We’ve lowered our Kiwi growth forecasts

“A green plastic watering can, for a fake Chinese rubber plant, in the fake plastic earth.” Radiohead.

The failure to generate consistent and prolonged nominal growth has uneased policymakers into easing. Interest rates are falling further, and fast.

We’ve revised down our growth forecasts. Because the risks we have been wary of are coming to fruition. The RBNZ are likely to cut to 1.25%, and we still believe there’s a 40% chance of a move to 0.75%.

The NZ economy has slowed much faster than expected. Growth hit 2.3%yoy to end 2018, down from 3.4%yoy a year earlier. And we expect growth to slow to just 2%yoy in 2Q 2019. The economy is now growing below its potential – a key concern for the RBNZ in its seemingly perpetual struggle to lift inflation back up to its 2% target midpoint. Businesses are reluctant to invest, the housing market has cooled, and a deteriorating global outlook hangs over the NZ economy.

Kiwi companies remain in the doldrums, at least on surveyed paper. Firms have effectively been in a lugubrious mood since the 2017 general election, with Labour Pains. We are now seeing the consequences of an extended period of uncertainty, and low confidence. Firms are reluctant to invest, cautious in their hiring, and struggling to pass on rising costs to customers. The ratcheting up of the minimum wage, and the pass-through to higher paid workers, is one such cost. Consequently, profitability is taking a hit. And the outlook concerns many. Offshore, the global outlook has deteriorated. The IMF has revised down its growth forecasts. The US and China continue to wage a trade war, with no resolution in sight. Brexit drags on with deadline slippage ongoing. The failure to generate persistent nominal growth has uneased policymakers into easing.

Central banks around the word are responding. Here in NZ, the RBNZ cut the OCR to a new all-time low of 1.50% in May. And we don’t think the Bank will stop there. We expect the RBNZ to deliver another cut in August to 1.25%. And we still believe there’s a 40% chance the RBNZ is forced to keep going to 0.75%. The policy action is likely to support growth, we hope. Lower interest rates, and no CGT, will support the Kiwi housing market. But we are not convinced it’s enough to stimulate investment, yet. Confidence is key, and confidence is lacking.

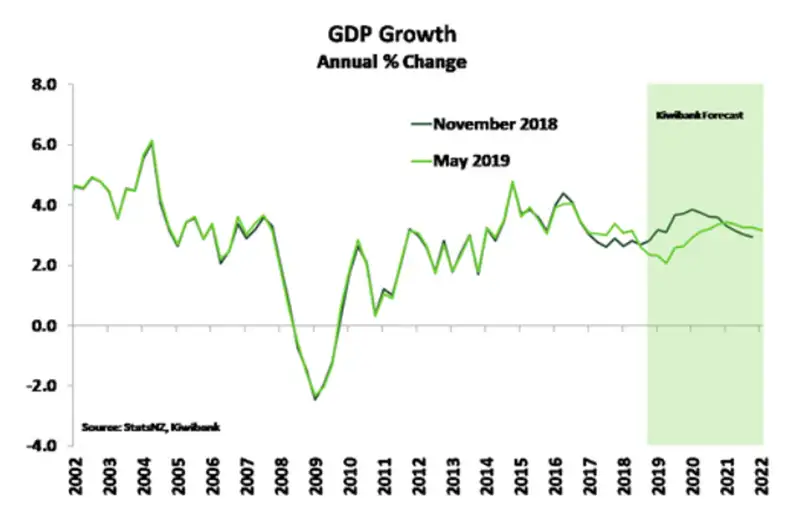

We have lowered our growth forecasts for the Kiwi economy. We now see growth peaking around 3.4%yoy in 2021. In our last forecast update in November, we had a healthier forecast peak of 3.8%yoy in early 2020. Our forecast growth is now lower, for longer. To get growth back above 3%, help is needed. Much of our forecast growth comes from government (fiscal) initiatives. But more fiscal investment is needed in the outer years, beyond 2020/21. NZ’s elevated terms-of-trade should cushion the export sector for the time being. But slower global growth may lower our export prices in time.

Monetary policy is (again) called upon to support growth.

