We have already recorded a technical recession, well in advance of any forecasts. And we’re likely to see another 3 quarterly declines from here. No matter how you slice and dice the data, the rapid rise in interest rates is dragging down demand.

Our forecast terminal cash rate of 5.5% is unchanged. And the RBNZ has said as much. The focus (rightly) turns to the timing of rate cuts. And we think cuts will be delivered from February next year.

It’s technical, but it’s a recession. And we’re likely to see a double dip recession this year. Our first dip was over spring and summer (Q4 and Q1). We think there will be a bit of a bounce back in autumn (Q2). And then we’re likely to see another dip from here (Q3, Q4 and Q1). Growth in 2024 will remain weak. It’s an RBNZ engineered recession.

Very restrictive monetary policy is still working its way through the economy. Monetary policy works with long lags. Over the last year, most of our mortgages rolled off low rates. And 40% of our mortgages roll onto much higher rates in the next 6 months. Household budgets are being stretched. On top of the rapid rise in interest rates, high rates of inflation have slashed household purchasing power, and falling house prices have dented confidence and the ‘wealth effect’. But it’s not all bad news…

The biggest development over the last 6 months happened at the border. There has been a surge in migration and a beautiful bounce in student and tourist numbers. Aotearoa is, and will always be, an attractive place to come for work, study or play. The bounce in student and tourist numbers will boost our service exports. And there’s plenty of upside. We’re still working our way back to pre-Covid levels. Tourism is at about 70% of pre-Covid levels… levels we will surpass. Our current account deficit should improve from here. And then there are the migrants. More foreign workers are coming and plugging the gaps in our tight labour force. They will reassert downward pressure on wage growth. At the same time, migrants boost demand for everything, including housing. The migration-induced boost to our team of 5mil, actually make that 5.2mil, has led us to revise up our projections for the Kiwi economy, but only just.

So what does all this mean? A double dip recession should cause a lift in unemployment, by RBNZ design. Cost pressures, including wage pressure, should ease into next year. Inflation rates should return to the RBNZ’s 1-to-3%yoy target band. And very tight monetary policy should be loosened. We expect to see rate cuts in 2024.

Ultimately, the surge in migration will add demand to a languishing housing market. And lower mortgage rates (into next year) will support demand. Confidence is returning already, and the demand/supply imbalance will remain fundamental to the outlook.

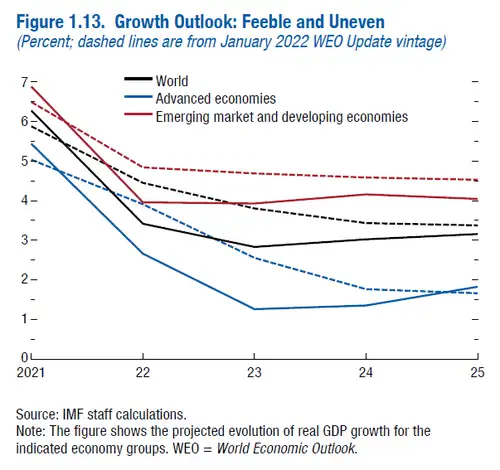

Our trading partners face “feeble and uneven” growth

When analysing the small and open Kiwi economy, it’s important to think of us on the global stage. Global growth remains low. And our trading partner growth will weaken. Despite some resilience, many economies are still absorbing the recent shocks. The pandemic has left some scars. Commodity prices have fallen back from the sharp spike following Russia’s invasion of Ukraine. But geo-political tensions remain high. Meanwhile, labour markets in many economies are running hot. And stubborn inflation has forced the (heavy) hand of most central banks. Higher interest rates continue to hamper activity, as intended.

The IMF forecasts global growth to fall from 3.4% in 2022 to 2.8% in 2023. The slowdown is heavily concentrated in advanced economies, particularly in Europe. Growth in advanced economies is forecast to drop from 2.7% in 2022 to just 1.3% in 2023. And the outlook remains bleak. Global growth is forecast to rise to 3% in 2024 and settle there for the next 5 years. That’s weak. The IMF forecasts are the lowest medium-term forecasts in decades.

Going one step further, we need to think about the outlook for Asia. When we hear of recessions developing in North America and large parts of Europe, we ask the question: what does it mean for Asia, or China in particular? And the outlook for China has deteriorated. The much-celebrated reopening of the Chinese economy has led to little more than a whimper of activity. Chinese growth has slowed to just 4.5% and inflation is surprisingly low at just 0.2%yoy. Import and export growth has disappointed. And retail sales, investment and industrial output continue to undershoot projections. Manufacturing activity remains low at a contractional rate (below 50) of 49. Meanwhile, weak Chinese growth strengthen calls for more government stimulus. The weak recovery does not bode well for us Kiwi.

