- Our first inflation read for 2026 is out and although it’s as predicted, 3.1%, it’s not what we were hoping for. Inflation is just above the RBNZ’s target band, with no big downside surprises to help ease cost pressures.

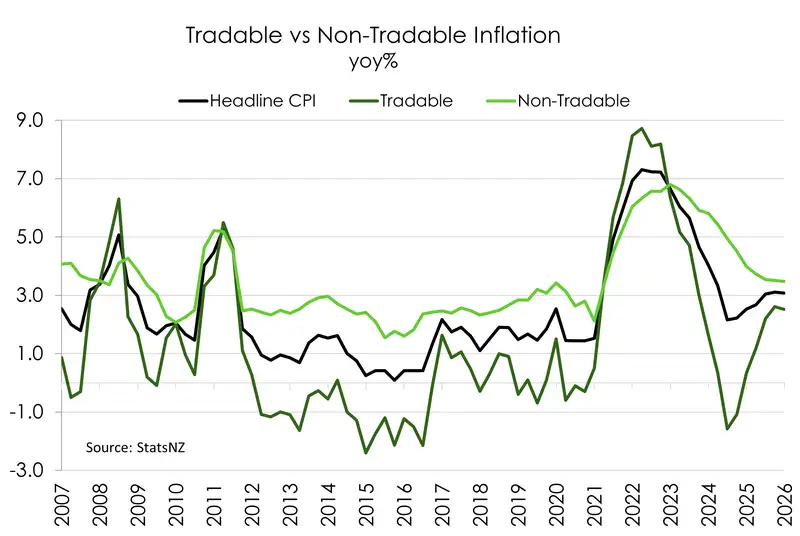

- Tradeable inflation (imported) accelerated to 3.1%yoy, with the rise in petrol. The tradeable rate drops to 2.7% when we exclude all fuel costs. Some domestic inflation pressure kept the headline up as well, including government charges and food. But the trimmed mean inflation eased from 2.8% to 2.6%. That core measure was the good news… we had hoped for some more good news, but were left wanting.

- All in all, there’s nothing in theses numbers to spook the RBNZ in to early action. But the Kiwi economy is in an awkward position. The Quarterly Survey of Business Opinion, also out today, adds a down-beat tone to the story. The global uncertainty is causing firms to pull back, and batten down the hatches.

We expected an awkward report, and we got an awkward report. We had hoped to see some more disinflation, but we didn’t see enough of it. Just because we forecast a 0.9% gain, and a 3.1% annual rate, doesn’t mean we like it. We weren’t expecting good news, and we didn’t get good news. The early stages of the war in Iran, played a part.

Tradable inflation accelerated, as expected, to 3.1% from 2.6%. Petrol spiked 3.5%, diesel 11.3%, over the quarter. And we will see another sharp push higher in the current June quarter. That we know. That we don’t like.

From the RBNZ’s perspective, it’s the non-tradables components that matter more. It’s the domestically generated inflation that they have some control (influence) over. And non-tradables posted enough of a gain to keep the annual rate unchanged at 3.5%. So no real relief there. And that’s no fun.

We had hoped to see some more disinflation in the core measures, to give the RBNZ a clearer reason to hold back on rate hikes. Today’s report does not support immediate rate hikes as priced in the market… but it does highlight the awkward starting point for inflation leading into the conflict in the middle east.

Some of the domestic pressure came through from central and local government charges, and we can’t just blame council rates this time. Although local government costs were up 8.1% compared to Q1 of last year, they were only up 0.1% from last quarter. Central government costs were another story, 4.8% up from last quarter and 7.5% from last year. Taking these government costs out, the inflation rate drops to 2.7% yoy, the same read as last quarter.

Other main drivers of inflationary pressure came from food prices, up 4.0%, mostly driven by fresh produce (up 7.4% yoy and meat (up 7.7% yoy). Coffee and chocolate prices also driving some of the move up. Some surprises came from prescription charges affecting health costs, fees free University tuition changes, and the cost of jewellery & watches going up with the price of gold and silver. Not a good quarter for romance if you were looking to buy an engagement ring or surprise your significant other with their favourite chocolate.

All in all, there’s not enough in theses numbers to spook the RBNZ in to early action. The deflationary pressure we were expecting hasn’t shown up yet, but we are already keeping eyes on next quarter’s numbers and the one after that. The true impact of the oil disruption (prices up and down) won’t show up for a while yet.

