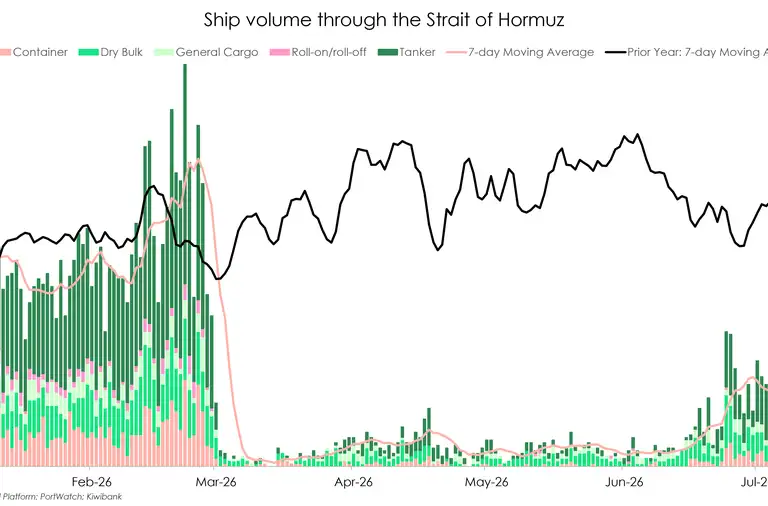

- The conflict in the Middle East continues to vacillate between escalation and peace. The two-week ceacefire is due to end this week. So far, the Strait of Hormuz has been opened and closed and open and closed again so many times we don’t know what to expect next. The price for Brent Crude dropped last week and is now picking back up. Time will tell when things normalise again.

- This week we have two big domestic numbers out, the Quarterly Survey of Business Opinion and CPI for Q1, both out on Tuesday. We expect the CPI show a small bump relative to our forecasts from last year – staying closer to the 3.1% we ended 2025 on.

- Our view is that Kiwi businesses and households have just had to wear these hugely increased costs of transport right in the middle of a cost of living crisis – household savings are depleted, business margins are depleted, appetite for risk is down, confidence is down – we aren’t expecting a swift rebound, but more likely an achingly slow recovery once the war is over.

The war in the Middle East is still causing conflicting headlines. The market is responding to the volatility by reacting more strongly to the good news than the bad – we don’t mind that optimism. The US-Iran cease-fire held for another week, and the end of last week saw a 10-day cease-fire agreement reached between Israel and Iran as well. On the flip side, the US is putting substantial pressure on Iran in the strait of Hormuz, mobilising its Navy and adding extra troops to the region to create a blockade. One moment the Strait is open, then it is closed again.

In the mean time, we’re hearing more and more stories of Kiwi businesses struggling under the strain of increased fuel prices, especially diesel. The increased operating costs passing through supply chains from B2B businesses are now reaching the final consumer. The push-back is powerful. Businesses at the end of the supply chain are faced with consumers more and more willing to cancel or delay projects, because wearing the cost of the entire supply chain is proving impossible.

A big shift is coming to industries that rely on diesel. Negotiations about who should wear the cost of this supply shock are starting. We expect that some suppliers, dealing with understanding Kiwi businesses have been working on the honour system to overcome what we’ve hoped is a short-term shock.

This week, we are looking forward to the Q1 Quarterly Survey of Business Opinion and Q1 CPI data both out Tuesday. We finished 2025 with a 3.1% inflation rate, and we started 2026 at the same run rate, just above the RBNZ’s target band. Without a strong demand-side growth story to tell, the increased prices we are likely to see, should be temporary.

The March 2026 quarter only got to see the very beginning of the oil crisis, so we don’t expect next week’s numbers to show much price pressure. The June quarter is when the true impact will be felt.

The war in Iran broke out on the 28th of February, but the real impact didn’t hit our shores until mid-March, when we started to see petrol prices increase. That means only 1/6 of Q1 was affected (2 weeks out of 12).

We’re playing it by ear and making some adjustments to our Q1 CPI forecasts. We’re expecting a chunky 0.9% over the first quarter, keeping the annual rate at 3.1%. That is significantly above our original forecast of 2.4% for the March quarter.

Financial Markets

The comments below were provided by Kiwibank traders. Trader comments may not reflect the view of the research team.

Rates – RBNZ policy dilemma

The past week saw our rates market back to headline watching for direction, though some local commentary did provide some input at stages.