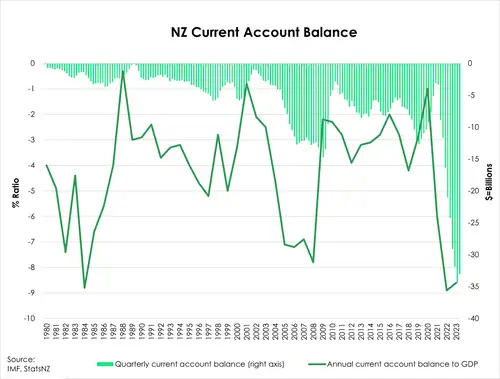

Our current account deficit (CAD) has raised some red flags. We recorded a CAD of 8.5% of GDP, or $33 billion in the year to March 2023, $8.8 billion worse than last year. Our goods exports have fallen. And commodity prices have weakened. But a large part of this deficit can be attributed to the lingering effects from the pandemic.

We’ve been here before. In 1984, amidst oil shocks and recessions, and in 2008 with the GFC, our current account deficit made up 8.8% and 7.8% of GDP respectively. And each time these recessions pulled back our deficits. So, we expect the CAD to improve. Tourism, once our largest export industry, is on the rebound. And while our import levels remain high, activity will slow as consumers pull back spending.

A double-dip recession

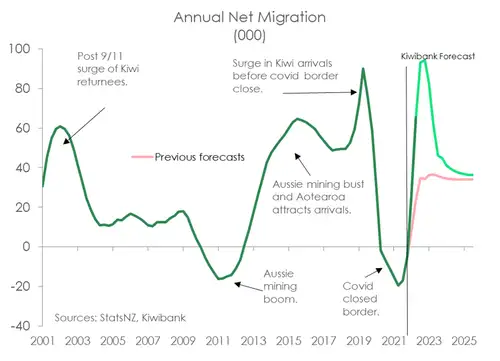

It’s been a while since our last forecast update. And a lot has happened. The biggest development over the past six months has been the surge in migration. We’ve gone from an annual net loss of 19,000 in early 2022, to a net gain of 72,000. And we’re on track to hit 95k-100k later this year. That’s a lot. And because of this migration-induced boost, we’ve revised up our growth projections for the Kiwi economy – but only just. Because migrants are arriving at a time when the economic undercurrents are weakening. Nonetheless, rising migration provides a boost to both the supply and demand side of the economy. More people means more demand for goods and services. More people also means more hands on deck, so greater production.

However, we are still expecting a continued slowing in activity. And this time, it won’t be down to bad weather or teachers on strike. The RBNZ’s sheer determination to constrain demand cannot be discounted. Having delivered 525bps of rate hikes, the RBNZ has been one of the most aggressive central banks in the fight against inflation. While the RBNZ may have called time on rate hikes, previous rate increases are still working through the economy. When the time comes to re-fix, discretionary incomes will be squeezed further. And the appetite to spend will wane.

The June quarter may see a temporary bounce back in growth. It’s a mix of cyclone rebuild and payback for the 0.8% contraction over the last six months. However, a recession later this year is still our base case. Albeit a little shallower. Because the migration-led boost, will boost demand in the economy. We have shaved a few %pts off our last estimate. We expect a three-quarter, cumulative 0.4% contraction in economic activity beginning from the second half of the year. If we include periods of (effectively) no growth in 2024, we’re expecting about 12-straight months of very weak activity ahead.

Tourism is not yet back to full strength

One upside risk to bear in mind is the ongoing recovery in tourism. Prior to the pandemic, tourism was our biggest export industry with a 20% contribution to total exports. In the year to March 2022, that contribution fell to 2.4%. It’s partly a consequence of capacity constraints. The sector remains heavily under-resourced with employment around 130k short of 2019 levels. Thankfully, the return of migrants is helping to plug the gaps. On the demand side, visitor arrival numbers are also underperforming. Tourism arrivals jumped in December last year, but the lift was short-lived.

In April, arrivals plunged 17% (seasonally adjusted) and are currently running at 70% of pre-pandemic levels. It doesn’t help that Chinese arrival numbers – our second largest market after Australia, pre-pandemic – are only slowly recovering (10% of 2019 levels). Covid restrictions in China were not unwound until earlier this year.

Judging by reports of airlines adding capacity, especially across Asia, there’s still pent-up demand for travel. The tourism sector needs a rebound in Chinese arrivals to get back to full strength. And we could see this by summer.

