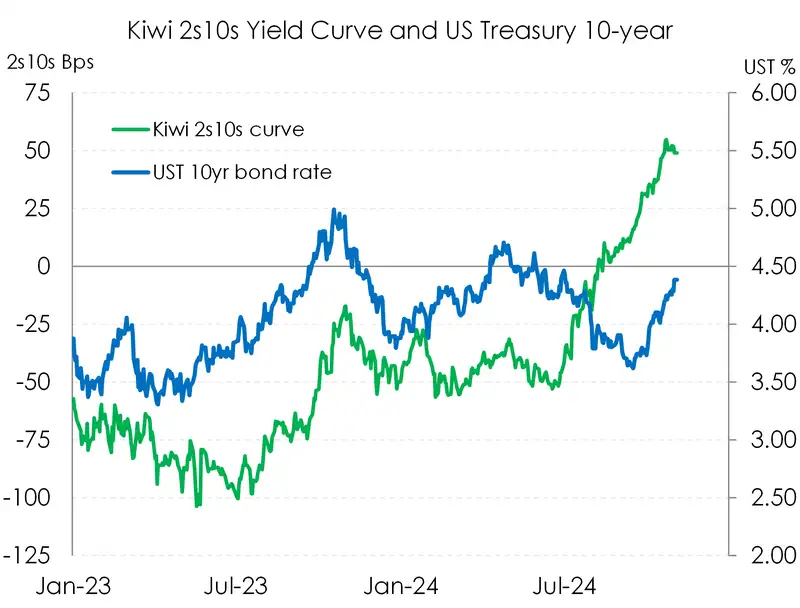

The US election, with thoughts of Trump being re-elected, has caused a push higher in US interest rates. Trump’s policies are seen as stimulatory and inflationary. Even Harris’s policies are likely to cause a bit of inflation. The rise in US yields has pushed interest rates up globally, including in NZ. And it’s the longer end rates, like 5- and 10-year, that have moved the most. The move has not impacted our shorter rates, with the 2-year swap rate firm around 3.68%. The 2s basically haven’t moved much at all.

If you’re on a trading floor, you like looking at curves. As analysts, we love ‘em. If you could imagine a sand pit full of kids with tonka trucks, sandcastle buckets, and spades… the cool kids are the rates traders, the naughty kids are the FX traders, and the economists are sitting on the grass outside the sandpit, not invited to play. We just model what it would be like to play. And the stock market traders are the smallest, covered in sand, but always optimistic. All kids understand the importance of interest rates. Interest rates are like the sand.

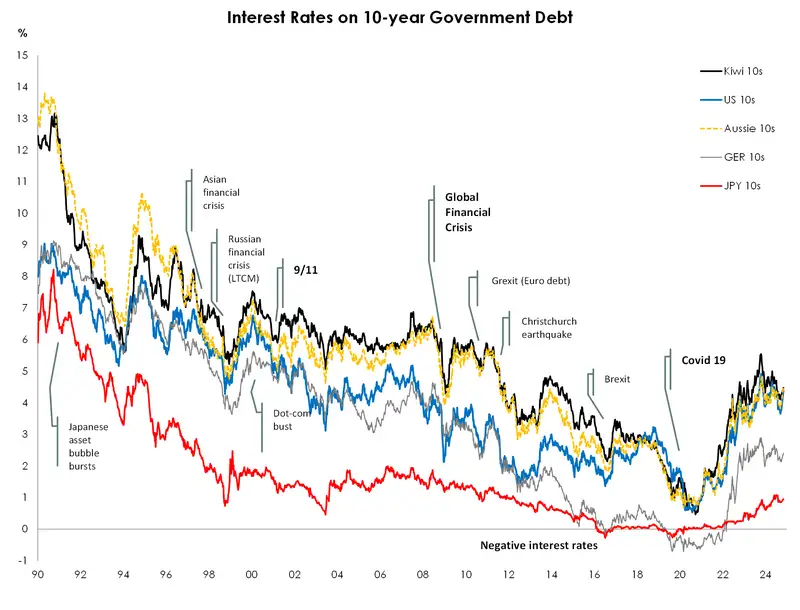

We’ve seen some extraordinary moves in interest rates over the Covid period. Interest rates broke to new lows, in the history of mankind, and even became negative in parts. Those same rates were catapulted higher over 2022 and 2023 as central rates had to unwind and reverse policy stimulus. And now they’re cutting again.

Interest rate curves, typically measured by 2-year rates versus 10-year rates, move in response to economic developments and policy changes. When central banks cut rates, shorter term rates move (down) the most, and the curve steepens. Short term rates fall below long term rates. But sometimes it's the longer end that moves more, like what we’re seeing now.

The move in US rates is not all Trump. The primary driver has been around the US Fed, cutting less, and the US economy outperforming. The US 10-year has lifted from a little over 3.6% to 4.38%. Most of that is fundamental, economics driven lift. We’d say the move from 4% to 4.38% is more election driven. Trumps polices are inflationary… and so too are Harris’s.

So what does it mean? Well, rates markets are pricing in a bit more growth and a bit more inflation over the longer term. Some of that move reflects central bank easing. Cutting interest rates generates more growth and inflation. And some of that move reflects the risk of inflationary policies in the US, including tariffs. With higher 5-to-10 year rates, the mortgage curve may find a higher base next year. We still see mortgage rates hitting 5%, or slightly below, but they may not be there for as long as we currently expect.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.