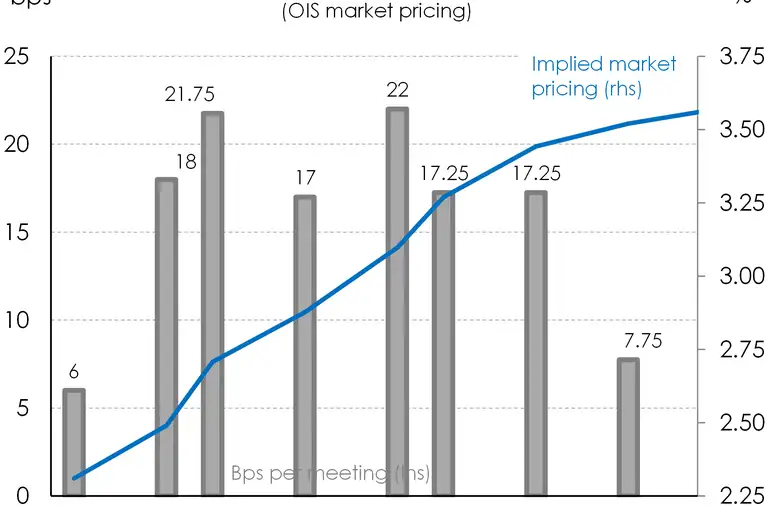

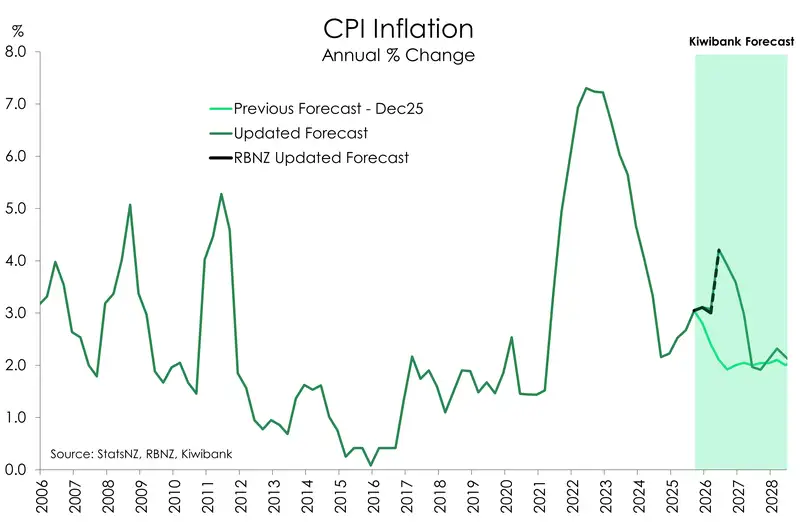

All eyes are on the inflation numbers out next week. The starting point for 2026 is likely to be 3.1%, the same run rate we finished 2025 on.

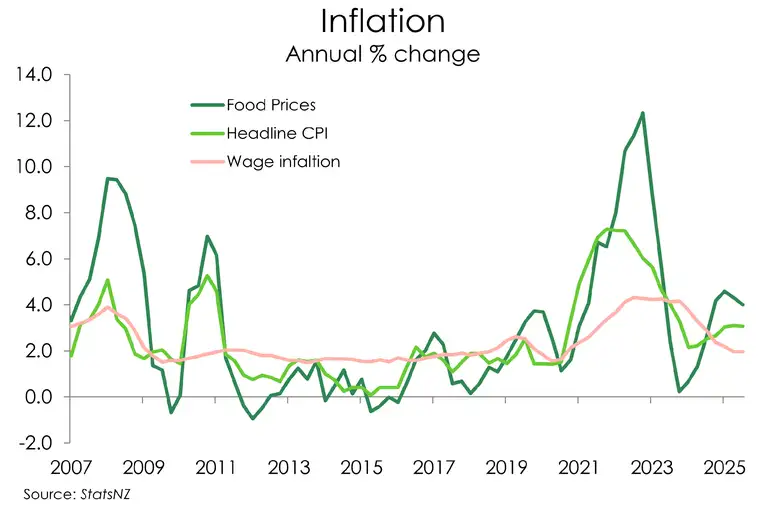

Before the war in Iran, we expected to see headline inflation decrease. We knew the rate was driven, in part, by higher administered costs like council rates, electricity and the like. Underneath, excluding food and energy prices, core inflation held at 2.5% after being on a general downtrend since hitting the peak in late 2022. Trimmed mean, another way of excluding volatility in inflation, accelerated to 2.8% from 2.5%. Without a strong demand-side growth story to tell, the increased prices weren’t the best news. We hoped that 2026 would finally be the year where growth caught up with prices.

We’re now less optimistic. Businesses and households are facing yet another cost in a cost-of-living crisis. Demand destruction is our biggest concern. The downside risk to global and domestic growth can’t be understated here. The IMF and other forecasters have slashed global growth forecasts. That’s worse than good. Until the conflict in the Middle East is resolved, we will continue to see the cost of oil and oil-derived products remain elevated. And this is severely impacting industries heavily reliant on diesel.

The March 2026 quarter only got to see the very beginning of the oil crisis, so we don’t expect next week’s numbers to show much price pressure. The June quarter is when the true impact will be felt.

The war in Iran broke out on the 28th of February, but the real impact didn’t hit our shores until mid-March, when we started to see petrol prices increase. That means only 1/6 of Q1 was affected (2 weeks out of 12).

We’re playing it by ear and making some adjustments to our Q1 CPI forecasts. We’re expecting a chunky 0.9% over the first quarter, keeping the annual rate at 3.1%. That is significantly above our original forecast of 2.4% for the March quarter.

Last quarter, we were concerned that administered costs were not the only costs pushing higher. When we removed these (mostly) government charges, inflation was still pushing up – from 2.4% to 2.6%. Other hot spots within the CPI basket included an a-typically expensive retail sector. The holiday-period “discounts” left us feeling very disappointed. The percentage of retail goods that were discounted over the 2025 December quarter dropped to just 15% down from 20% the same time in 2024. For household furniture specifically, the average discount was just 3% compared to the 11% in December 2024. Discounts in 2025 just didn’t stack up to previous years. Instead prices for clothing & footwear increased 0.8%, while household contents & services lifted 0.6%. Both stronger prints than we had expected.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.