The RBNZ revealed an upwards bias to inflation risks and will not call job done until they see the fruits of their labour shown with inflation back down to 2%.

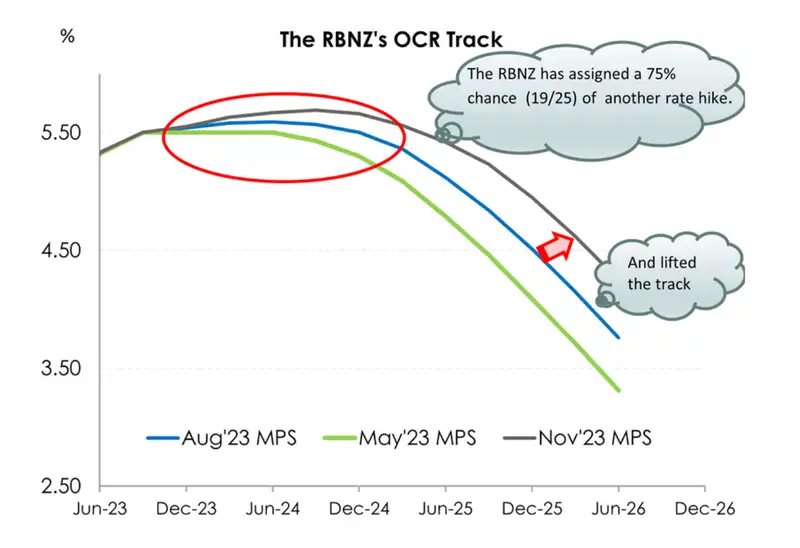

Despite a number of data points which would have suggested the end of the tightening cycle, the RBNZ have kept the door wide open for another hike. Lifting the OCR track to 5.69% by September 2024, signalling a 75% chance of a hike.

The timing of cuts is getting pushed further and further into the distance. We fear the downside risk of a softening global backdrop and the high interest rates which are still making their way through the economy. But we have to take the RBNZ’s word. Rate cuts are not looking likely anytime soon.

“…capacity pressures are assumed to decline by less than in the August Statement over the projection, supported by strong net immigration, a higher outlook for house prices, and stronger government investment over the medium term. World interest rates have also increased, placing downward pressure on the New Zealand dollar exchange rate and, all else equal, boosting inflationary pressure within the economy.” (RBNZ Nov MPS)

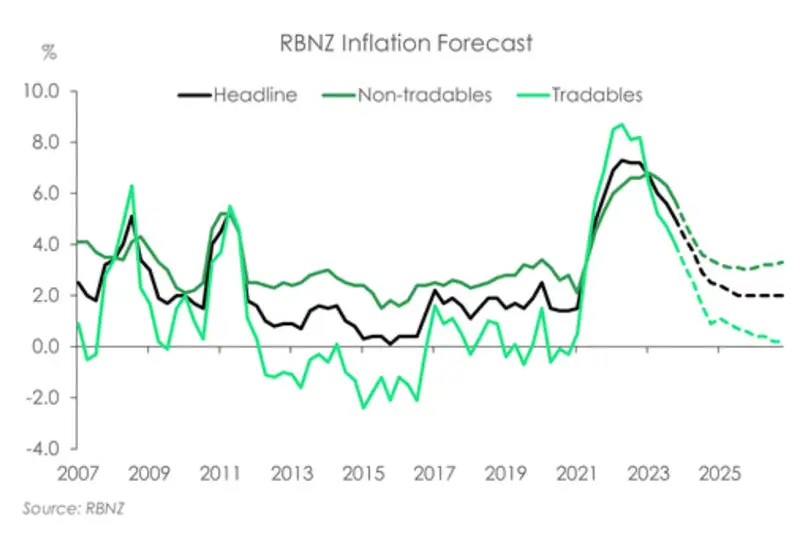

The RBNZ left the cash rate unchanged at 5.50% - no surprises. But the OCR track was lifted from 5.59% to 5.69% - big surprise. The RBNZ came out a lot more hawkish than expected. Inflation came in below their August expectations. But the RBNZ made clear that the champagne’s still sitting on ice. Rapidly decelerating imported inflation is doing most of the work in bringing down headline inflation. Domestic inflation is a slow-moving beast. And risks are tilted to the upside. Upside risks for which the RBNZ holds very little tolerance. Inflation has been sitting above target since mid-2021, and is forecast to remain above 3% for another 12 months. It’s going take some time before we get back to the 2% target. And the RBNZ is running out of patience. The RBNZ made clear that they’re “willing” to hike rates again if needed. Inflation expectations have become unanchored, and their credibility is under threat.

