The correction we had to have, actually, the correction the RBNZ made sure we had, is lingering. High interest rates are restraining demand. House prices are up 4% from the May 2023 low, but remain 14% below to November 2021 peak.

The last few months are hard to gauge. We’ve been through the strong seasonal period, without conviction. But activity is showing signs of improving. And prices will follow. The new coalition Government’s policy changes are a positive.

Interest rates will play a big role. Rates may rise a little more. And then they may fall, later in the year.

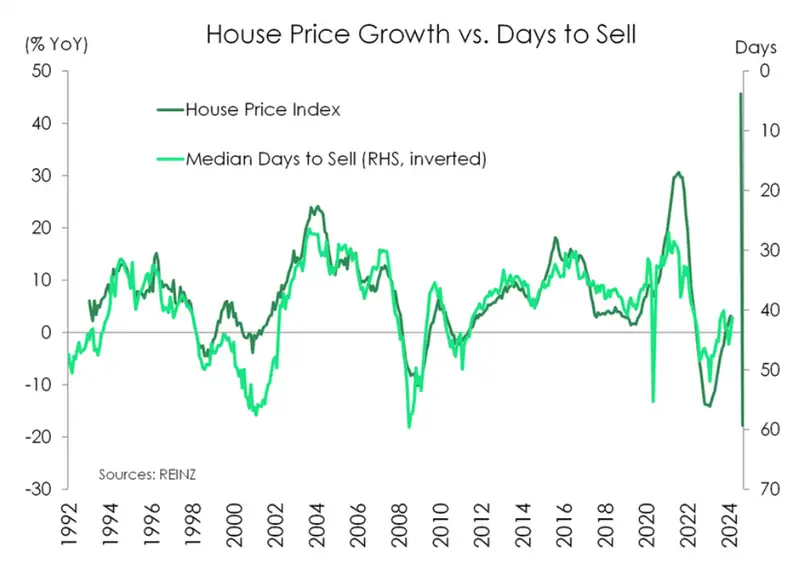

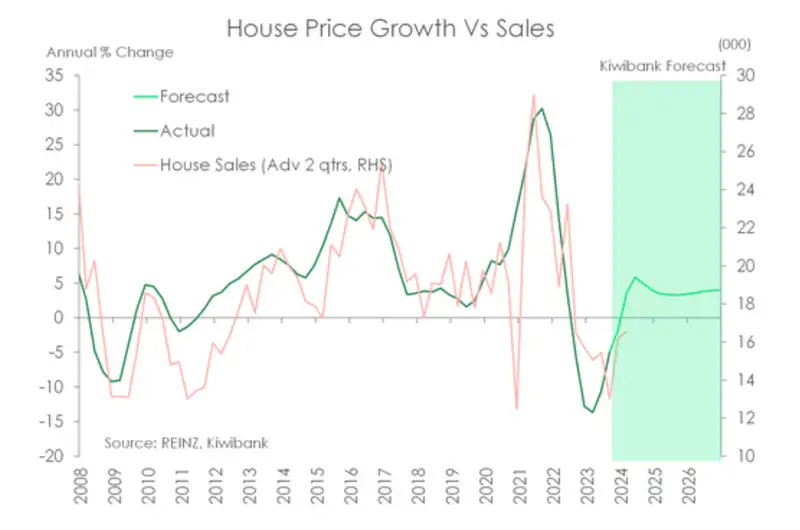

The latest REINZ data for March showed another step back, falling 1.2%. Most regions recorded declines. And it’s one of the busiest months of the year. The housing market is still struggling to regain its footing. The correction that started in November 2022, and lasted 18 months to May 2023, recorded an 18% decline (with price falls recorded in 15 of the 18 months). The RBNZ induced correction followed “unsustainable” price gains over 2020-21, with an eyewatering 45% spike in 18 months. And here we are, recovering without conviction (yet). The annual gain in house prices sits at just 2.6%. We’re back in the black, after being deep in the red, but confidence is grey.

The enthusiasm that followed the change in Government, mainly from the investor community, has waned. Anecdotes from our mortgage managers and client base were very positive towards the end of last year. Now we’re all waiting. It’s hard to get too excited when the rampant rise in interest rates is still feeding through. And homeowners and buyers are hanging out for rate cuts, later in the year.

