich end with only just over two 25-point moves priced by year-end, the Fed decision and outlook with GDP saw our market retrace, moving higher and flatter on the day, with further paying interest noted up the front. Implied year-end OCR tracked back to 2.90% as the Q4 and Q1 gaps noted above looked to narrow, 2-year IRS finishing 9-points higher at 3.37%, 10-year at 4.07% (+4).

Friday proved to be a more subdued rates session, with the curve finishing mildly higher, though off session highs, 2-year finishing the week at 3.38% (-2 w/w), 10-year 4.07 (-7 w/w), with December OCR seen at 2.91% and June 2027 pricing around 3.20%.

Developments were broadly unfolding in line with those assumed in the last MPS – a resolution to the conflict and shipping via the Strait to resume, Q1 GDP indicating a reasonable starting position for the economy, and with market cash-rate pricing largely in line. While you would not likely want to entirely rule out a chance of a pause in July, the dataflow and events probably provides a degree of comfort to the RBNZ to start to a gradual removal of the current accommodative policy. With the December pricing moving back to around 2.90%, we would anticipate the potential for this to resume cycling around the 2-plus to 3-plus 25-point tightenings as the central year-end case depending on dataflow and events. This cycling may still provide short-end accrual opportunity for opportunistic participants. Further, if indeed we do see a start of a tightening cycle, discussion will likely centre around determining a terminal rate. While currently June 2027 pricing sits at around 3.20% provides a good fit with the MPS projections, variations of shorter term forward-starts may indicate that this may be a little low compared to market – this may be worth keeping an eye on, if at least for interest. As is always the case of late, there will always be a disclaimer around event-risk over the weekend. Graham Hughes, Trader – Financial Markets.

In currencies - the Fed was the driver last week:

The Kiwi dollar was under pressure last week, driven by broad US dollar strength. The Federal Reserve meeting was the key event; while the Fed held rates as expected, the relatively hawkish tone saw markets further price in the potential for rate hikes later this year, with cuts pushed out to late 2027. NZD/USD opened the week just shy of 0.5850 and traded lower into the FOMC, falling sharply to 0.5760. The GDP release provided a modest lift to 0.5798, but the move ran out of momentum against the stronger USD, with the pair closing the week at 0.5736. With a US holiday on Friday, trading conditions were thin, offering little additional direction.

While the Kiwi was on the back foot last week, expectations for RBNZ tightening in the coming months remain firmly intact, reinforced by a stronger-than-expected Q1 GDP print, which added confidence to that view. This week begins with the risk of further escalation in the US–Iran conflict, rather than the anticipated progression towards a formal agreement. Volatility remains contained for now, despite a modest uptick in oil prices.

NZD/AUD also moved lower last week, partly reflecting the lingering hawkish tone from RBA officials following their decision to remain on hold. Upcoming Australian data (including CPI) is more likely to provide support for the AUD in the week ahead, particularly given the limited domestic release calendar in New Zealand. Mieneke Perniskie – Senior Dealer, Financial Markets.

The Week's Key Events:

- Not much domestic data out this week, so we keep our eyes peeled for international data this week.

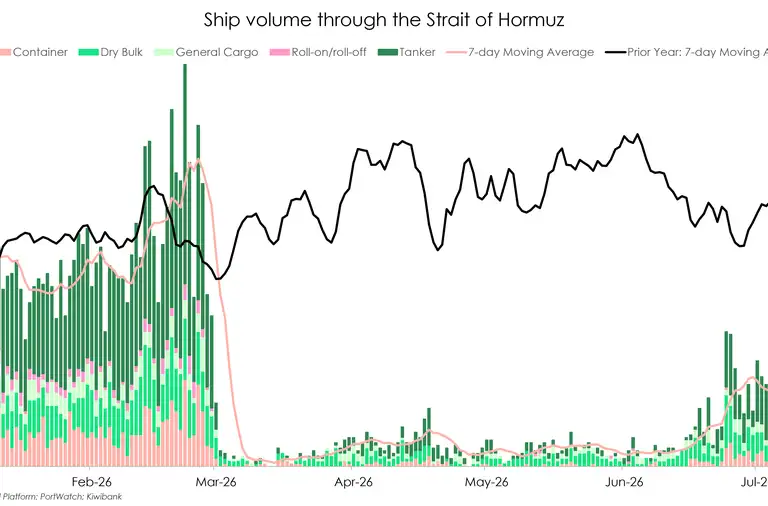

- The war in the Middle East is back on. Israel has violated the cease-fire. Iran has blocked the Strait of Hormuz again. Global uncertainty is high, but volatility is low. We wait for the Northern hemisphere to wake up and markets to re-open before we can fully assess the damage.

- Internationally, we are keeping an eye on Canada, Australia and Japan. All of which have CPI data out this week. S&P Global PMI out tomorrow as well, alongside lots of activity data out of the US late in the week.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.