- Another week of rolling the dice on the conflict in the Middle East. This time we hit a ladder, as a peace deal looks more likely. But there are snakes in the grass, and downside risks are not off the table. US equities are rallying and the oil price is falling. We hope that President Trump follows through on his peace promises.

- We have a big week for central bank decisions. Our nearest neighbour, Australia, looks likely to hold its cash rate steady after delivering three hikes this year. The BoJ more likely to start hiking than not. The Fed has a lot of eyes on it, with new Fed chair Kevin Warsh commenting that a hike is not out of the question if it’s needed. Finally, Bank of England and Swiss National bank, both likely to hold at the end of the week.

- The Kiwi economy is still tracking sideways. The GDP report card for the March quarter will tell us more. Although out of date, this data will strengthen or weaken the RBNZ’s resolve to hike rates in July, but not as much as the Food Price and Selected Price Indexes.

More of the same, volatility is the new certainty. The War in the Middle East appeared to be escalating last week, until an abrupt shift bolstered markets. US President Trump cancelled planned attacks on Iran and signalled that a peace deal was ready to be signed. Although we have yet to see that happen… we hold out a tiny bit of hope.

On that news, US equities rallied sharply. An end to the war is good. The S&P 500 posted its strongest gain in two months. We also had the SpaceX IPO last week, on the NASDAQ, raising $75bn. Completely shattering the record IPO from Saudi Aramco in 2019 (29.4billin) by 155%.

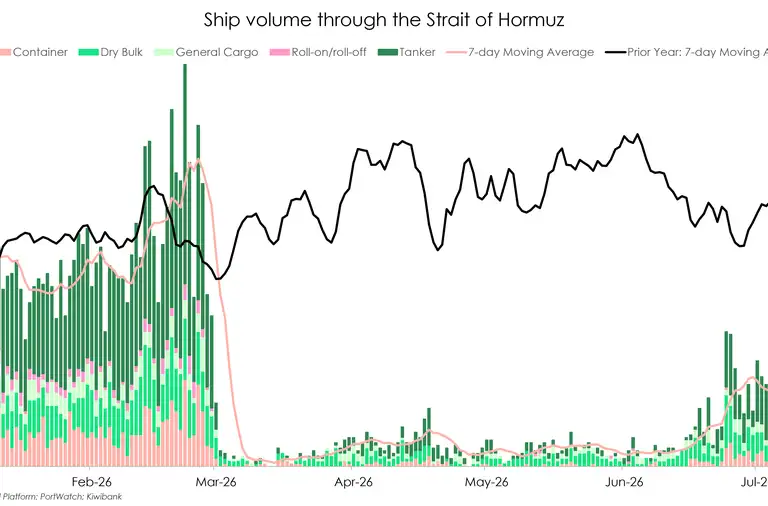

The price of Brent crude has dropped below $90USD per barrel for the first time since March. Currently sitting on $87.3USD, markets are quickly pricing in a resolution to the war and a re-opening of the Strait of Hormuz.

It’s a central bank mega week this week. Starting with the RBA decision tomorrow, most are expecting a hold. After delivering 75bps of tightening this year, Australia hopes to have tamed the inflation beast for a time, although another hike is not out of the question. The Bank of Japan is only just starting it’s tightening. They are expected to deliver a 25bp hike this week. In the US, debate is abound on moves from the Fed later in the week. Most are expecting a hold, but all eyes are on Kevin Warsh’s first meeting as Fed chair – markets will be sensitive to the rhetoric that comes out of that meeting. Finally, we end the week with Bank of England and Swiss National bank, both likely to hold, but hawkish in their most recent commentary.

Back home, we had some migration data out last week. Net migration is still looking strong – better than we hoped coming into this oil crisis. April data showed short-term visitor arrivals passed 3.65m, that’s 93% of pre-COVID arrivals, and up 8.4% yoy. However, some downward revisions have weakened the underlying improvement. We expect that the conflict in the Middle East will have a negative effect on tourism. High fuel costs continue to erode budgets and uncertainty weighs on travel plans. That is, unless the war really does end this week… only time will tell.

As for data out this week, the GDP report card for the first quarter of the year is due on Thursday. We ended last year with very little wind in our sails. The GDP report card for December was modest. Economic activity lifted 0.2% over the December quarter, 1.3% over the year. This took some of the optimism out of our estimates. We are expecting a stronger lift on a quarterly basis, of 0.7% for the March quarter, but a soft 0.9% over the year.

We are keeping a pulse on the high-frequency data and we know to expect an even softer June quarter, that will be the important stuff… but alas, we won’t have that for a while yet. The Q1 GDP data will strengthen or weaken the RBNZ’s resolve to hike rates in July. A weaker GDP print coming into the year means weaker demand and thus lower inflation pressure before the oil crisis. In all fairness, the Food Price and Selected Price Indexes (SPI), will be more important to the RBNZ. The SPI acts as an early indicator for quarterly inflation, tracking everyday costs like food, housing rent, fuel, and airfares. That data is out on Tuesday.

Financial Markets

The comments below were provided by Kiwibank traders. Trader comments may not reflect the view of the research team.