Some members noted that inflation has now been above target for some time, and that there should be a low tolerance for any increase in the time to return inflation to target.RBNZ Nov MPS

Everything washes out in the OCR track. And it was more hawkish than we had hoped. The key message in the track is that the RBNZ is willing to raise the cash rate again. The RBNZ lifted the OCR track to 5.69% by the September 2024 quarter. So odds are on (75%) for another rate hike and way out in 2024. We were surprised by the move. The RBNZ is clearly putting more emphasis on the growing demand impulse of the current migration boom. There’s greater risk that the boost to aggregate demand and housing (specifically rents) will outweigh the deflationary force of greater supply capacity.

There’s no doubt that a higher track was presented to also remind markets that “higher for longer” remains the rhetoric. Influenced largely by offshore developments, wholesale rates have recently drifted lower – effectively loosening financial conditions. And that’s not something the RBNZ wants here and now. What they do want is for rates to remain restrictive to continue weighing on household consumption and broader economic activity. Wholesale rates and therefore mortgage and other lending rates, need to stay high and dry. And the threat of further rate hikes does just that.

The other, somewhat academic, rational for the move higher in the OCR track was the upward revision to the guesstimated “neutral rate” – the Goldilocks interest rate that’s not hot or cold, it’s just right. The non-contractionary rate was lifted in the August MPS, from 2% to 2.25%, resulting in a higher track. And we saw the same play out today. The neutral rate was revised up 25bps to 2.50%. That’s the RBNZ’s way of saying the current level of interest rates don’t hurt as much as they’d like. The current cash rate is a little less effective in constraining demand. So basically, monetary policy is not quite as tight. And, in their eyes, we can handle a little higher rates.

But the hawkishness didn’t stop with the lift in the OCR track peak. Thoughts of rate cuts were also squashed. The new track has now pushed out the first rate cut to 2025, which would mean RBNZ staying on hold for ~2 years! We disagree. We acknowledge that the risk over the next 6-9 months is tilted toward further tightening. The RBNZ admitted an upward bias to rates. But we still believe the RBNZ will be in a position to normalise policy next year. Rate cuts could well be a 2024 story. Just later in 2024. We expect the inflation rate to be back within the 1-3% target band by mid-2024, and confidently returning to the 2% target. In saying that, our initial call for May is proving optimistic, at this stage. The RBNZ will want more data under its belt, specifically inflation prints, before changing direction. We now pencil in the first rate cut in November next year.

Inflation is public enemy no.1 and remains at large

Another forecasting round paints a resilient economy, supported by the current migration boom. In the RBNZ’s eyes, a fast-growing population is boosting aggregate demand. So much so, that an outright recession is no longer forecast for the Kiwi economy. Previously, the economy was expected to contract a cumulative 0.4% over the second half of 2023. But that’s now been stripped out on account of a stronger economic starting point (June quarter rebound) and the demand impulse from high migration. Both developments suggest a higher estimated output gap – the extent to which demand is running above potential output. The economy is still expected to slow in the coming quarters as high interest rates continue to weigh on activity. A slowdown is needed, if inflation is to return to target.

Headline inflation may have printed well below the RBNZ’s August forecasts. But for the RBNZ, that wasn’t worth celebrating – yet. The committee was strong in making their point that core inflation remains too high. Globally, headline inflation has fallen. And this, along with lower commodity prices has helped to drive our headline inflation lower at home. Lower inflation amongst our trading partner nations means we’re importing less inflation.