We expect the market to regain momentum. But it may take a rate cut. And we’re not expecting one until November. Rate cuts are needed to encourage investors to invest, developers to develop, buyers to buy and of course sellers to sell.

Days to sell declines

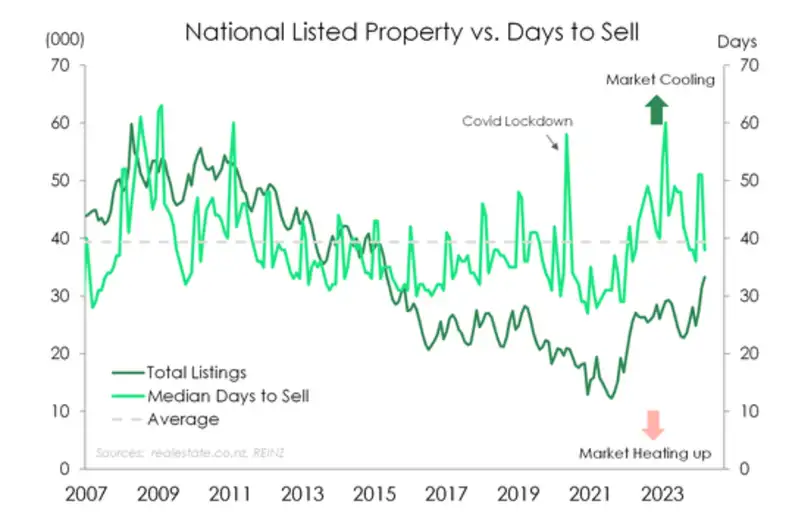

There was some good news in the dreary report. After peaking around 52 days (national seasonally adjusted) in February’23, the days to sell fell to 40 in October, bounced to 46 in January, and then fell back to 41 in March. The long-term average is 39. 41 is a great deal better than 52. The time it takes to sell a property is one of the best real-time indicators of housing market dynamics. And despite some volatility, (volatility that will persist for the rest of the year), the distance between buyers and sellers is narrowing.

The two capitals followed each other south

In the capital, house prices fell 1%. And Wellingtonians will be weighing up the impact of significant job cuts in the public sector. There will be flow on effects. Prices are up 4.7% in Wellywood over the year, but follow a sharper 25% correction. Wellington has underperformed. Sales were soggy, but the days to sell held at a respectable 38 days.

In the real capital, house prices are up a little over 2%. The city of sales (or lack thereof) activity was weak over the month, despite the days to sell easing a little to 40 (from 42).

Most regions recorded declines over the month, with a hefty 2.7% contraction in Northland. If prices didn’t fall, as in the mighty Hawkes Bay, Manawatu, Marlborough and Tasman, they merely bounced from previous declines.

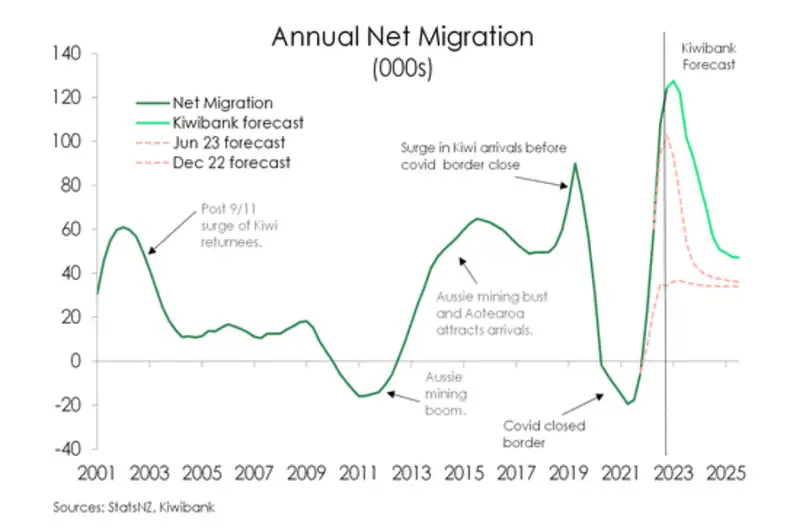

The migrant boom is massive

Any discussion around the Kiwi housing market must involve the migration boom. Back in 2022 we made what we thought was an assertive, well above consensus, forecast of a net 40,000 permanent migrants in 2023. We soon saw the avalanche coming, and bumped out forecast to 100,000. Again, it was well above consensus. And we ended up with 130,000… a new record intake. More people means more housing. And housing is already in short supply.

