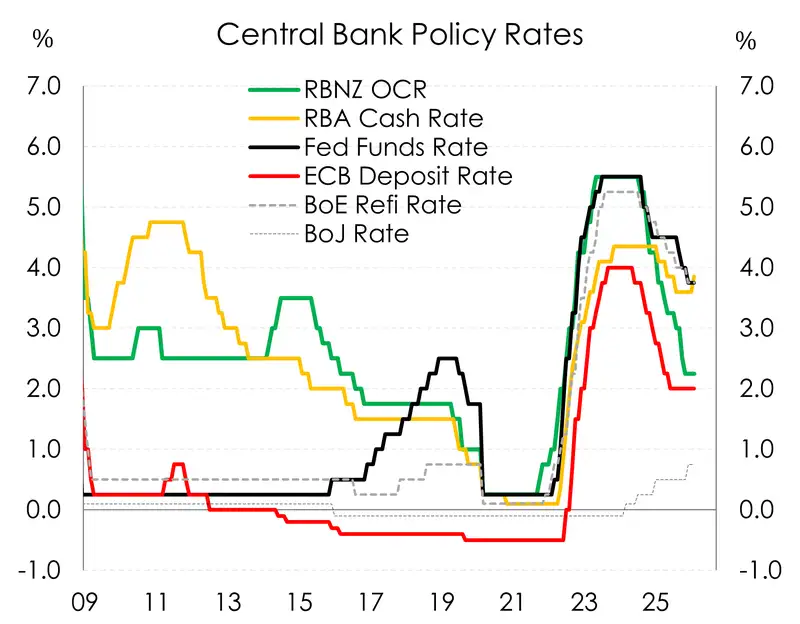

Alongside all the war headlines we also had a bonanza of Central banks meetings over the last week to keep us busy. The decisions from all were virtually as called by markets. With the Fed, BoE, ECB, BoJ, BoC, and Swiss bank all keeping rates steadily on hold. While the RBA, under a close 5-4 vote, lifted the cash rate 25bps to 4.10%.

For those that kept rates steady and on hold the overall tone last week was broadly wait and see with acknowledgements to both the upside risks of inflation and downside risks to growth. Just some differences in tone around the edges.

But it’s worth highlighting the move from our neighbours down under. The RBA is the only central bank that raised rates last week, and that only by the nearest of margins. We stand firm that the Kiwi economy is in a very different position to the Aussies, and so we don’t see this as a risk that the RBNZ will follow suit.

The RBA voted 5-4 to hike the official cash rate last week. This is the second hike in a row for the RBA, raising the OCR 25bp from 3.85% to 4.1%.

The split-vote is a reflection of global uncertainty and high Aussie inflation. Unlike New Zealand, Australia’s economy has been running hot, with a tightening labour market and higher than expected growth since February. The disagreement between board members centred around timing, with all members agreeing that a hike was needed, but some tempted to hold out until May. This is completely different to the Kiwi economy. Our labour market is still showing signs of large spare capacity and low demand.

The conflict in Iran and subsequent oil price disruption is increasing the downside risk to the global and Australian economy. The resulting higher petrol prices will act as a tax on consumption while also adding to inflation. However, Governor Bullock was clear, the RBA believes that higher fuel costs will not slow demand enough to bring Australia’s inflation down on their own. New Zealand is more likely to feel the downside risk to demand from the increased oil prices, because our demand never really got a good chance to heat up in the first place. Comparing the Kiwi and Aussie economies, if they were pots on the stove, the Kiwi economy is luke-warm at best, while the Aussie is starting to simmer. The RBA wants to make sure their pot doesn’t boil over, while the RBNZ should be trying to make sure that the Kiwi doesn’t grow completely cold. All that to say that our view on next week’s RBNZ decision is that they will hold and that rate hikes are not a part of the story for New Zealand in 2026.

Another central bank holing last week included Canada’s BoC which is set to look through the conflict’s near-term inflationary effects. Although Canada is sitting at 2% inflation, a much more comfortable spot for their economy than the Kiwi 3.1%, we feel that a similar approach is needed at home. The Canadians quoted slack in their economy and the expectation that higher gas prices will “squeeze consumers, leaving them with less income for other spending” – exactly our view.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.