- Central banks are in the limelight this week. The Fed is set to begin its cutting cycle. But it’s proving a line ball call whether the first cut will be 25bp or 50bps. The Bank of England and Bank of Japan will also announce their latest policy decisions. And no change in policy is expected for both. One is looking for softer services inflation (BoE), while the other wants stronger (BoJ).

- Here at home, we will find out how the Kiwi economy fared over the June quarter. We expect another sombre report with a 0.4% decline in activity and most industries contracting.

- Our COTW looks at the latest migration data. Monthly net inflows have gone from averaging over 10k last year to under 4k this year. And the annual balance has fallen to around 67k. Arrivals are falling, but it is the rapid rise in departures that is driving the slowdown in net inflows.

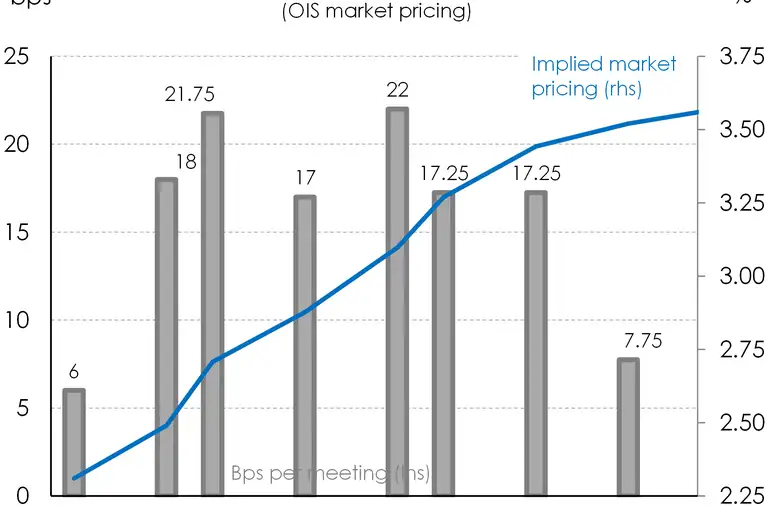

Strap in for Super Thursday. It’s all happening. And it begins with the U.S of A Federal Reserve finally kicking off its cutting cycle. The Fed is expected to deliver its first rate cut in four years. But the jury is still out as to whether the first cut will be by 25 or 50bps. A 25bps cut would be the safest bet, and Fedspeak did not signal any urgency for the bigger cut. Whether it’s 25 or 50, of greater interest will be the Fed’s updated dot plot. The June projections reduced the amount of expected easing to 25bps from 75bps. But the 2025 outlook was bolstered to 100bps of easing from 75bps. With another two meetings remaining, we’d expect the new dot plot to signal at least 75bps of total cuts this year.

Back home in NZ, we’ll also see how the Kiwi economy performed over the June quarter. And by our estimates, it’s looking like we’ll have another contraction to add to the long recession which began in 2022 (see our full review)

For most of 2023 we flagged and warned that the Kiwi economy would go through a ‘double dip recession’. And we did. We went through a cumulative 0.8% decline over the summer of 2022-23. Then another cumulative dip of 0.4% over the second half of last year. And now, we’re potentially gearing up for a ‘triple trough recession’. At least that’s what the RBNZ is pencilling in. The Kiwi economy is starting to sound like an (very sad) assortment of ice cream flavours. Double dip, triple trough, or more like “Rocky Road.” Officially we may record 3 dips. But for households and businesses, it has been 2 years of unrelenting recession.

We expect a 0.4% decline in activity over the June quarter. The RBNZ expects 0.5%. If so, that would mean the Kiwi economy contracted in 5 of the last 7 quarters. Compared to last year, the economy would be 0.7% smaller.

It’s pretty sombre at the end of the day. But it’s the outlook that matters most. And thankfully, the outlook is much, much brighter with the commencement of the RBNZ’s rate cutting cycle. We continue to forecast, with a much greater degree of confidence, that 2025 will be a better year than 2024.

To wrap up Super Thursday, Aussie jobs data will likely show employment growth just managing to keep pace with the rise in labour supply. The unemployment rate is expected to remain at 4.2%, well below ours of 4.6%. A relatively stronger Aussie labour market has implications for our migration outlook (see COTW).

The fun (and volatility) however carries on. Hot on the heels of the Fed, the Bank of England and the Bank of Japan will both announce their latest policy decisions. And both are expected to keep rates unchanged. The BoE will likely skip this meeting after cutting by 25bps last month. Like some of its peers, a cautious approach to easing policy settings is being taken as inflation lingers. The BoJ on the other hand may wait for further confirmation that solid wage growth is feeding through to services inflation before it decides to lift interest rates once again.

Financial Markets

The comments below were provided by Kiwibank traders. Trader comments may not reflect the view of the research team.

