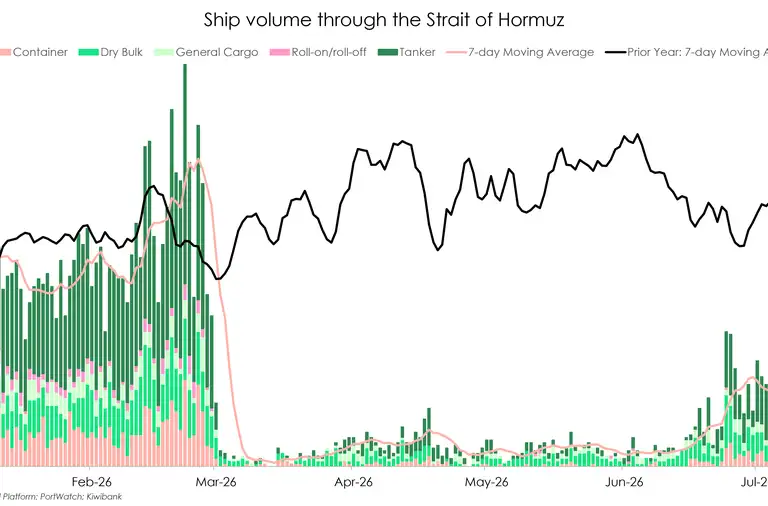

- Last Wednesday we were cautiously celebrating, after five weeks of the Middle East war, a cease-fire agreement was welcome news. But the re-opening of the Strait of Hormuz hasn’t eventuated. Oil tankers are still unable to flow through the Strait. And peace talks failed over the weekend. The ups and downs from the war continue to dominate the headlines, and financial market flows. So we’re back to where we started, with a bit of whip-lash to boot.

- Our view is that if this fragile step towards a peace treaty holds, oil flows, and the Kiwi economy can begin healing over the second half of the year. It’s an optimistic view. But even with oil flowing through the Strait again, it will take months to make up for 6 weeks of delays. And supply chains will be re-examined. There will be lasting impacts.

- We’re not out of the woods yet, and the next two weeks of ceasefire won’t bring swift relief. A much longer peace deal will need to hold for the Kiwi economy to stop feeling the pinch of fuel price increases and the threat of a diesel shortage.

Up to this point in the conflict, any news of de-escalation has been speculation only. To have a confirmed shift in the direction of a resolution was a huge (temporary) weight off.

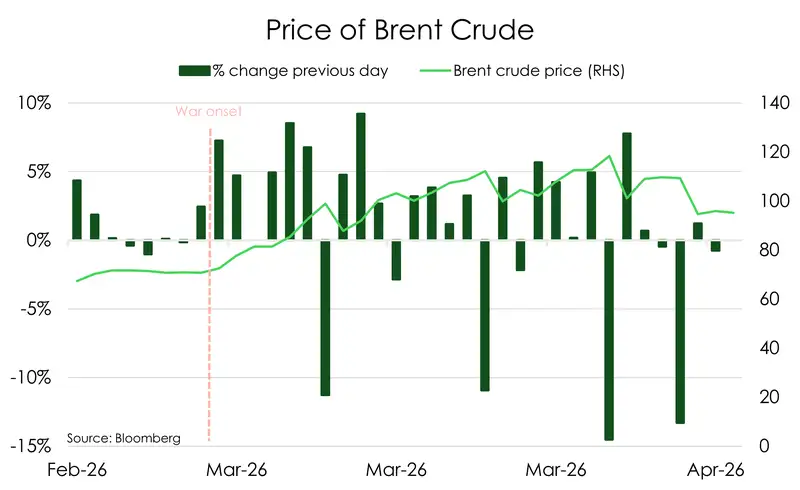

Markets moved swiftly in response to the good news, with a sharp decline in the price of Brent Crude. We saw the price drop over US$7 per barrel in less than two hours. The NZD has also seen a boost, climbing 1c to $0.5806. And the Kiwi flyer was bolstered by what the market read as a Hawkish hold by the RBNZ (we disagree with this read, see here).

We’re still waiting, hoping for this agreement to hold for the two-weeks and hopefully beyond. But news over the weekend reminds us not to count our chickens before they hatch. In the short term, not much will change for the Kiwi economy. If the cease-fire holds and negotiations re-commence, sentiment will improve as fear and uncertainty slowly dissipates. If not, we are likley to see uncertainty and elevated commodity prices squeeze the Kiwi economy into a contraction.

Even with oil flowing through the Strait again, we’ve lost five weeks (and counting) of oil supply from the Middle East. And oil tankers travel slowly, 10-15 knots, about the speed of a push-bike. Oil refineries are just now receiving the last shipments that left the region over five weeks ago. Now refineries will have to wait for the next shipments that have been severely delayed.

All that to say that we’re not out of the woods yet, and the next two weeks won’t bring swift relief. A much longer peace will need to hold for the Kiwi economy to stop feeling the pinch of fuel price increases and the threat of a diesel shortage.

Financial Markets

The comments below were provided by Kiwibank traders. Trader comments may not reflect the view of the research team.

Rates – RBNZ unchanged, notes balance between inflation risks and of unnecessarily stifling the economic recovery

The past week saw both international and domestic factors drive trade with developments related to the conflict in the Middle East coupled with the RBNZ OCR review providing direction.

