Modal to play video

- The war in the Middle East isn’t over yet. And we don’t know when it will end. And even when it does, it will take months to return to normal. The real threat that remains, is the risk of a true knockout punch, that would come from a domestic fuel shortage. The heightened uncertainty is causing businesses and households to bunker down. Raising interest rates is tone deaf, and potentially reckless. Both businesses and households are struggling with increased costs, not surging demand.

- Any rise in the costs of essentials will feed into inflation short term, but cost increases will push demand down and put down-ward pressure on growth. We are likely to see a contraction in economic activity in the current quarter. And we won’t see this played out in the data for months to come. Q2 CPI isn’t out until July, after the RBNZ’s decision, and to know if inflation sticks around we really need to see Q3 data at the very least.

- In our view, the RBNZ’s best course of action is to watch, wait, and weigh up the facts once they have the information in front of them. Households and businesses who’ve already seen their costs rise don’t need a rise in interest rates to dampen their demand – because this is not a demand story, this is not Covid. Raising interest rates risks a repeat of past mistakes, potentially inducing a recession. It could be reckless.

Trump’s failed peace talks over the weekend have us worried about inflation and most importantly, how Kiwi businesses are meant to weather yet another punch in the guts from inflated fuel prices. We speculate over the length of the conflict and already, we are looking to 2027 for an economic recovery – it feels like this year is similar to last.

The war in the Middle East isn’t over yet. And we don’t know when it will end. And even when it does, it will take months to return to normal. The real threat that remains, is the risk of a true knockout punch, that would come from a domestic fuel shortage. And it is still a serious threat. The heightened uncertainty is causing businesses and households to bunker down. Confidence has been hit, and so to have investment intentions and hiring. Raising interest rates is tone deaf, and potentially reckless. Because both businesses and households are struggling with increased costs, not surging demand.

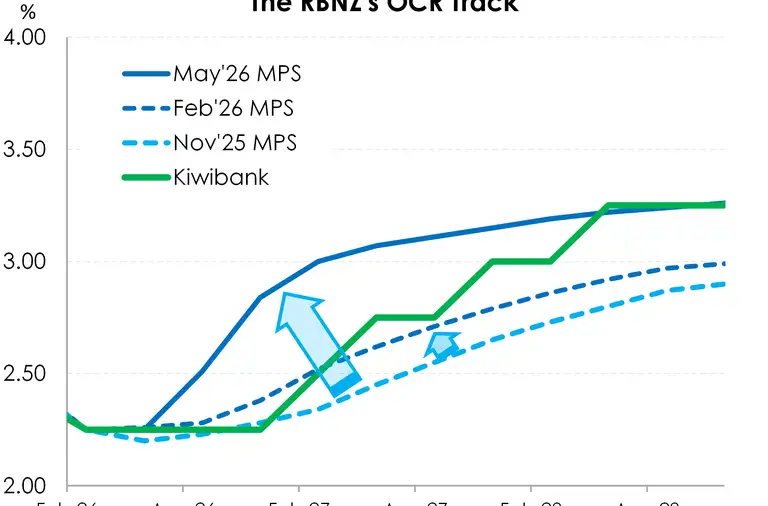

Uncertainty is up, prices are up, and the only logical next step is for demand to bottom out. We see little risk of inflation becoming imbedded in the economy through wages. We have a high unemployment rate (5.4%), a high underutilisation rate (13%), and low growth. With wage growth at 2%, we’re at a low starting point. With GDP growing only 1.3% over 2025, we’re at a low starting point. With inflation at 3.1%, we’re at a slightly uncomfortable starting point. It’s not the 7.3% we saw out of Covid. And we see a swift move back to 2% in 2027 (unfortunately no longer 26).

We are likely to see a contraction in economic activity in the current quarter. And we won’t see this played out in the data for months to come. Q2 CPI isn’t out until July, after the RBNZ’s decision, and to know if inflation sticks around we really need to see Q3 data at the very least.

The RBNZ have been clear on one thing, which is there won’t be any knee-jerk reactions from them. They don’t feel pressured to pick a move too early, and we agree.

In our view, the RBNZ’s best course of action is to watch, wait, and weigh up the facts once they have the information in front of them. Households and businesses who’ve already seen their costs rise don’t need a rise in interest rates to dampen their demand – because this is not a demand story, this is not Covid. Raising interest rates risks a repeat of past mistakes, potentially inducing a recession. It could be reckless.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.