- It feels like we’re stuck in the dentist waiting room. Limbo. The war in the Middle East keeps going on, and on… and on… And we’re forced to wait. The White House is discussing Iran’s latest proposal to re-open the Strait of Hormuz in exchange for the US lifting its blockade… so we continue to wait and read the outdated magazines.

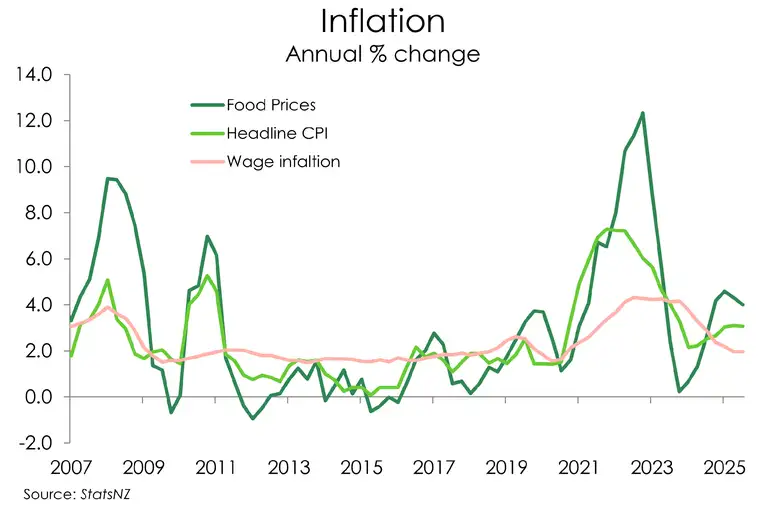

- The domestic inflation report card from last week wasn’t what we were wanting, despite coming in as expected. The 3.1% inflation rate was unchanged, and uncomfortable for the RBNZ. We don’t think it’s time to react. And we don’t expect the RBNZ to hike in response, but others disagree.

- Our view is that demand destruction is ongoing, and will keep inflation bound over the medium term. Kiwis are already struggling, with the most vulnerable families and businesses feeling it most. Rate hikes are not the answer, in our view, and will not help solve the fuel cost crisis. This is not a demand shock that requires reining in.

The situation in the Middle East hasn’t been resolved, and we are stuck in a liminal space. We’re mindful of inflated fuel prices without an end to the conflict… The price of Brent crude has gone back up to $108 USD a barrel this morning – we had a short reprieve mid-month, with prices going as low as $90 USD. Domestically, we have had some easing in petrol prices (still over $3L for 91), but those prices could go back up… while the price of oil remains elevated. An end is in sight. But is it just a moving mirage?

Last week’s inflation report card was not good news. Prices rose over the first quarter, at a rate above market expectations. Despite coming in inline with our forecast, it wasn’t what we wanted to see. A 3.1% inflation rate is slightly above the RBNZ’s target of 1-to-3%, Aiming for 2%.

But there’s no strong demand-side growth story to tell. Tradable (imported) inflation accelerated, as expected, to 3.1% from 2.6%. Petrol spiked 3.5%, diesel 11.3%, over the quarter. And we will see another sharp push higher in the current June quarter.

The non-tradable (domestic) inflation remained elevated at 3.5%. That’s not good. A lot of the pressure came through from central and local government charges. And although local government costs were up 8.1% compared to last year, they were only up 0.1% from last quarter. Central government costs were another story, 4.8% up from last quarter and 7.5% from last year. Taking government costs out, the inflation rate drops to 2.7% over the year.

Other items ruined romance. Coffee and chocolate prices moved up, making that romantic gesture of a coffee in bed or the gift of chocolate even more valuable. Jewellery and watches became more expensive on the back of silver and gold prices going up – an expensive quarter to be buying an engagement ring!

By and large, food prices were up 4.0%, mostly driven by fresh produce up 7.4% yoy, and meat up 7.7% yoy. These cost increases when paired with the fuel costs rising are devastating for our most vulnerable Kiwis.

On the back of that, we have the wholesale rates market pricing in three rate hikes by October now… over 90bp by December, and 130bps by this time next year. That is super aggressive, even for the most hawkish of hawks. We’re acutely aware that with other bank economists calling for rate hikes. It’s frustrating and dispassionate. We might see this play out like a sell-fulfilling prophecy, with that sort of commentary feeding into inflation expectations - which is a key component that the RBNZ is keeping an eye on.

Anna Breman will speak at an event in Hamilton on Wednesday, which may offer further guidance on the policy outlook ahead of the May meeting. Hopefully she brings her ice bucket again to douse the heated panic out of the rate market.

Financial Markets

The comments below were provided by Kiwibank traders. Trader comments may not reflect the view of the research team.

