The Middle East conflict is still playing out. Over the past few months, it’s been a rollercoaster that the world has, willingly or not, been forced to ride.

One of the core metrics showing the impact of this conflict is the oil price. Oil prices flow through to the price of other goods including plastics, transportation, and refined fuels. Central banks are therefore wary of oil price spikes.

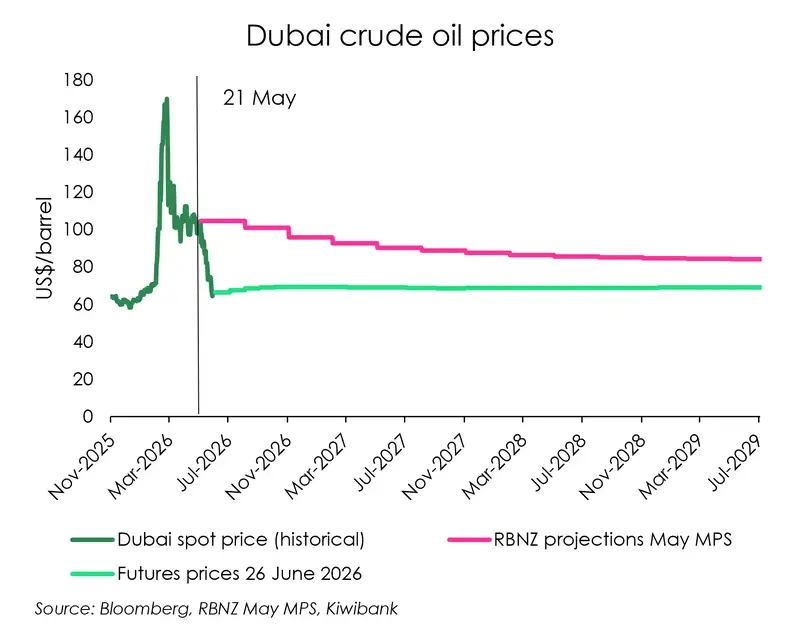

In May, the RBNZ, assumed a gradual decline in oil prices over several years. Based on current evidence, this is proving far too pessimistic.

The spot price of Dubai crude oil spiked dramatically because of the Middle East conflict. The price reached just shy of $170 US/barrel in March. This posed a significant concern to central banks, including the Reserve Bank of NZ. The price of oil flows into the cost of doing business, through elevated petrol, diesel, jet fuel and other petrochemical costs. A spike in oil price means a spike in the costs of these inputs and, eventually, goods and services.

In May 2026, markets were expecting oil prices to remain elevated for a long time. This informed the Reserve Bank’s central projections. As the chart shows, the spot price has fallen sharply on hopes of a peace deal being struck between Iran and the US. Now the market is predicting that the rollercoaster ride is at an end. The futures curve is substantially more optimistic than it was a month ago. This changes the Reserve Bank’s underlying assumption for oil pricing significantly.

Of course, this is simply a snapshot of the market at a particular point in time. If the events of the 2020s have taught us anything, it is that things can change without notice. The renewed tension in the Middle East over the weekend is one example of this. The futures pricing shown in this chart doesn’t yet reflect these most recent events. This is one of the few drawbacks of New Zealand being ahead of the rest of the world!

Regardless, the world is in a very different place to when the Reserve Bank was publishing its May forecasts. Oil prices are a lot lower. The market is expecting much lower prices out to the end of the decade. These data points give us confidence that medium term risk from tradeable inflation remains low. The Reserve Bank would be wise to hold rates rather than hike. We need to give the Kiwi economy more space to breathe.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.