Rates – Central bank roundup

Rates opened the week higher after the strong US payrolls the Friday prior. With the Treasury curve around 10-points post release and Fed Funds futures siding more strongly on the side of 2026 tightening, our curve opened higher. Though initially tempered somewhat by an Australian holiday that saw a curtailed Australian futures trading session on their key benchmark three and ten-year government bond futures. By the end day the IRS curve was around 8-points higher 2-10-years, while the implied December pricing that had dipped below 3% at the prior Friday traded back through this level. That was the broad highpoint on rates for the week. The local market taking some direction from a rallying Australian market after what appeared to be a stampede of banks calling the end to the RBA tightening cycle. This sentiment was added to with the reporting that a deal was imminent around potential resolution to the Mid-East conflict. This alongside some local releases that printed softer resulted in an ongoing receiving interest in our market, with the manufacturing PMI which had held up reasonably well printing sub-50, and RBNZ’s own GDP now predictor model resuming its downward trend, with the latest print indicating -0.2% for Q2 at the end of the week. Here for the week NZ 2-year IRS finished at 3.40% (-7-points week on week), and 10-year at 4.14% (-7 w/w).

This week there are a number of key central bank policy decisions due, including the BoJ, where it is widely expected that the central bank will lift rates despite the Governor being hospitalised and reportedly not partaking in the vote. The US Fed where they are expected to hold though with the data flow of late generally printing on the firm side although balanced to a degree with pricing aspects typically showing some containment – here prices paid components in ISM survey data and the core CPI read, and the RBA which is expected to hold. While the Fed is seen on hold in the near-term, priced expectation continues to side on that of tightening, with a 2026 move seen at around a half-chance even after the potential Mid-East agreement re-rate of probabilities.

For our rate markets, we see some reasonable domestic data flow to add to our picture of the economy. The selected price indices released alongside the food price index is due early in the week, and this remains of interest given that broadly so far, pricing pressure has appeared to be contained to those sectors with direct exposure to fuel. The emergence of any second-round pricing effects will be watched for. GDP for Q1 is also due and while this figure may be dated given events towards the end of the quarter, it may still have some clout as a starting point read on the economy largely prior to the start of conflict – so any material divergence from expectation may drive a reaction. Assuming ‘normal’ prints and as we have noted previously, we would still anticipate that the net of all these is likely to see our implied pricing continue cycle between around 2.90% and 3.10% OCR for the year-end, with this likely providing an anchor of sorts for the front of the rate curve. For the RBNZ, a potential deal on the Mid-East situation may provide some comfort in starting a cautious tightening cycle in line with their last projections. Graham Hughes, Trader – Financial Markets.

In currencies - Central bank expectations and truce talks were the driver:

Last week, the Kiwi started on the back foot following a much stronger-than-expected US non-farm payrolls print. With expectations for rate cuts giving way to the potential for rate hikes from the Fed, interest rate differentials became the primary driver for currency markets at the start of the week. The US CPI print came in broadly in line with expectations, while the PPI print at the end of the week was slightly higher, further supporting the US dollar. The ECB lifted its cash rate to 2.25% as expected, giving the euro a modest boost. However, with the hike already priced at a 99% probability, the focus shifted to the ECB’s forward guidance. The Kiwi dollar spent most of the week trading near 0.5800 and was capped at 0.5840. Towards the end of the week, market participants focused on news that the US and Iran were close to signing a deal. This pushed the US dollar index back below the 100 level into the close. Whether the deal is ultimately signed is still uncertain, with tensions remaining elevated.

The Kiwi largely traded on headlines, closing the week at 0.5833. NZD/AUD moved higher over the week, rising from 0.8245 to 0.8295 before closing at 0.8278. For now, the cross is being supported by interest rate differentials, with the RBNZ expected to hike in July while the RBA appears to be on hold, despite some lingering hawkish commentary from officials.

Looking ahead, the RBA delivers a rate decision tomorrow. The Bank of Japan is also in focus this week, with a hike expected, alongside the Federal Reserve. While the Fed is expected to hold, attention will be on the tone of the statement, particularly as this marks Governor Warsh’s first FOMC meeting. We also have New Zealand’s Q1 GDP print due this week. While it is unlikely to move markets given the lagging nature of the data, a stronger-than-expected result could provide some support to the Kiwi via shifting RBNZ expectations. Mieneke Perniskie – Senior Dealer, Financial Markets.

The Week's Key Events:

- We have some data to watch this week. Food Price and Selected Price Indexes (SPI) will be important for the RBNZ. That data is out on Tuesday. Thursday, we have March quarter GDP for 2026, another early indicator of inflation pressures going into the war in the Middle East – but outdated data regardless.

- The war in the Middle East appears to be over (finally). Both Iran and the US have publicly stated that a peace deal has been signed, with the dirty details due to be released this Friday (US time). Markets are expecting a very favourable deal, with an opening of the Strait of Hormuz a major sticking point.

- Internationally, we have a central bank mega week. Starting with the RBA decision tomorrow, most are expecting a hold. The BoJ is only just starting it’s tightening. They are expected to deliver a 25bp hike this week. Most are expecting a hold from the Fed, but all eyes are on Kevin Warsh’s first meeting as Fed chair. Finally, we end the week with BoE and Swiss National bank, both likely to hold.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.