Rates – Growth risks, inflation risks, policy path - uncertainty remains despite data

The past week saw domestic factors play more of a roll in rates market activity. Monday saw NZ markets largely play a degree of catchup to an offshore market rally on back of conflict deescalation themes, that had seen a broad-based firming in US rates, including futures moving to reintroduce pricing of a Fed easing this year, with the domestic curve 6 to 9 points lower across 2 to 10-year. Tuesday attention turned to domestic data with the Consumers Price Index (CPI) the key focus, though this preceded by the Quarterly Survey of Business Opinion (QSBO) that given the current geopolitical and domestic economic climate had the potential to carry more influence than usual. The QSBO painted a downbeat picture of the economy noting amongst other things that the number of firms expecting an improvement in general economic conditions falling to a net +1% from +39% in the prior survey, though there was little discernible market reaction ahead of the main event. While a firmer March quarter CPI was expected and given the selected price index data released the week prior had indicated the extent of fuel price impacts, the still above-expectation print was enough to push rates higher on the day.

Headline March quarter CPI recorded a 0.9% gain on the quarter for +3.1% on the year against expectations of +0.8% and 2.9%, while the quarterly tradable and non-tradable figures were seen at +0.7% and +1.1% against 0.6% and 0.9% expected. As noted, the rates curve shunted higher on the release, with the front of the curve driving, with 2-year IRS higher by around 11-points at one stage before the release of the RBNZ sectoral factor model mid-afternoon provided for a let up in the selling. The RBNZ measure of core-type inflation recorded +2.7% over the March year, declining from the prior +2.8%. By the end of the day, 2-year IRS was marked higher by 7-points to close at 2.36%, 5-year 3.86% (+4), and 10-year 4.23% (+1), while the implied OCR path had moved to aggressively price near-term moves, with May meeting probability jumping from around 20% to near 50% of +25-points, and July through 100% priced. The remainder of the week saw our rates market continue to grind higher with the Moody’s ‘outlook negative’ change further detracting, with the implied curve now closing in on five 25-point moves within 12-months, with the IRS curve persisting with a bear-flattening – 2-year IRS at 3.53% +11 on the week, 5-year 3.96% (+6), and 10-year 4.33% (+2).

While the headline CPI printed higher, the RBNZ model measure showed some small progress and combining that with the decidedly downbeat QSBO and other business and consumer surveys with potentially some ratings agency inspired reduced fiscal flexibility leaves the implied rate path perhaps a little less certain than pricing may imply. While many would agree that the likely path is higher, and some may even suggest that the economy needs to ‘de-normalise’ 2%, the timing of any such move higher is up for debate. The RBNZ at its last review did note that the current economic situation is different to that of 2022 when COVID-19 and Russia’s invasion of Ukraine disrupted global supply chains and increased energy prices, adding that then demand was growing strongly which added to inflation pressure. This time however, certainly most reads on the general economic environment place the economy on a somewhat weaker footing, with this having deteriorated further with recent events, leaving questions as to the robustness of demand, and consequently the ability of businesses to translate pricing intention into pricing reality.

As noted previously, the RBNZ appears to be willing to utilise the medium-term language in their remit potentially utilising this flexibility to determine if pricing intention embeds and is reflected through higher prices or if the current price impact is only transitory and should be looked-through. So, all up, with the curve essentially currently pricing moves at five of the next seven meetings, could the risks to current pricing be viewed as asymmetric leaving the curve vulnerable to a steepening lead by the front? With a number of central banks due to provide assessments on these matters this week, it may well provide further insights into the balancing of monetary policy in the current environment and subsequently may prove to be an interesting one. Graham Hughes, Trader – Financial Markets.

In FX – Little change on the technical front

In currencies, the Kiwi continues to orbit the 0.59 handle, with price action stuck in tight and relatively uninspiring ranges. There is little change on the technical front, with support still evident around 0.5850 and resistance capped near 0.5930. Volatility has eased further, with 1 month NZD vols now back below 9 — broadly in line with pre conflict levels — and appearing biased lower as headline risk subsides for now. Offshore drivers will dominate the week ahead. The FOMC decision is widely expected to be uneventful, with no change to policy and a focus on commentary around inflation risks. While incoming Fed Chair Kevin Warsh has been vocal in distancing himself from political influence, markets remain mindful of his historically dovish leanings — creating a potentially conflicted policy outlook in the months ahead. That said, uncertainty around Fed direction has become a familiar backdrop.

In the cross currencies, attention turns to Australia, with Q1 CPI due tomorrow alongside inflation updates from Europe and Japan. NZD/AUD is trading within a clear descending triangle formation, with support near 0.8190 and descending resistance currently around 0.8270. From a technical standpoint, this setup carries a bearish bias, placing added significance on the Australian inflation print. Further offshore, US PCE inflation will also be closely watched, while outside of the Fed, policy updates from both the Bank of Canada, Bank of England and the ECB are due. No changes to cash rates are expected from any, but guidance around inflation and growth risks remains key for broader FX sentiment. Hamish Wilkinson – Senior Dealer, Financial Markets.

Weekly Calendar

- It's a massive week of central bank rounds. BoJ, the Fed, BoE, ECB and BoC, all expected to hold their rates steady. Other data out this week US PCE inflation and US ISM Manufacturing Index; China April PMIs and Australia, March‑quarter CPI. Australian inflation pressure is expected to push higher, with pressure on the RBA to consider a further rate hike.

- Domestically we have RBNZ Govenror Breman set to give a speech this Wednesday in Hamilton. We hope to hear another cool, calm and collected message which may help douse the market expectations.

- Other domestic data to look forward to next week, Q1 Labour market data out on the 6th of May.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.