- The war in the Middle East is still going… we feel like we’re in purgatory. The market is barely reacting anymore. The price of Brent Crude seems to have found a range around $100USD per barrel. And oil prices are ready to take off or plummet depending on the next headline.

- Domestically, the labour report card showed significant slack. Our unemployment rate eased a bit, from 5.4% to 5.3%, with signs of recovery. But the uncomfortable number of underemployed people, still waiting in the foyer, continues to put downward pressure on wages. And the slack in the labour market reduces future inflation risk.

- That leaves us in an uncomfortable place. The fuel (supply) crisis is pushing prices up, and the weak economy (demand) is pushing prices down. Our view is that the weak economy will outweigh the temporary price shock. The economy likely contracted in Q2, and we don’t need more weight to an already weighed-down economy.

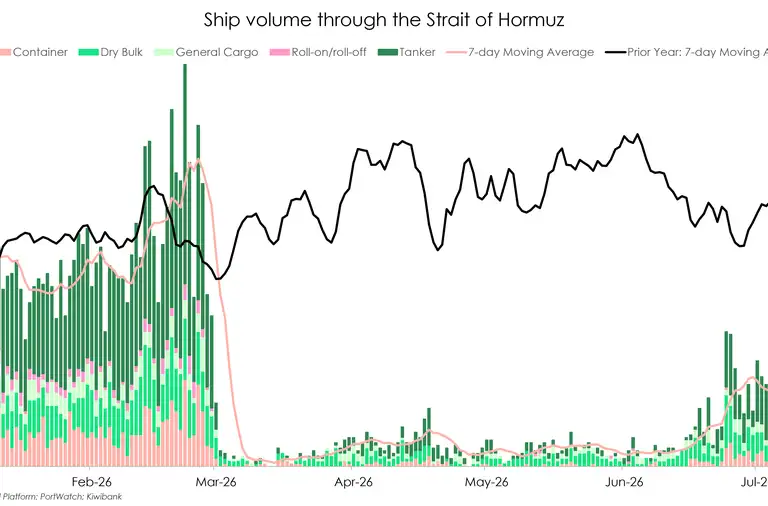

International news is no news because despite the minutia of the headlines, nothing has changed. The Strait of Hormuz is still blocked, both Iran and US are still posturing and threatening and firing at one-another.

Is a peace treaty coming soon? No one knows…

The price of brent crude is hovering around $100USD per barrel, ready to go higher if tension escalate or lower if they ease. And we’re likely to see both upward and downward surges, as the headlines contradict.

Across the ditch, Australia’s reserve bank hiked their rates last week for the third time in a row. But they are in a completely different boat to us. Their inflationary pressures were building long before the oil crisis hit. We’re not looking to follow in their footsteps.

The domestic rates market has come down slightly, but not enough. Traders are still pricing in a full rate hike in July – consistent with what some are calling for. Not us. The market has 4 rate hikes (100bps) priced in by February. We believe we need zero… none… nada. Wait and see.

The labour market report card was the most notable data out last week. We got a 5.3% unemployment rate to start 2026, down slightly from 5.4%. It was not earth-shaking. With the labour force also shrinking, the number of unemployed individuals didn’t actually fall. And the measure of greater slack in the market, the underutilisation rate, remained at an elevated 13%. That’s too high, and shows weakness.

We see slack in the labour market worsening, with the demand destruction caused by the spike in fuel prices. Wage inflation is already low, at 2%, and puts disinflationary pressure on the economy. When we have so many Kiwis looking for more hours to work, there is little bargaining power for a pay rise. This is in the environment where we are facing an economic contraction due to the destructive power of the oil price spiking.

The space between what we could be producing as an economy vs what we are producing is widening. That’s more disinflationary pressure in the mix. Many businesses are postponing expansions; Kiwis are putting off big projects in part due to the temporary(?) increased costs of petrol/diesel etc. And that makes sense. Uncertainty is high, the costs of doing things are high. The wait and see approach for non-urgent work seems wise.

That leaves us in an uncomfortable place for the time being. Higher prices due to the oil crisis, lower demand due to decreased demand in the economy. That’s dangerous. That’s moving us closer towards stagflation, a beast that’s notoriously difficult to tame. It all hinges on how long we will face elevated prices for, and how long they will stick around once the crisis is resolved.

Financial Markets

The comments below were provided by Kiwibank traders. Trader comments may not reflect the view of the research team.

Rates – Local price series data of interest

Last week, for our rates market, aside from the ups and downs of conflict related headlines, the focus shifted to that of a little more local with the RBA policy decision, NZ employment data, and the chance of some additional insight from RBNZ MPC member speaking engagements and the delivery of the Financial Stability Report.

