- Back and forth, back and forth, the war in the Middle East is like a tennis match that just won’t end (a hybrid cricket/tennis match?) But despite fresh fire exchanged over the weekend, markets are pricing in a peace deal as highly likely. With the price of oil down to pre-war levels, we might just see demand pick back up. But a lot has to happen for peace to stick.

- The good news is that humans are resilient and many countries are adapting to the oil disruption. The UAE is fast-tracking its East-West pipeline build. The US, Brazil and Venezuela are pumping out record-levels of oil. And the business case for electrifying operations has strengthened significantly.

- Our view is that the Kiwi economy has taken a knock but is not out for the count. The oil shock has put the brakes on our recovery, enough to destroy demand, but not derail us completely. There’s a strong case for not hiking in July. Keeping interest rates at accommodative levels for the time being is the RBNZ’s best bet at helping the economy recover.

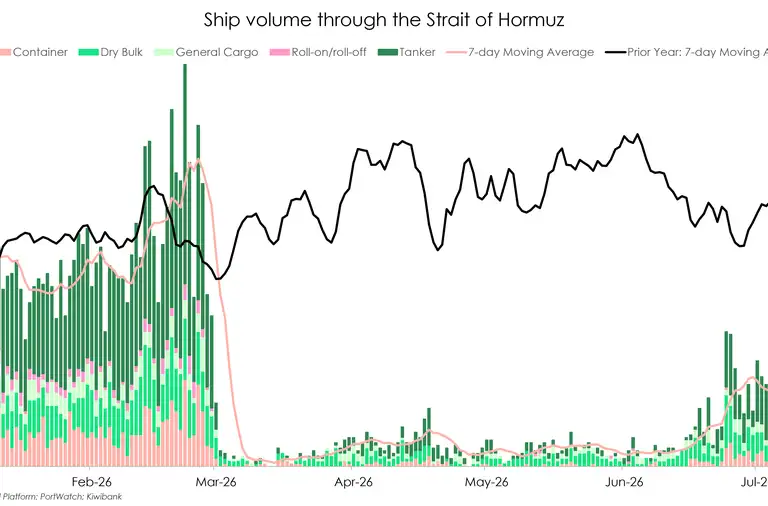

The war in the Middle East is on “hold”, but Iran and the US served fresh volleys over the weekend. The Strait of Hormuz is still closed after being open for less a than a week when the deal was initially struck. Despite this, markets are pricing in a very high likelihood of a peace agreement. The price of Brent crude has continued to drop over the last week, currently sitting at $72 USD per barrel. That price doesn’t reflect the reality of oil supply and demand. We have a low volatility index, meaning markets are not making a racket (as has been the story all year).

The good news is that quite a few tankers managed to get out of the Strait of Hormuz during the small window of peace, meaning more oil supply going to refineries in Asia. That will later come to us. Additionally, countries like the UAE are adapting, for example, fast-tracking the East-West pipeline, to bypass the Strait of Hormuz. The US, Brazil, and Venezuela have increased oil production and exports to fill global supply gaps resulting from the conflict. In short, the world is adapting around this curve ball of a crisis.

The demand destruction playing out in poorer countries has served to decrease the amount of global oil demand. That will change as the price drops. A decrease in price drives higher demand for fuel that isn’t there.

Domestically, it makes financial sense for businesses to insulate themselves from future oil shocks by taking advantage of new technologies. These adaptations will take time, but the war in Iran is a catalyst for change that will pay off in the long run.

The Kiwi economy had a strong start to the year, but the soaring price of petrol, diesel and other petrochemicals stifled demand. Business and consumer confidence have been slammed, intentions to invest and hire have taken a nose-dive during this crisis. As the price of fuel feeds into the cost of doing business in almost every industry, businesses facing a cash-strapped final consumer have been hard pressed to raise prices. Some industries have been less affected than others, since we have to buy some necessities to survive, regardless of the price. But industries like construction, where projects can be delayed indefinitely, have taken a massive hit.