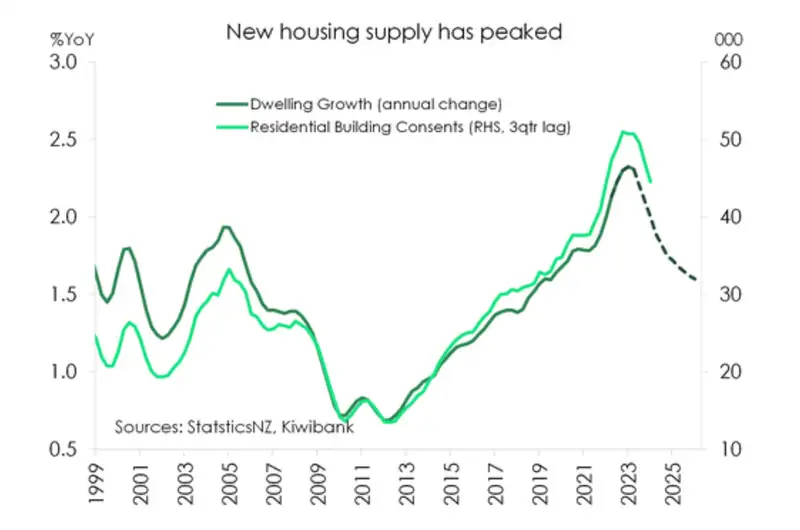

In previous publications we've commented on the drivers of the Kiwi housing market and the monumental movements in migration, and the chronic shortage of dwellings. We've talked through our recent experiences, and the likely path forward. Basically, we have a housing shortage, exacerbated by surging migration, complicated by climate change related risks, and our policymakers focus more on demand than supply. Supply is the issue. It is increased (or elastic) supply that will better balance our housing market. It’s not about limiting demand.

So, what is happening with supply?

At a time when we need the supply of homes to surge, to meet migration demand, we’re seeing a fall in consents. Over the last year or so, the decline in housing activity and prices have seen builders scale back. It’s expensive to build in NZ, for a variety of unacceptable reasons. And developers are no longer getting the premium price they need. Pre-sales are also soft.

The good news is we’re getting builders. Our migration stats show us that the largest group of migrants are tradies. So we’re increasing our capacity to build. What we need is a stabilising in house prices – and it’s happening now – to shore up demand and therefore boost supply.

So, what can we expect?

Forecasting is as much an art as it is a science. And we still think we’re much more likely to see price gains over 2024.

The surge in migration will play a big role. The demand/supply imbalance will worsen. The surge in migration and the loss of dwellings at high risk of climate change will only exacerbate the housing shortage. The new Government will play a big role. Because the ‘promised’ reintroduction of interest deductibility, shortening the Brightline test timeline, and possible watering down of the CCCFA, will entice investors. Any added infrastructure spend or incentives for new builds will also be welcomed. Interest rates will also play a large role, eventually. We think rates will fall late in 2024.

Our best guess is house prices will rise by 5-to-7% this year. Call it 6% to sound precise.