Monday opening saw rates opening higher after the breakdown of talks between the US and Iran where they failed to produce a way forward with the sticking points reportedly on the nuclear and tolling aspects, though a later press reports citing some involved indicated a slightly less hawkish read on the situation. The curve opened higher and combined with commentary from a domestic bank indicating three 25-point tightenings from the RBNZ in rapid succession was their central case, saw the curve higher and flatter – up 7.5-points in the 2-year, and 6.5-points in the 10-year, with the move outpacing a similar upward adjustment seen in Australian markets. The front of the curve saw the implied path pricing three-plus 25-point moves by year end. It was noted that The Treasury also released its regular economic update where it referenced the disruption from the current conflict and the negative impacts from this. They reported on their meetings with businesses and industry in early March alongside the RBNZ, whereby the general theme was that growth remained fragile, while developments in the Middle East were considered an emerging downside risk. It was also noted that margins in the domestic sector were compressed owing to modest demand that limits firms’ ability to raise prices. As has almost become the norm recently, the curve looked to re-trace the move the following day. Our curve opened lower, and again with a flattening bias with the front of the curve still weighed by the implied pricing, and some wholesale flattening interest circulating. Our implied continued with the three-plus tightenings by year end for around 115-points over the next 12 months while in comparison the Australian implied curve did start to look to finesse the tightening cycle, with their curve pricing a peak in early Q4 before mild reductions thereafter. The curve continued with incremental rallies as the week progressed, with a degree of receiving activity around front of the curve emerging towards the end of the week, including some near-term forward start, this despite some additional economists finding safety in numbers in calling for more rapid rate rises. The resultant activity did start to see curve pivot with a mild steepening occurring.

This week, while CPI data is due for Q1, and the obvious jumps in the fuel categories were noted in Fridays selected price index release, high-frequency data aside, until the receipt of further data in the form of Q2 and Q3 CPI it may be a little difficult to determine if the current lift in pricing shifts from a likely transitory event to be looked-through or to one which permanently embeds in pricing. The RBNZ has so far displayed a degree of caution and willingness to lean on the medium-term language contained within the remit, most notably in the February MPS when perhaps the economy appeared to be on a sounder growth footing, so it may be viewed as a potentially a difficult proposition to change this approach now, and particularly so given the recent deteriorating growth sentiment noted by businesses. So, for the curve, does that see the acceptance of a priced steepness element to the front in-part to curtail expectations while the OCR provides the anchor, or does the RBNZ deliver a pre-emptive near-term move in what some may suggest would likely see a lower peak cash rate. Either way, the accrual play at the front of the curve is, within reason, likely more determinable than that of weekend headline watching. Graham Hughes, Trader – Financial Markets.

In FX – a recent outperformance within risk-on environments, may provide longer term clues when better times come.

The Kiwi enjoyed a solid week as global risk appetite returned. From trough to peak, NZD/USD rallied around 2.4%, touching a 0.5929 high late Friday as markets initially reacted to headlines suggesting progress in US–Iran negotiations, including speculation around the Strait of Hormuz and a potential halt to Iranian nuclear enrichment. However, clarity following the New York close that the US intends to maintain its blockade, alongside heightened uncertainty over the negotiation path, saw sentiment reverse. As markets opened on Monday, the Kiwi was marked around 0.5860 — roughly 1.2% below last week’s highs.

Volatility within well defined recent ranges remains the dominant theme for investors. Technically, NZD/USD has cleared both the February–April descending channel resistance and the 200 day moving average near 0.5850. The next upside battleground sits at the 61.8% Fibonacci retracement around 0.5935, while initial support at 0.5850 looks likely to be tested in the near term as markets await fresh headlines ahead of the expiry of the two week US–Iran ceasefire arrangement.

Looking ahead, attention shifts firmly to macro drivers this week. Domestically, NZ CPI will provide important guidance on the inflation outlook and the timing of any eventual shift in RBNZ policy signalling. Offshore, a heavy slate of global CPI releases and US retail sales will shape expectations around inflation persistence, consumer resilience, and the path of US rates. Together, these releases are likely to dictate broader risk appetite and USD direction, leaving the NZD reactive rather than self driven.

More broadly, against a backdrop of geopolitical uncertainty, elevated inflation expectations, and ongoing headwinds to global and domestic growth, the Kiwi’s turnaround over recent weeks has been impressive. It may offer a glimpse of what the longer term outlook for the currency could resemble once the domestic economy is on a firmer footing and the RBNZ is tightening policy for the right — rather than the wrong — reasons. Hamish Wilkinson – Senior Dealer, Financial Markets.

Weekly Calendar

- It's an important week for domestic data. The March quarter CPI numbers are out on Tuesday, with the NZIER Quarterly Business Confidence Survey also out at the same time. Our expectations are set, nothing too drastic this quarter, the June CPI is where the real drama starts.

- Internationally, the two-week cease fire between Iran and the US is due to expire on Tuesday - all eyes will be on the region to see if the conflict escalates or if we get an extended deadline and more peace negotiations.

- Japan is also expecting their CPI numbers this week on Friday. US monthly retail data also out this week.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.