The March GDP release was better than expected. A modest yet solid 0.8% lift in activity printed for the March quarter. With a revision to the 2025 December quarter (up to 0.5% from 0.2%). Economic activity lifted 1.5% over the year.

Most industries saw an increase in output (9 out of 14). With the strength in today’s report coming from equipment and technology upgrades across the board. Strong investment in computing also helped drive up the expenditure side of GDP.

Fist we look back. Around 75% of the up-ward revision to the Dec quarter was due to revisions to building activity estimates, which came in stronger that first estimated. The remainder was mostly due to revisions to agriculture estimates.

From the Reserve Bank’s perspective, the economy was moving along nicely on its growth trajectory before the war, but not heating up too much. That’s key. Modest growth does not stoke inflation fears.

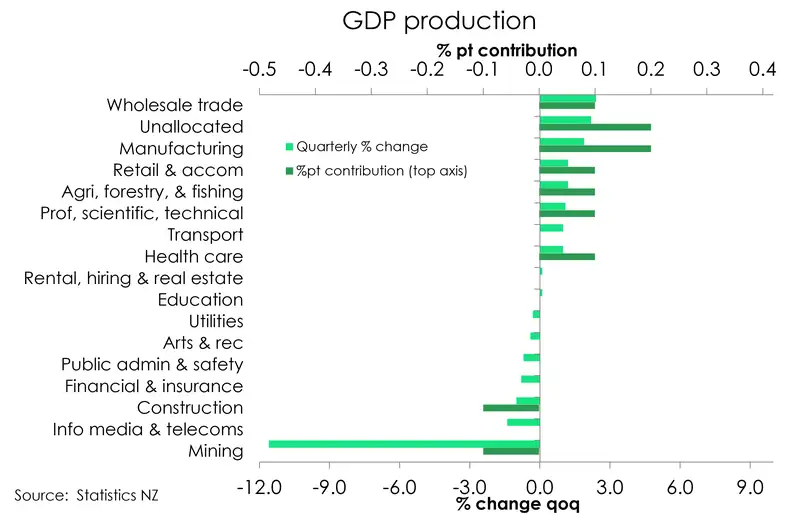

What’s behind the growth? Nine of the 16 industry groups showed solid gains. One of the biggest industries to grow, was manufacturing, up 1.9%. This contributed 0.2% to the overall quarterly growth rate. Driving this, was transport equipment and machinery manufacturing.

Wholesale trade, also driven by machinery and equipment wholesaling, was up 2.4%, contributing 0.1% to growth.

Business services were also up 1.1%, in part driven by computer system design also contributing.

This movement all points to one source: AI. With computing services up, along with purchases of computing hardware, it’s hard not to make assumptions. Our crystal-ball gazing tells us that we have the AI revolution to thank for some of this growth.

On the expenditure side, we saw a 1% lift in activity, compared to the December quarter of last year.

We had a large up-tick in plant machinery and equipment (5.5% qoq), largely driven by computers, including imports. Expenditure on transport and equipment lifted 6.7% qoq, a huge jump from the -11.4% we saw in December. Business investment also saw an up-tick of 3.7%... All roads lead to Rome, or in this case, (hopefully) technological advancement.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.