Just don’t look offshore

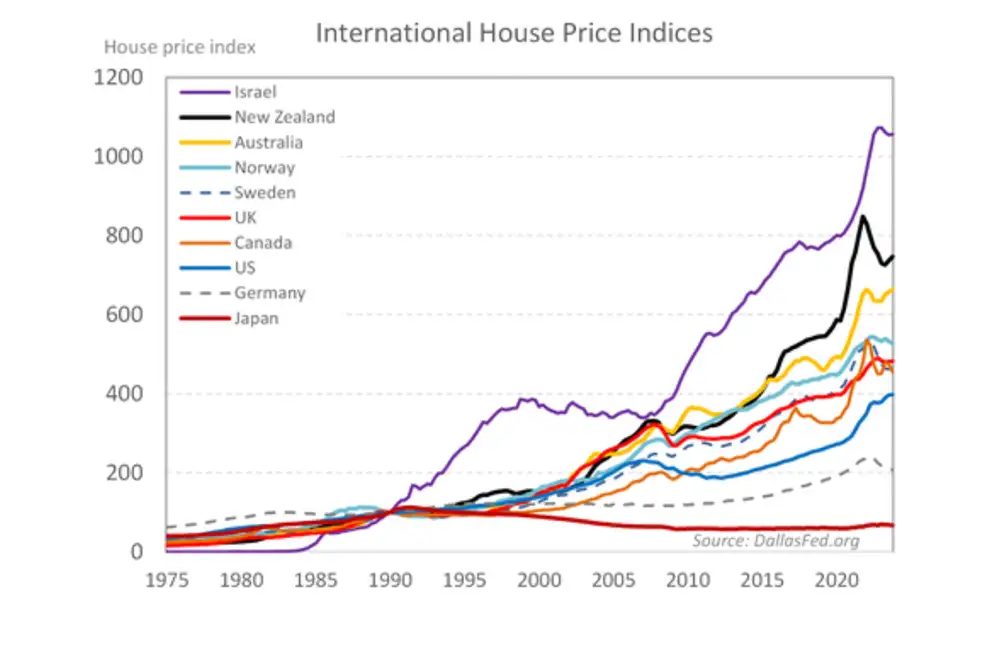

Many analysts look at Kiwi house prices through an international lens. And their minds explode. The rampant run in Kiwi house prices, post-Covid, has outpaced all developed economies, except for Israel. And the affordability problem, a symptom of the lack of supply, has worsened. It’s not apples for apples. It’s apples for pears, oranges, raspberries and kiwifruit.

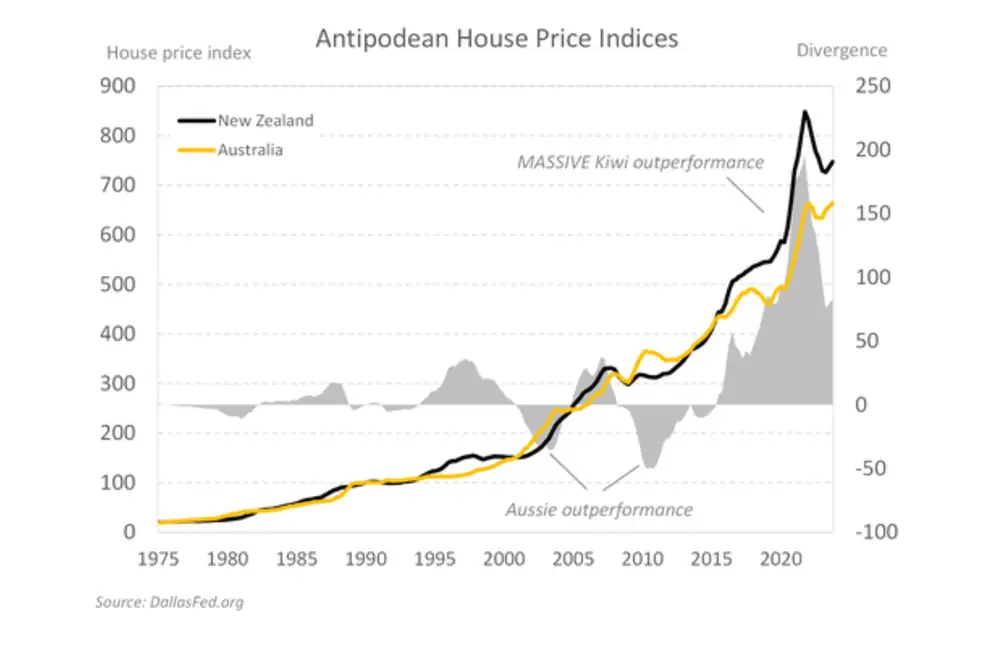

But we do like comparing to Australia. We are very similar in our differences. And we’ve outperformed, MASSIVELY. Both Antipodean housing markets took off in 2020, with peak madness in the December quarter of 2021.

The Kiwi market pulled back by around 17% from the peak in 2021. Whereas the Aussie market pulled back around 4-5%. The Aussie market has outperformed, recently. But for those in the market over the longer term, Kiwi prices have still outperformed. Why? Well, the Australians know how to maintain their infrastructure. They’re better at building infrastructure for the future (not trying to catch up for the past). And they can build a house, cheaper, faster and better. As a

Kiwi, it hurts saying that. But it’s undeniable.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.