Tuesday, ahead of the review, our curve traded mildly lower and steeper, with this only partially reversing the sharp move higher witnessed on the prior Thursday, as particularly New Zealand and Australian markets sought to take risk off the table and reduce event-risk ahead of the long weekend. The proximity to the RBNZ statement tempering the rally with some noted underperformance versus Australia noted. Wednesday opened with news that a two-week ceasefire had been agreed to in order to further talks aimed at ending the conflict. This saw an immediate rates market reaction with the curve trading circa 9-points lower in an initial broadly parallel move. The implied OCR path sought to reprice lower, with the year-end implied at 2.75% - down from the near 3.00% at the end of the prior week.

The RBNZ statement landed at 2pm and while delivering an as-expected unchanged result, provided the impetus for a sell-off at the front of the curve. The statement itself appeared to be a reasonably balanced, noting the downstream impacts of the conflict had materially altered the outlook and balance of risks for inflation and growth, noting the near-term lift in inflation and weakening of growth. They noted how if medium-term inflation expectations increase then inflation would likely become more persistent though noted how current weak demand and spare capacity in the economy should constrain this to a degree. The RBNZ also acknowledged that market interest rates had increased, and how the current economic situation differed to that of 2022 where the supply-chain disruption and energy price rises occurred at the time of strong demand. They finished by reminding of the remit of returning inflation to the 2% mid-point of the band over the medium term. It was this part combined with some headlines from the new media conference around whether a rate hike was considered, even though dismissed as “not close to a hike today in any way", that perhaps saw this reported in some quarters as a ‘hawkish hold’. The intent perhaps behind the reminder around the 2% mid-point being to maintain a degree of steepness in the implied track in order to serve to constrain any thoughts around the risks that inflation may become embedded.

The curve response on the day saw an immediate pressure on the front with some taking the opportunity to scale back some short-term positioning. 2-year IRS ended sharply off the low yield on the session, closing at 3.38% on the day (-3) up from the low of around 3.32%, with the 10-year finishing at 4.25% (-9) around a point off the low. The implied OCR path also reversed, with interest so to speak, the earlier move on the session, with the year-end implied moving back to price near 2½ 25-point tightenings by year-end. For the remainder of the week the market continued to trade on the side of the more hawkish interpretation, movements at the front of the curve also drawing out some activity in the forward-start space – particularly given the move from above 4% to circa 3.70%’s then back to 4% all in a short space of time. By the close on Friday, the general view on the path had seen resulted in some decided underperformance in the front of the curve, and particularly against Australia, with the 7-10 April seeing outright NZ 2-year IRS +8-points, AU -4-points, with the short NZ curve weighed down by an implied path moving back to price three 25-point increases by year-end.

Again, where does this leave us and the disconnect we have talked about previously? It would appear to still be in play for those prepared to back a tentative or cautious RBNZ who may be prepared, within reason, to let the market provide some steepness to provide some caution to pricing expectation. From an accrual perspective, the bill/cash gap to short swaps may still prove compelling, particularly given the comments in the review on how the current economic situation differed from 2022 where the demand element was growing more strongly when the gap between these was equally wide. Graham Hughes, Trader – Financial Markets.

In currencies, global headlines remain the driver

Last week the Kiwi dollar lifted on the back of some good/OK news stories. The Iran ceasefire news on Wednesday had the Kiwi lift a full cent higher to 0.5819. Following shortly after the RBNZ delivered a very balanced MPR, but the market took it as leaning slightly hawkish, which provided a touch more support for the Kiwi up to 0.5873. The NZDAUD cross also gathered some strength within this context, trading from a low of 0.8203 up to 0.8297. The ceasefire was fragile from the outset, and the Kiwi dollar lost steam into the close of the week, closing the NY session at 0.5837. Over the weekend there was only bad news out of the Middle East/US, which sees the Kiwi in early Monday trading around the 0.5800 handle. Further upside in the week ahead is likely capped at 0.5850/0.5900, and we expect that the Kiwi is more likely to retreat to the 0.5750 levels, given that risk sentiment has taken another hit. Oil prices are on the surge again, currently up circa ~8%. The NZDAUD cross we expect to remain in the recent relatively tight ranges of 0.8200/0.8300. Domestic data prints are unlikely to provide further bearing on currency direction in the current climate. It’s all headlines again this week. Mieneke Perniskie– Senior Dealer, Financial Markets.

Weekly Calendar

- Domestically the February net migration numbers are out Tuesday, before the Middle East oil crisis had time to impact the economy, so expecting to see strong numbers there. The BusinessNZ Performance Of Services Index for March is out on Monday, and some of the impact will be felt in that data. But more importantly, we will see food prices, retail and total electronic card spending data for March out on Friday. This data will tell the story of how much of an impact did fuel price surges have on the Kiwi economy in Q1. Fuel prices jumped in the last two weeks of March, but we don't expect to see the flow-on effects of that price surge too sharply so early. April and Q2 data will tell us more.

- Offshore, we’re all waiting to see if the fragile cease-fire can hold another week. News was not good over the weekend, with peace talks failing and the US forming a blockade of the Strait of Hormuz, threatening Iran with its Navy.

- Australia is releasing business and consumer confidence data for April/March as well employment data this week. US also has employment data out at the end of the week, along with trade balances. In Asia we have China March trade balances and March GDP.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.