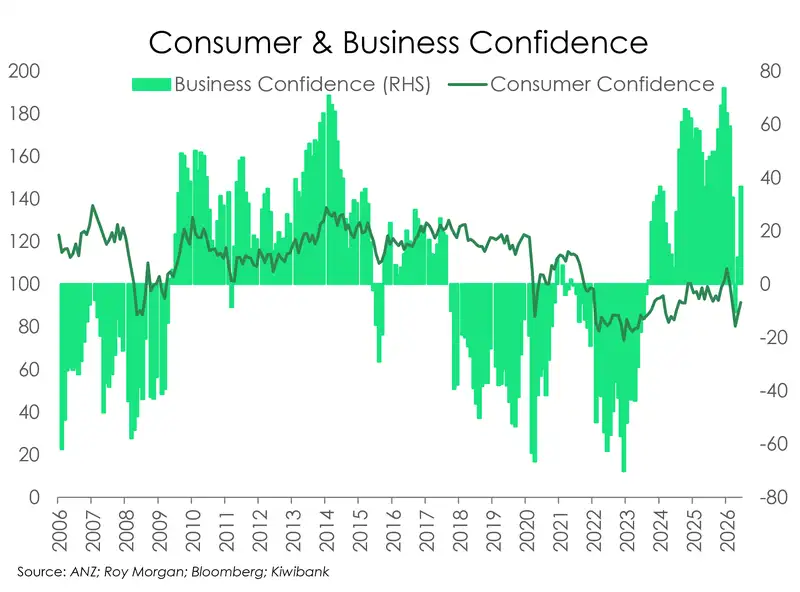

As our chart of the week shows, business confidence has surged over the past two years. Lifting to levels not seen since the post-pandemic reopening period and approaching highs last experienced during the mid-2010s. Firms have been increasingly optimistic about the outlook, helped by falling interest rates, easing inflation pressures, and expectations of a stronger economic backdrop ahead.

Consumers, however, remain considerably more cautious.

While consumer confidence has recovered from the lows reached during the most recent cost-of-living crisis, it remains subdued by historical standards. The gap between business and consumer sentiment is now among the widest seen outside of the extraordinary COVID period.

The divergence is telling.

Businesses tend to look forward. Lower borrowing costs, improving profitability expectations, and a better outlook for activity over the next year are providing reasons for optimism. Households, on the other hand, are still dealing with the legacy of the downturn, falling house prices, and cost of living pressures. Mortgage repricing, weak income growth, elevated living costs, and a soft labour market continue to weigh on confidence and spending decisions.

This split explains much of the current economic landscape. Despite a sharp improvement in business sentiment, consumer spending has remained lacklustre. Retailers, hospitality operators, and discretionary sectors continue to report challenging conditions even as broader measures of business confidence point to better times ahead.

The key question is whether consumers eventually catch up to businesses…

Historically, sustained recoveries have typically required both households and firms pulling in the same direction. Businesses can invest and hire based on expectations, but ultimately stronger demand from consumers is needed to validate that optimism. Encouragingly, consumer confidence has been gradually trending higher over the past year, suggesting households are beginning to feel some relief from lower inflation and easing monetary conditions.

For now, the chart highlights an economy in transition. Businesses appear increasingly convinced that the worst is behind us. Consumers remain less certain. Closing that confidence gap may be one of the defining features of New Zealand's economic story over the coming year.

Most recently, the oil crisis has put doubts in both consumers and businesses minds about how well a recovery will be sustained. Recent progress in the Middle East and news of the Strait of Hormuz re-opening, alongside a large drop in oil prices, have seen both groups rebound. Although not as high as before, this is movement in the right direction. It shows that despite the divide, businesses and consumers may be moving in lock-step going forward.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.