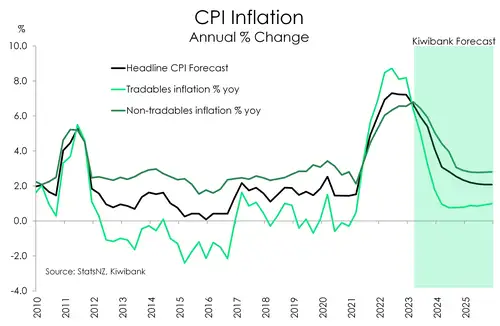

A significant slowdown is needed for inflation to return to target. Headline inflation should decelerate from 6.7% to 4% by year-end. And that’s the easy part. Favourable base effects are in play with last year’s spike in energy and food prices falling out of annual calculations. Cooling commodity prices will also help to lower the cost of imports. The tricky part is getting back to the 2% target. And it all hinges on domestic inflation – the stickier, demand-driven kind, with ongoing strength in wage growth.

Also complicating matters in the near-term is the end to temporary discounted fuel excise tax. And full price public transport resumes for those aged 25 years and older. All in all, it will take until the middle of 2024 for inflation to fall back within the RBNZ’s 1-3% target band. That’s about three months longer than we had previously forecast. And it’s not until 2025 that we see inflation back at the 2%.

The big uncertainty is the inflationary potential of the migration surge. It’s our view that the surge will prove less inflationary than previous episodes. Because rising migration is providing a boost to capacity. Employment growth accelerated at the start of the year and participation lifted to a new high (72%). Evidently, the boost to labour supply is helping to fill long-vacant job positions.

Migrants generally turn up and accept the going wage. And they are arriving as demand for labour softens. We expect the current boom to exert more downward pressure on wages than it will add to aggregate demand and inflation. Accordingly, we now see wage inflation topping out at current levels. High inflation and labour shortages have bolstered wage expectations. But with both now improving, 4.5% wage growth may be the high-tide mark.

Currently, the pace of consumer prices is running faster than wage growth. The good news is, we see the current cost-of-living pressures easing soon. By the end of this year we see wage growth exceeding consumer price inflation.

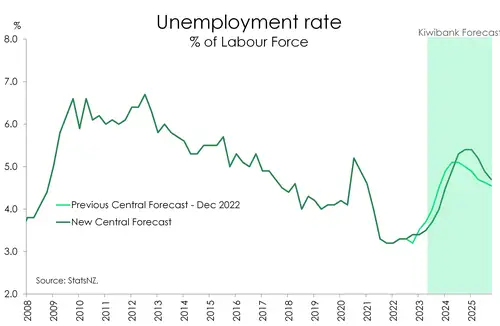

It's a tough task to cool inflation with a persistently tight labour market. But the forecast recession will see conditions loosen. As consumer demand cools, so too will firms’ demand for labour. Already, we’re hearing of firms looking to downsize their workforce. Those anecdotes will continue to stack up. There’s been a mindset shift among business, and employment intentions are weak. We are expecting the unemployment rate to track higher this year before ramping up to a 5.50% peak in 2024. That’s slightly higher than our previous forecast, and remains elevated.

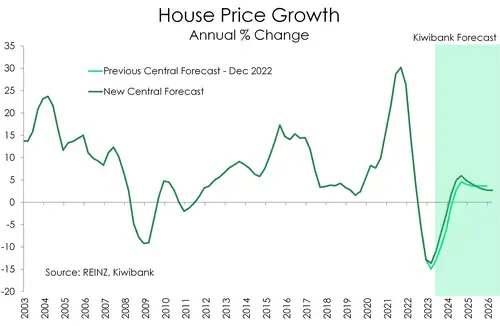

Fortunately, the tight labour market has helped cushion the blow of the housing market downturn. For the last 18 months, house prices have steadily fallen back to early-2021 levels. House prices are down 16.3% from the November 2021 peak. However, the housing market looks to have found a base. And there are tentative signs of recovery. House prices are still falling but at a reduced rate, and sales activity is picking up.

There are three drivers of the housing market. Firstly, falling mortgage rates will support confidence and activity. Secondly, the demand/supply imbalance will worsen. The surge in migration and the loss of dwellings at high risk of climate change will only exacerbate the housing shortage. And finally, the residential construction boom is coming to an end. The number of dwellings coming to market will fall back from very high levels. The growth in demand, with a migration boom, will once again outstrip supply in coming years. All three drivers point to a strengthening housing market, and price gains. We see a return to monthly house price gains – albeit very modest gains – beginning from the second half of the year. We forecast annual gains creeping up to 2% by the first quarter of 2024, before hitting a high of 6% by the middle of the year.