Paranoid Android: Trump and what’s wrong with the world…

“When I am king, you will be first against the wall.” Radiohead.

The outlook for global growth continues to disappoint. Our economic potential is fading, and output is failing to meet lowered expectations of potential. There are some very large forces at play, and some crazies in charge.

Our economic potential is being inhibited by the tectonic shifts in demographics (declining fertility rates and ageing populations), which lower population and participation rates. And our productivity has disappointed due to an underinvestment in infrastructure, and education. Fiscal austerity in the post-crisis world (since 2008) has severely limited the outlook for growth.

“The persistence of low inflation and low interest rates is not a surprise when, as has been true in fact, the low interest rates fail to generate substantial fiscal expansion.” (Christopher Sims, Fiscal Policy, Monetary Policy and Central Bank Independence)

Regulation has also played a large role. The repricing of credit (money was “too cheap” prior to the 2008 crisis) is ongoing. Regulation has impacted the price, by restricting the supply of credit. Credit is the oil in the economic engine. The ramping up of bank capital requirements has yet to play out here, and abroad. Lower rates of credit creation, lower the nominal growth outlook.

And then there is the rise of the populist protectionist. The rise in “anti-system politics” is a threat to global trade, and a threat not seen since the 1930s. Trumps’ tirade may be a tipping point.

We believe these forces, particularly demographic headwinds, will have to be analysed and re-analysed for years to come.

One thing is certain, global growth rates are on a glide path lower. The problem is the recent slowdown has been abrupt. The populist protectionist president, aka Trump, is fighting on many fronts. The US-China trade tariff “war” continues without resolution. Mexico quickly succumbed to US trade threats over boarder protection to avoid a similar fate. But we suspect Trump has not finished with Mexico, or any nation with a trade surplus to the US. The populist protectionist Brexit ordeal is still unresolved, and the patience of the EU is wearing thin. The real concern for the EU, however, is the rise in anti-EU politics within. The epic recovery in equity markets since the start of the year has been halted in its tracks. Interest rates have fallen sharply as traders’ position for several rate cuts, by several central banks!

For the last 18 months we have warned of the severe risks on the horizon. Clouds of uncertainty remain, many have darkened, and we have lowered our forecasts of GDP growth. The outlook for NZ’s key trading partners has deteriorated, and forecasts of global growth by institutions like the IMF have been lowered further. Our neighbours in Australia are experiencing a sharp correction in their housing market. Australia’s economic data is also looking increasingly shaky, and Australia faces the same risks to their outlook from abroad. The RBA has cut the cash rate to 1.25%, and it looks likely the RBA will continue to 1% and below. We expect the RBA to cut to 0.75% this year.

The Bends: Where do we go from here?

“The planet is a gunboat in a sea of fear.” Radiohead.

It is not just about the cool winds from offshore that have altered the economic landscape here at home. Business confidence, already in the doldrums, fell at the start of 2019. Firms continue to face labour shortages, higher costs, and an inability to recover these escalating costs. Profitability is being squeezed. We are now seeing the consequence of weak confidence over an extended period. The lack of confidence is partly a protest vote against the Government, and the uncertainty surrounding (tax) policy. Some of the uncertainty has been removed, with the Government ruling out the possibility of a comprehensive CGT. But questions are being asked around: what tax is next? Confidence should start to recover, but the signs are only tentative at this stage.

A lift in Kiwi economic growth is likely to be gradual, and off a lower starting point. After easing further to 2% in 2Q 2019, we now see growth peak at 3.4%yoy in 2021. We had forecast a stronger rise to 3.8%yoy in 2020. But we have been disappointed. Fiscal policy hasn’t delivered what was anticipated.