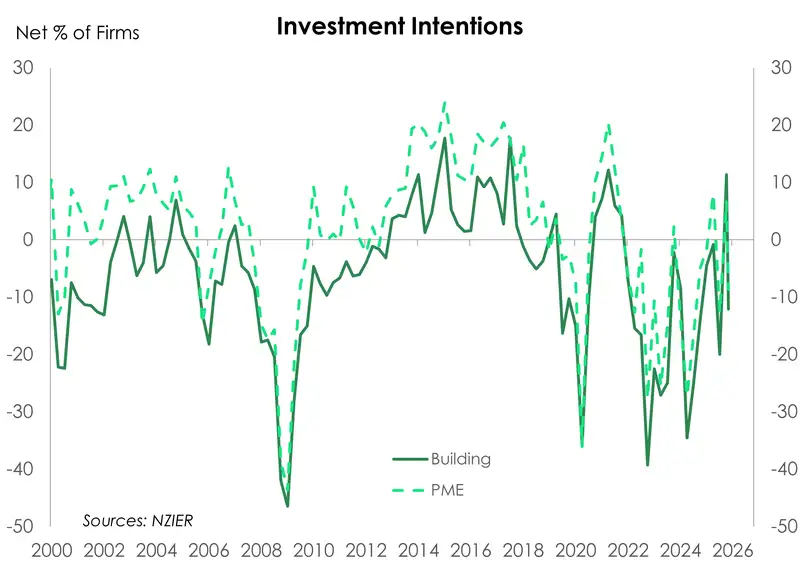

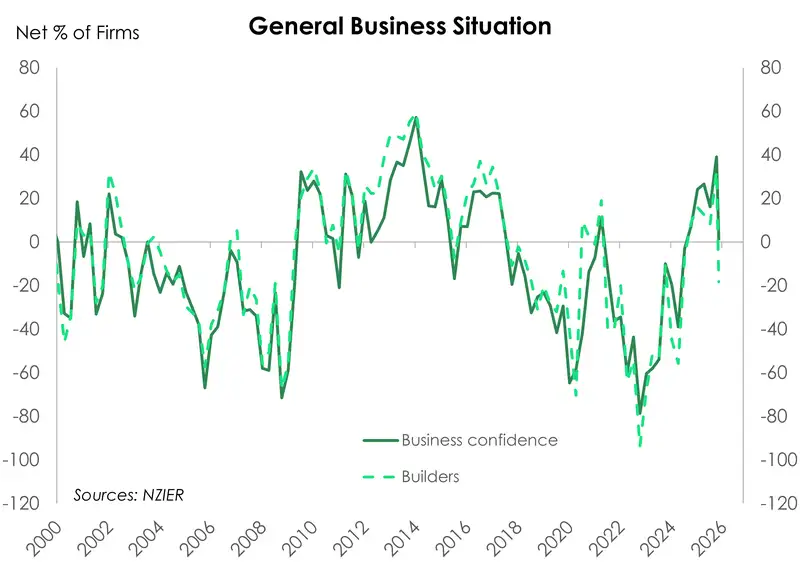

At the same time, the NZIER published their Quarterly Survey of Business Opinion (QSBO) today. And there was a marked deterioration in firm’s confidence and activity… as you would expect. The report captured the early reaction (6 March to 10 April) to the Iran war. Just a net 1% of firms expect an improvement in economic conditions… down from a net 39%. And we’re likely to see a further fall from here. “Overall, these results suggest that the fragile recovery that had been taking shape is at risk given the gas and oil supply chain impacts of the US-Israeli war with Iran. The increased caution amongst firms is evident in the cutting back of staff numbers by firms in the March quarter, as well as the decline in investment intentions.” - NZIER. It is the postponement, or cancellation, of investment decisions that raise the red flag for us. When considered alongside the “cutting back of staff numbers”, firms are battening down the hatches… and that kills growth.

On the inflation front, the NZIER noted that “inflation remains contained in the New Zealand economy for now, despite the recent surge in fuel prices, which has raised costs for households and businesses. It appears weak demand is limiting the extent to which firms can pass on rising costs.” It’s hard to pass on costs when demand is elastic, and businesses and households simply buy less at the higher price.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.