Interest rates should fall

We think the time will come, sooner rather than later, for interest rate cuts. As we outlined in “Are we the waiting: the RBNZ’s prolonged pause will turn to rate cuts, eventually. Interest rates should fall.” If the economy develops in a way we expect, then the RBNZ will start easing early next year. That’s an important message for Kiwi households and businesses. We may have reached the peak in lending rates. And as with all peaks, we will come down the other side. Tailwinds are coming.

The Kiwi dollar should fall too

Our forecast for the Kiwi dollar is sharply unchanged at 55c by year end (if it aint broke, we wont fix it). And we have grown in our conviction. Falling commodity prices, narrowing interest rate differentials, and weakening risk appetite should see it through. As we outlined in “The Kiwi dollar has hit an airpocket. It should be a slow descent from here. NZD to hit 55c.”

The fall in the Kiwi towards 55c will help offset weakening commodity prices for exporters. Unfortunately, a weaker Kiwi makes imported goods more expensive. We have factored in the softer Kiwi, and we still expect to see a helpful deceleration in imported inflation.

Special topic: Who’s coming, who’s going?

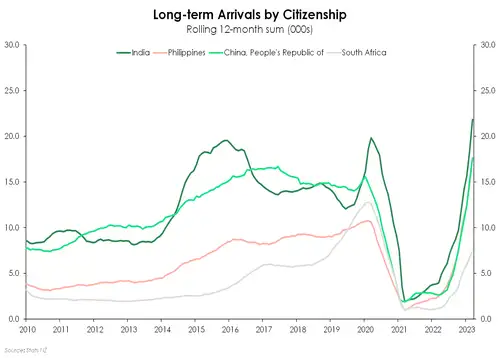

Long-term arrivals have been on a steep climb. And non-NZ migrants are at the front of the queue. It’s pent-up demand in play. Migrants whose plans to come to NZ were stymied by Covid border restrictions are coming now. In the year to April 2023, we recorded a net gain of 98,400 non-NZ citizens. Like pre-Covid trends, most have arrived from India, Philippines, China, and South Africa. And most are of a working age. In the last 12 months, over 40% of the net gain in migrants was concentrated within the 20-34 year age bracket. Arrivals on student visas are also steadily rising. And international students studying here typically move into the workforce (as most student visas allow up to 20 hours of work per week).

Migrants are helping to plug the staffing gaps that have long plagued firms in this covid era. Most are concentrated in the services sector, particularly hospitality and trades. And that’s great news. Sectors across the board have been screaming out for workers, but hospitality, horticulture and construction have been among the loudest. Food trade workers – think chefs, cooks and butchers – have climbed to the top spot, up from being fourth place in 2015 (previous boom). While Architects, Designers, Planners & Surveyors have fallen to the 20th spot, down from 12th place. And Scientists and Health & Welfare workers have been replaced by Labourers (construction and mining).

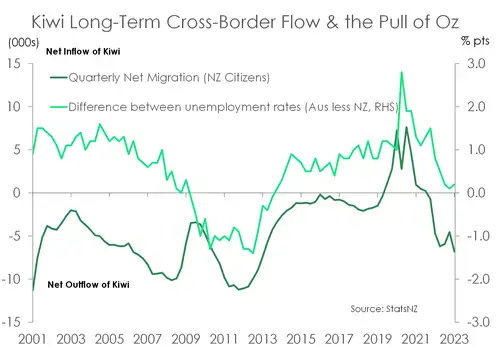

In terms of the flow of Kiwi across the border, we’ve returned to recording the typical net loss. Over 27,000 Kiwi returned home, but that was more than offset by the almost 54,000 Kiwi leaving the burrow. When it comes to migration flows, the pull of work is a powerful one. We expect the Aussie labour market to retain its relative strength over the coming months. The relative story is also a monetary policy one. The RBNZ has been far more aggressive than the RBA in slowing the economy. As a result, we could see our economy slow much faster than the Aussie economy. And our unemployment rate may rise faster than that of our Antipodean counterpart. A measurable outflow of Kiwi – bigger than pre-covid levels – is likely to persist for the foreseeable future.

Just as spectacular as the rise in migration, so too the fall back to pre-covid levels will likely be. Immigration settings are more restrictive than what was in place over much of the 2010s. Also, NZ is competing with other developed countries for skilled migrants. The net result of these forces means we are expecting a surge in annual net migration numbers to around 95k-100k by the second half of 2023, before settling to an average of between 35,000-40,000.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.