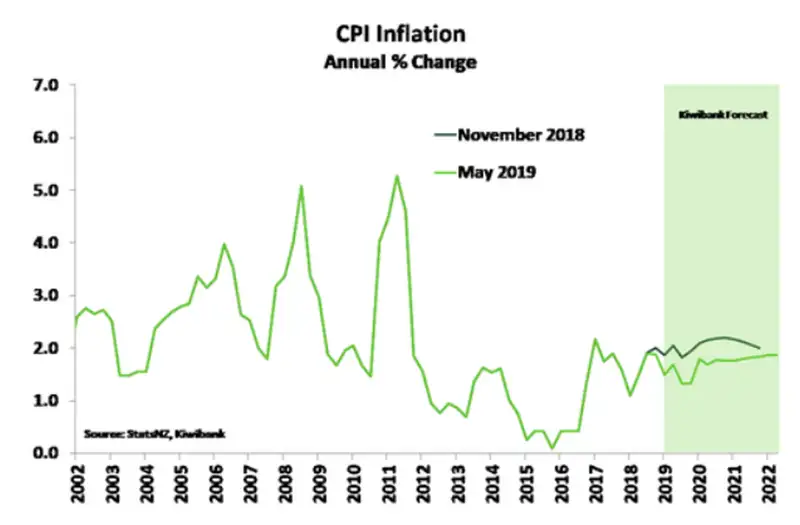

Inflation undershot expectations at the start of 2019, thanks in large part to lower imported prices. Inflation has fallen to 1.5%yoy, further below the RBNZ 2% target midpoint. Petrol prices had tumbled at the end of 2018. For the RBNZ, volatility in petrol prices can be looked through – so long as second round effects are contained. Of more concern, underlying inflation is cooling to the core. Core inflation, which excludes volatile prices, has also fallen further below the RBNZ’s 2% target midpoint. Core inflation is slow moving and provides a guide as to where inflation will settle after short-term volatility dissipates. The cooling in core inflation added to the need for RBNZ action.

The RBNZ is cutting interest rates, and growth is (still) expected to lift above potential next year. In time, inflation will lift back to target. But we have been in this position before. There are structural factors, such as globalisation and technology, that have been a persistent deflationary force. We think imported inflation will continue to weigh down prices and the road back to the RBNZ’s 2% target midpoint will be long, and bumpy.

The lack of inflation is one factor in keeping wage growth down. And wage growth remains muted despite the tightness of the labour market. The unemployment rate of 4.2% is consistent with maximum sustainable employment. Firms’ complain of the inability to find (good) workers. Yet private sector wages rose only 0.3%qoq in the March quarter. We forecast wage inflation will lift, partly because of a tight labour market and ongoing large hikes to the minimum wage to $20/hr by April 2021. The unemployment rate is expected to hang around current levels in the near-term before tightening to just below 4% next year. Beyond 2020 we expect a tick up in unemployment rate as the minimum wage hikes bite. The risk is firms chose to invest more into capital, and automate faster.

The recovery in economic growth will filter through the economy in different ways. We expect the building industry will continue to be busy. But it’s hard to see growth in construction sustaining a second leg higher. The construction sector’s contribution to growth is likely to be limited. Tourism-related spending, on the other hand, should be given a boost by the lower kiwi dollar over the first half of our forecast period. Tourism is another area of the economy facing capacity issues, so stronger overall spending may mask limited growth in tourist numbers. Turning to retail, stronger tourism-related spending should help. Moreover, rising wage growth and lower interest rates underpin consumption. An elevated terms of trade is a boon for our export sector, providing a cushion for our farmers and export-orientated manufacturers. Services sectors in the economy have been the powerhouse of growth over the last few years as strong population growth has led to a general increase in demand for all manner of services. Population growth is slowing, and will likely slow further, limiting the growth in this area over our forecast horizon.

High and Dry: Construction has surged! But will it last?

“Don’t leave me high. Don’t leave me dry.” Radiohead.