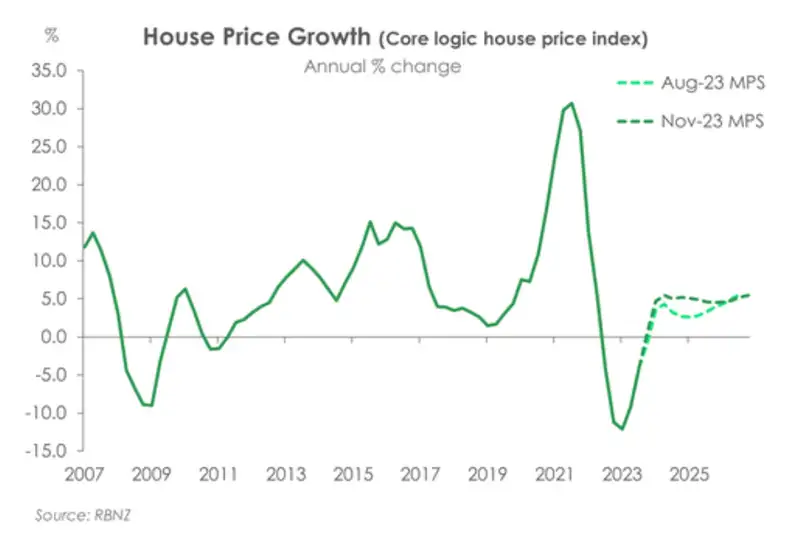

Nonetheless, it's the slow-moving domestic (non-tradeable) inflation, driven by a still-tight labour market, rising house prices and rent increases, that is the RBNZ’s biggest concern. Strong net migration is boosting productive capacity which is putting downward pressure on wage growth. Back in August, the RBNZ was expecting wage growth to fall below 4% in Q1 2023. But we’re likely to get there sooner, with a forecast fall to 3.8% by the end of the year. However, as the RBNZ sees it, the demand impulse of net migration is gaining traction. The housing market is recovering, with prices on the rise. And rents are elevated and increasing. All underpinned by a growing population.

Wage growth and the housing market are two of the strongest forces that drive domestic inflation. A slowing in the former is good news for domestic inflation, while a rebound in the latter – not so much. And according to the RBNZ, the net effect is expected to be more inflationary. Sticky domestic price pressures frustrates the RBNZ’s job in returning headline inflation to target.

Upcoming inflation prints will be even more closely watched – and in light of the RBNZ’s forecasts. “If inflationary pressures were to be stronger than anticipated, the OCR would likely need to increase further” (RBNZ Nov MPS). Downside surprises are very much welcome. But when it comes to upside surprises, the RBNZ has very low tolerance.

Special Topic: A change in the length of monetary policy lags

Beyond the lift in the track and revised forecasts, the RBNZ has snuck some further important comments within their special topic section. At first glance, the topic appears to be just another explainer about the lags of monetary policy. Changes to the OCR are never instantaneous. It takes time for higher interest rates to make their way through the economy and affect inflation. That’s something we are hard on communicating because any hasty over aggressive policy moves can cause unnecessary additional losses to output later. It’s what we’ve been warning for all along. Especially with 30% of the mortgage book yet to roll onto higher rates. The RBNZ continues explaining these lags and the transmission channels through which monetary policy works. Then all of a sudden…Bam! Another bombshell.

The RBNZ have lowered their estimate on how long it takes for monetary policy to work its way through the economy… Though it’s a very complicated and obscure estimation to make, previous empirical studies had suggested it takes about eight quarters (two years) for monetary policy to have its maximum effect on inflation. But having done some empirical research themselves, the Reserve Bank now believe it only takes an average of six to nine quarters for monetary policy to reach peak transmission depending on the estimation approach used.

Given the Reserve Bank began their aggressive monetary policy in July of 2021 through to May 2023, they believe most of the monetary policy tightening to date has already reached its peak impact on inflation. It’s important to stress that this does not mean that the transmission is over, but rather that the impacts are unlikely to get much larger over time. Certainly, a factor behind today’s hawkish statement and lift in the OCR track.

RBNZ Statement

The Monetary Policy Committee today agreed to maintain the Official Cash Rate (OCR) at 5.50%.

Interest rates are restricting spending in the economy and consumer price inflation is declining, as is necessary to meet the Committee’s Remit. However, inflation remains too high, and the Committee remains wary of ongoing inflationary pressures.

Internationally, economic growth has been stronger than was expected at the start of this year but remains below trend and is likely to slow further. This subdued growth outlook will continue to restrain New Zealand’s export revenues.

In New Zealand, demand growth has eased, but by less than anticipated over the first half of 2023 in part due to strong population growth. The OCR will need to stay restrictive, so demand growth remains subdued, and inflation returns to the 1 to 3 percent target range.

Wage growth has eased from recent peaks. Demand for labour is softening, with job advertisements now below pre-COVID-19 levels. At the same time, strong inward migration is increasing the population and adding to labour supply.

While population growth has eased supply constraints, the effects on aggregate demand are becoming apparent. This is increasing the risk of inflation remaining above target.

The Committee is confident that the current level of the OCR is restricting demand. However, ongoing excess demand and inflationary pressures are of concern, given the elevated level of core inflation. If inflationary pressures were to be stronger than anticipated, the OCR would likely need to increase further.

The Monetary Policy Committee agreed that interest rates will need to remain at a restrictive level for a sustained period of time, so that consumer price inflation returns to target and to support maximum sustainable employment.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.