In rates, markets flirt with a 50bp from the Fed:

“A relatively quiet week in Kiwi rates as markets remained in holding pattern ahead of FOMC decision this week. In saying that NZD rates ended the week a sizable 10bps lower. This was in line with moves in global yields driven in part by a significant fall in oil prices, signalling weakness in the outlook for global growth.

In the short end, the market continued to flirt with a 50bps cut from the FOMC this week, though CPI data didn’t provide the Fed much in the way of pretext. Meanwhile the ECB delivered their second 25bps cut downgrading their growth forecast at the same time.

Locally, we got releases of a range of high frequency measures, all still very weak but rebounding slightly off their lows. Notably, Selected price indices signalling weaker inflation in Q3. On the supply front Westpac are launching a 5-year senior transaction first in over a year.

This week is jam packed with data and central bank decisions. GDP will be the focus domestically though may get lost in the mix after FOMC decision on Thursday. With RBNZ forecasting -0.5% unlikely to see a downside surprise so would seem risk is for a strong print.” Matthew Crowder, Balance Sheet Manager – Treasury.

In currencies, the week ahead could provide a catalyst for the Kiwi to move lower:

“The last couple of weeks have seen the Kiwi dollar relatively well supported, albeit in a fairly familiar range. The Kiwi has been stuck in a 0.6080 – 0.6250 range as the US dollar has lost some ground as traders prepare for the Federal Reserve to kick off their rate cutting cycle, which is most likely to commence this week. Some widening concerns around the performance of the US economy have also been a major theme. As the data points continue to point to a softening on the US labour market, investors have become concerned that the US will not be able to achieve a soft landing at the end of their restrictive rate period. This has increased the rhetoric from some market participants, for the Fed to deliver a larger 50bp cut this week. Over the past week traders were focused primarily on the likelihood of an outsized 50bp cut, but the more likely outcome (in our opinion) is that the Fed will deliver a regular 25bp cut, and signal a more cautious stance around the risks of reigniting inflation. This outcome would likely drive a rebound higher for the US dollar, which has potentially been oversold based on too much pessimism around the US economy. A break higher for the Greenback, should see the Kiwi back to the 0.6080 level or lower. Later on the same day, the NZ GDP print for Q2 is due out. We are expecting it to be a lacklustre print, with a likely contraction of -0.4%. This data is lagging, but should the Fed take a more cautious stance, it should provide a little more of an argument for the Kiwi dollar to head lower. We have a similar view for the NZDAUD cross. It should trickle lower as the real divergence in rate outlooks between the RBNZ and RBA come into play. Conversely, a big dovish cut from the Fed could see the Kiwi higher again….watch this space.” Mieneke Perniskie, Trader - Financial Markets.

Weekly Calendar

- Here at home, the June quarter GDP report is due out on Thursday. Economic activity is expected to have contracted 0.3% following the 0.2% increase over Q1. Similar themes are expected, with weak retail sales and construction activity leading the decline. Economic output per capita likely shrank for the seventh straight quarter.

- The US Federal Reserve is widely expected to lower the fed funds rate this week, but the jury's still out as to whether the first cut will be by 25 or 50bps. A 25bps cut would be safest bet, and Fedspeak ahead of blackout period did not signal any urgency by FOMC officials for the bigger cut. However risks are titled toward a quickly weakening labour market which may prompt the 50bps move. Alongside the policy decision, the Fed will also publish its new set of economic projections and an updated dot plot.

- A day after the Fed, the Bank of England will announce its latest policy decision. The BoE is expected to keep rates unchanged, after its 25bp cut at the August meeting. Like some of its peers, the BoE will likely take a cautious approach to easing policy settings. The persistent strength in services inflation casts doubt on the return to 2%. Potentially supporting a cautious easing cycle, UK inflation data - due before the BoE's policy decision - is at risk of a re-acceleration. Market consensus expects the headline rate to remain at 2.2%yoy in August, however services inflation is expected to pick up to 5.5% from 5.2%.

- The Bank of Japan will announce their latest policy decision. Market consensus expects the BoJ to keep its rate unchanged, but may signal further hikes later this year. Wages are running at pace, and hot inflation prints point to risk of inflation overshooting the BoJ's 2% target. A hike in October is on the table. Ahead of the BoJ policy meeting, Japan inflation data will be released. Core CPI is expected to increase 2.8% in August from 2.7% as solid wage increase feed through to consumer prices. Services prices in particular is expected to accelerate, which the BoJ would receive favourably.

- Across the Tasman, Aussie employment data is also due out on Thursday. Employment is expected to grow at a modest pace, adding 25k jobs over August, just enough to keep the unemployment rate unchanged at 4.2%. Labour supply continues to grow quickly, fuelled by immigration and high levels of participation.

See our Weekly Calendar for more data releases and economic events this week.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.