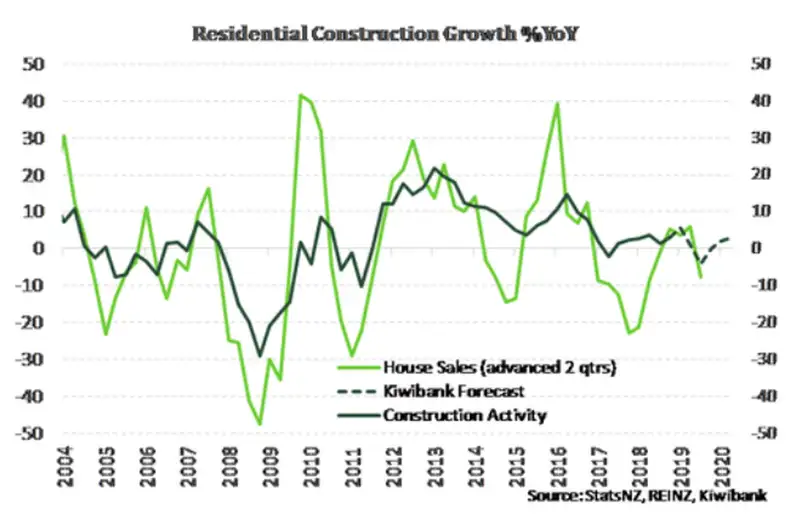

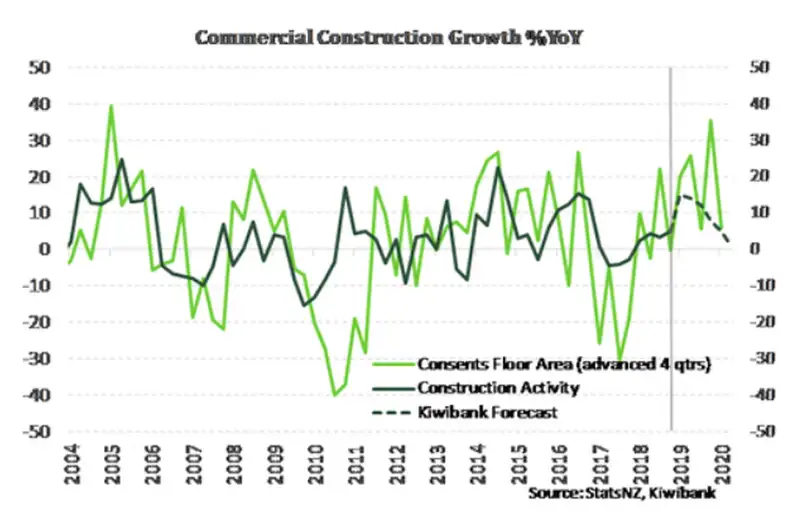

At the start of 2019 construction activity has surged according to StatsNZ’s data on building work put in place. The volume of both residential and commercial construction activity was markedly higher over the March quarter. Commercial construction activity for instance lifted 9%qoq, the largest quarterly jump since early 2014 – the height of the commercial phase of the Canterbury rebuild – leading to an annual growth rate of 17%yoy. We know there is no shortage of building work at present as the industry plays catch up to an earlier migration-led jump in population growth. But it’s unlikely the industry can sustain such stellar growth for an extended period.

Capacity constraints are a major impediment to the sector and NZIER’s quarterly business survey shows builders capacity utilisation has been periodically punching survey highs since mid-2015. In March capacity utilisation was running at 94% among builders. Moreover, looking at other details of business confidence survey’s we have seen in recent months that building intentions have fallen off a cliff, particularly for residential construction. It looks as though capacity constrains are creating pinch points for future home building. There has also been a sharp contraction in home sales, centred on a subdued Auckland housing market. Building is correlated with housing market activity. A cooling housing market reduces the incentive to build and renovate.. We expect that growth in residential-related construction will slow over the second half of this year followed by a modest recovery over 2020 to low single digit rates of growth. Mortgage rates are heading lower, investors don't have a CGT to worry about, and we still have a housing shortage to address.

Commercial construction activity has been under pressure in recent years, with well-publicised collapses of major contractors faced with cost escalations and difficulty accessing credit. But growth in this area is surging ahead. Building consents data also suggests that strong growth will hold up for much of this year. Next year is likely to be a different story. We believed that as we head into next year, capacity constraints will hold back this sector, and growth will fall sharply. A key question mark hanging over the commercial construction sector next year and beyond is the RBNZ’s proposed increased bank capital requirements. This is likely to lead to an increase in the cost and a shift of credit away from riskier lending such as commercial property.