It will take time to recover from the demand destruction of the oil crisis. But there are some signs of resilience. Some first-home buyers are taking advantage of a bottoming out of real estate prices, manufacturing is still showing signs of strength, and a weak Kiwi dollar supports our exporters by essentially giving our main trading partners a discount on NZ goods. Monthly filled jobs data for the month of May is out this morning. We expect job growth to be subdued due to the oil crisis and a lag between economic recovery and job market growth.

This all culminates to one thing. The RBNZ is less likely to hike rates in July. In our view, that’s the right move. Wait and see how the demand destruction plays out and how delayed our recovery is.

Financial Markets

The comments below were provided by Kiwibank traders. Trader comments may not reflect the view of the research team.

Markets are back focusing on what matters.

The main theme through last week was a fading in Middle East risk premium, alongside markets reassessing the outlook for US interest rates.

Oil prices have now given back most of their earlier gains, with Brent crude falling back below pre-conflict levels. Shipping flows through the Strait of Hormuz are beginning to normalise, and markets are growing more comfortable that a US–Iran deal remains on track. However, developments over the weekend are a reminder that tensions haven’t fully disappeared, and the situation remains fluid. While markets have so far taken these incidents in their stride, they do highlight that geopolitical risk hasn’t been fully priced out. For now, lower oil prices are helping ease inflation concerns at the margin, but the backdrop remains sensitive to any renewed escalation, with peace talks set to resume this week.

Away from geopolitics, focus has shifted back to the strength of the US economy. Recent data continues to support the view that US interest rates may need to stay higher for longer. This has underpinned the US Dollar, pushed short-term US yields higher, and weighed on assets such as gold and commodity-linked currencies. For the New Zealand Dollar, it was a weaker week. The combination of higher US yields and softer commodity prices saw NZD/USD come under pressure, drifting to multi-month lows. On the downside, initial support is seen at 0.5636, the 76.4% retracement of the 0.5486–0.6120 move, followed by 0.5590 (the October 2025 low), with the multi-year low at 0.5486 below that. Across the Tasman, Australian employment data was mixed. While there was a rebound in May, this was offset by downward revisions to prior months. It doesn’t materially change the view that the Reserve Bank of Australia is nearing the end of its tightening cycle, although the AUD did find modest support on the release, with NZD/AUD briefly dipping below 0.8170.

In the near term, NZD/USD may remain under pressure while USD demand persists, and US rate expectations stay elevated. For now, markets are back focused on the matters that matter most – the management of longer-term inflation dynamics and not playing dodgeball with Trump lobbed geo-political grenades. Interest rate expectations are back in vogue and with a Fed determined to deal with inflation right here and now, the USD stands out from a pure yield play perspective. However, as the cycle evolves, lower oil prices feed into lower inflation markets will begin to look toward eventual US rate cuts – perhaps now not until 2027 - the New Zealand Dollar should find better support particularly as the RBNZ normalises rates for the right and not wrong reasons. For NZD buyers, current levels and perhaps into the 55s once again present attractive hedging opportunities as have been noted in previous ventures since establishing strong Covid determined support lows. Hamish Wilkinson – Senior Dealer, Financial Markets.

The Week's Key Events:

- NZ monthly filled jobs data for the month of May is out today (Monday). Business and consumer confidence surveys for the month of June are also due this week, on Tuesday and Friday, respectively. Other high-frequency data to watch includes the HLFS estimate resident population for June (Wednesday) and Building consents for May (Thursday).

- The war in the Middle East is still churning away. Crucially, the Strait of Hormuz is closed. Again. Globally, uncertainty is high, but volatility is low. Markets are optimistically pricing an end to the conflict (or an adaptation away from the Strait of Hormuz). Oil prices are bottoming out and we are keeping a close eye on how long they remain low.

- Across the Tasman, we are expecting the RBA Minutes of the June MPB Meeting on Tuesday. Also on Tuesday, private sector credit data for the month of May, with building approvals data out on Wednesday. Finally, Aussie international trade is due Thursday.

- In the US, we have non-farm payrolls data out on Thursday. This crucial employment data will speak to the state of the US labour market. Also on the radar, Eurozone CPI is due on Wednesday.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.