Monday saw the IRS curve open around a ¼-point lower initially then slowly eked out some further mild gains on conflict-related headlines, trading around 2 to 2¼ points lower by mid-morning. News service headlines from an RBNZ MPC committee member Prasanna Gai speaking engagement that supply shocks like Hormuz raise the neutral rate did result in some reversal, though this move faded as upon a full read was part of a far longer more theoretically focussed presentation. Tuesday saw the curve open small higher in line with international moves, though within narrow ranges ahead of the RBA and with the ‘hawkish hold’ playbook having been largely adopted the week prior by central bank decision-makers, the market was attentive to the chance of similar adoption by the RBA despite the hike around 75% priced. The RBA hiked, as expected, in an 8-1 decision, against 5-4 last time, though did flip the playbook with what read as a strict statement unwound to a degree with a more neutral press conference – a ‘doveish hike’ so to speak. Australian rate reaction was a swift rally with short to mid dated IRS gaining most traction, 2-year at one stage marked lower by 7-points on the day, and 3-year lower by 10-points, though with all this occurring after our close.

Wednesday, the release of the RBNZ Financial Stability Report barely impacted ahead of employment data, with the focus of the report unsurprisingly on financial stability, though perhaps of interest was the use of the past-tense when referring to growth in the economy and the expectation of a somewhat slower recovery. Employment data followed, printing better than consensus expectation at 5.3%, though this was through the participation rate, and if adjusted for that would have resulted in a small above expectation print, which better aligned with the quarterly and annual employment change undershoots. The day finished small higher in yield, with the 2-year IRS around 3.55 (+2) and 10-year 4.30 (+1), while the implied path continued with its aggressive pathway. Post the RBA, their implied curve continued at cap at around a 4.70 terminal rate, implying circa 1½ 25-point moves, though economist surveys started to side on unchanged policy for 2026, while the NZ implied curve only modestly pared back expectation by a few points, still retaining near five 25-point moves in the next seven meetings as the priced base case. By Friday close, the curve had ground its way higher, including after a domestic bank now indicated a Q2 contraction was on the cards, with a pronounced steepening on the day despite some noted paying of shorter runs out of forward dates, with 2-year IRS marked at 3.55%, +3 on the day and +1 for the week, and 10-year at 4.34% +7 d/d, +2 w/w.

For the coming week, the prior comments around the likely ranges and drift sideways with time still hold with reads on the strength of the economy and business and consumer measures still indicating a sharp weakening of confidence and expectation, while offset by current known inflationary impacts though with less certainty over whether or if these prove to be persistent or transitory. As such, data flow locally including the RBNZ 2-year inflations expectations survey and selected price series data (SPI) may be of interest, alongside any comments from Dr Breman at an offshore panel discussion where ‘Risk management in an uncertain world’ is the topic. This week however, time is likely that conflict related headlines could reinsert themselves a little more into the trading view this week. g. Graham Hughes, Trader – Financial Markets.

In currencies - When fundamentals don’t make sense – maybe the tea leaves can tell us something:

A record run in global earnings growth continues to overshadow broader macro concerns, including ongoing tensions in the Middle East. That dynamic has kept risk appetite firmly supported and has once again worked in the Kiwi’s favour. Over the past week, NZD/USD rose 1.6%, making it the standout performer across the G10 currency space. The Kiwi also outperformed the Australian dollar as markets absorbed what was ultimately a not so hawkish RBA rate hike. While the RBA did tighten policy, the tone and accompanying guidance reinforced the growing sense that the hiking cycle may be closer to its end than its beginning. That shift has prompted renewed interest in NZD/AUD, with the cross pushing up to a 0.8247 high and perhaps providing early signs that a base may finally be forming in what has been a heavily sold trend. In the US, Friday’s payrolls report had little meaningful impact from an FX perspective. More broadly, however, the continued resilience of the US economy remains a double edged sword for the USD. While firm growth is supportive for the currency at the margin, in the current environment it is also reinforcing broader risk sentiment, which continues to favour higher beta currencies over outright USD strength.

Looking ahead, domestic data takes centre stage with inflation expectations alongside SPI and food price data due. These releases will be important in either validating or challenging the market’s still elevated short term interest rate pricing, which we continue to view as expensive. From a technical perspective, NZD/AUD is showing tentative but improving signs. A sustained push through 0.8260 would open the door toward 0.84, supported by improving technical momentum, stretched positioning, and the possibility that the divergence between NZ and Australian cash rate paths is beginning to narrow. If 0.8174 proves to be the broader cycle low, a clean break above 84 cents would expose retracement potential toward the mid 0.86s.

Meanwhile, NZD/USD’s break back above the 0.5920/30 region is a notable development. From a structural standpoint, the Kiwi has once again pushed back above its broader five year downtrend, further reinforcing the medium term recovery narrative. The next upside focus sits around 0.6090, while on a longer dated, multi year horizon, the 0.6300 area remains a credible — albeit distant — upside target should the recovery continue to gain traction. Hamish Wilkinson – Senior Dealer, Financial Markets.

The Week's Key Events:

- Domestic data to watch for this week includes RBNZ 2 year-ahead Inflation Expectations, monthly food prices for April and BusinessNZ Manufacturing PMI. We also have RBNZ Governor Breman speaking on a conference panel on Tuesday.

- The war in the Middle East is still going. With no end in sight, unless you believe Trump’s posturing. The ceasefire agreement is holing despite both sides exchanging fire over the weekend.

- International data to watch. Inflation data out this week for the US (Wed) and China (Mon). Australia has some monthly business confidence and consumer confidence data to report as well, off the back of a tightening from the RBA last week.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.