The hardest segment of the building sector to forecast is the civil/infrastructure construction, due to the lumpy and specialised nature of it. Construction in this area contracted sharply early last year as activity wound down on the rebuild of the Kaikōura coastal highway and rail line. However, we know there are a number of large projects already well underway, including Auckland’s City Rail Link, and there is more to come. A steady pace of activity is expected here.

Karma Police: Auckland housing is still paying for past

“Arrest this man, he talks in math”

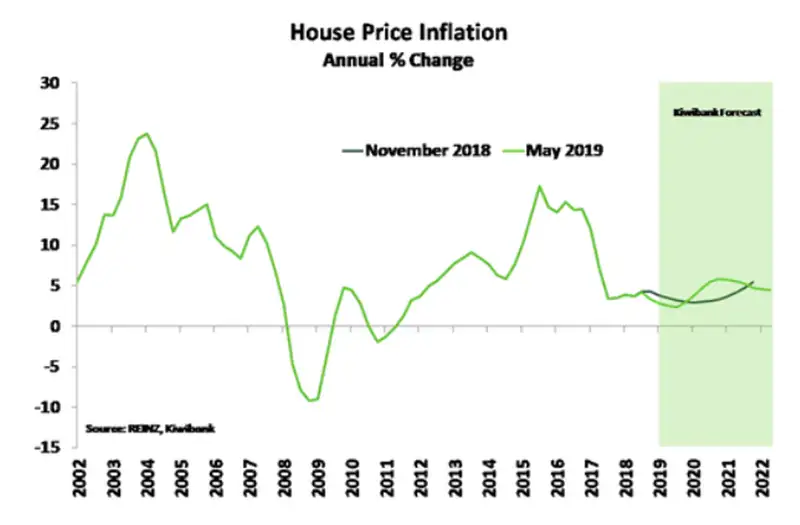

In August last year we went through the undersupply of New Zealand’s housing market. We spoke in math. And we used a model to show the undersupply. Developments have largely played out as we anticipated. Auckland has cooled, but not collapsed. Auckland house prices are down nearly 5% from the peak with more downside expected near-term. Auckland’s slowdown will eventually feed into the regions. House sales have been muted across the country. And there has been a lack of listed property. Nevertheless, we don’t expect a major correction like that seen in Australia. Auckland’s housing market is in payback for previous excesses, but remains fundamentally UNDER-supplied. A lack of housing supply is a key feature across NZ.

Government policy has weighed on investor activity (including: banning foreign purchases, removal of the negative gearing tax loophole, tightening the bright-line test), and affordability constraints are ever present. But the abolition of the planned CGT, has lifted a major concern for investors. When combined with further interest rate cuts, we expect the housing market to lift between 5-6% over 2020-21.

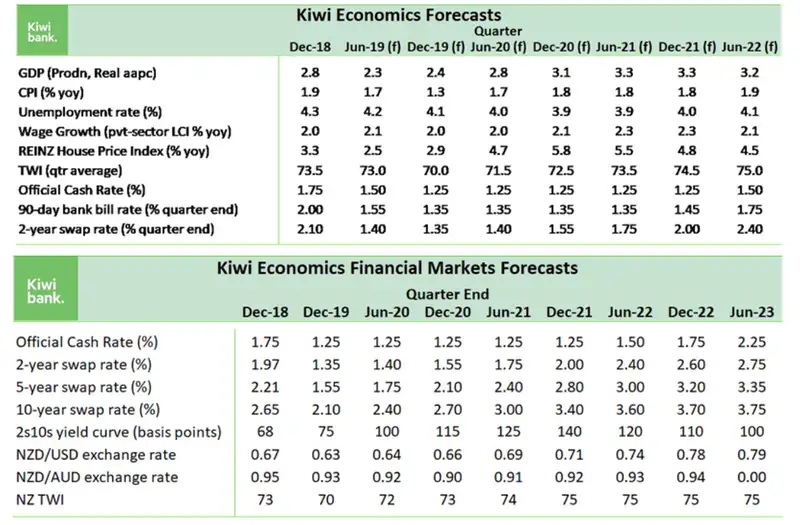

Forecast tables

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.