Lifting just 0.5% over the December quarter the annual inflation rate has fallen from 5.6% to 4.7%. Don’t get us wrong, its good news. But deep down we were hoping for a downside surprise.

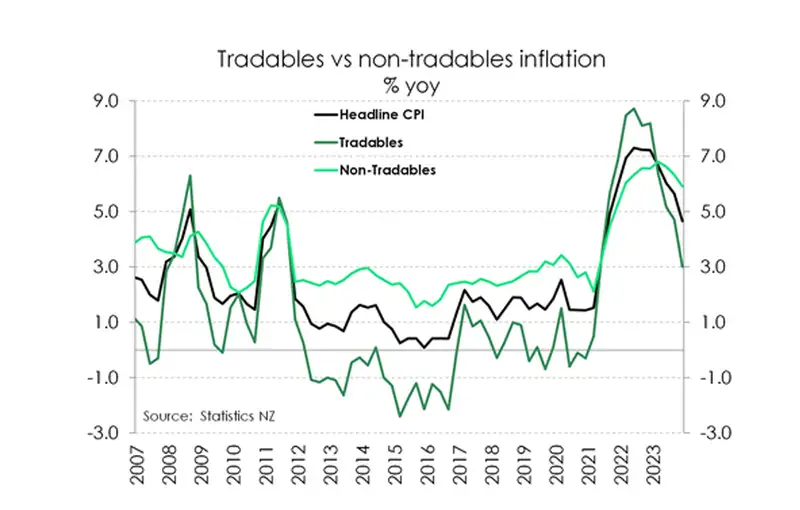

Scratching beneath the surface, the details were even less exciting. Imported inflation, sitting at 3%, continues to do most of the leg work in bringing down the headline number. But that’s not really what the RBNZ cares about. They want to see a significant deceleration in domestic inflation. And with non-tradable inflation remaining elevated at 5.9%, that’ll do little to appease the RBNZ.

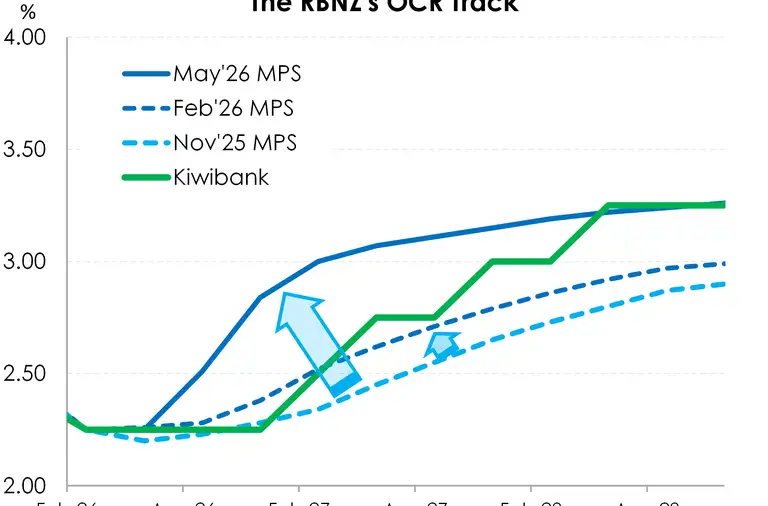

In saying that, the fall in the headline number is warmly welcomed. Inflation is running well below the RBNZ’s forecasts. But we are still a ways away from our central bank pivoting. The RBNZ have made clear their need to see stable inflation in their rear view mirror, not their projections. In November, the RBNZ noted they want to see inflation back at 2% before cutting. We think they’ll cut before then. But that’s the vibe.

Inflation continues to decelerate in a way we largely expected

Inflation continues to decelerate in a way we largely expected. The deceleration in prices is a tradables story. And the stickiness in domestic prices is a migration boom and housing story. Over the quarter, prices rose 0.5% with the annual rate falling to 4.7% from 5.6%. The numbers were pretty much bang in line with our forecasts and what the markets had expected. The RBNZ on the other hand, had forecasted a 0.8% rise over the quarter and an annual headline rate of 5%. To be fair, their forecasts were finalised in November, and most of the data since then has come in (much) weaker than they expected. So it’s good news to the RBNZ. Especially since the core measures, which strips out the stuff we don’t like, fell further from 5.2% to 4.1%. As well as prices for about one third of all items in the CPI basket decreasing over the quarter.

Though that’s probably where the celebrations end and our more critical analysis kicks in. Because the falls in inflation are still coming from imported components, rather than domestic components. Tradable inflation, now at 3%, is sitting within the top range of the RBNZ’s target band. Again, good news. But the RBNZ has most it’s influence over domestic inflation which is still sitting well above their band at 5.9%!

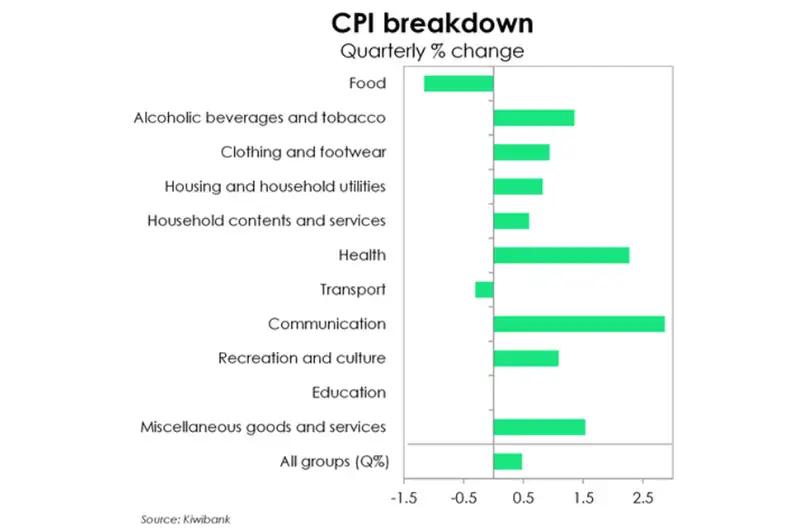

The number one theme arising from the stickiness of domestic inflation comes from our surging migration and understocked housing market. Despite the biggest price change over the quarter coming from the communications group, it was the housing and household utilities group that had the largest contribution.

Over the December quarter alone:

- rents lifted 1.1%,

- while construction was up 0.7%, and

- the housing energy group lifted a strong 1.9%.

An influx in migrants is great for relieving wage pressure and some pressure in services inflation (which mind you still sits elevated at 4.7%). But migrants also add demand pressure through a number of channels – rents being most obvious.

That said, todays report is still a move in the right direction. And we remain on track in seeing inflation back within the RBNZ’s 1-3% target band. And today’s report should still be sufficient to see the RBNZ pivot away from rate hikes. A prolonged on-hold stance has been the global norm. But 2024 should be the year central banks deliver rate cuts.

Falls within the CPI basket

We’re starting to see falls in a number of items and groups within the CPI basket. About one third of items in the basket recorded price declines over the December quarter, and that the most in over three years.

Food prices recorded the largest declines, down 1.2% over the quarter, thanks to a 6.4% fall in the price of fruit and vegetables. There’s been some seasonal softness across fresh produce. Over the year however, food prices remain elevated, up 5.7%. But that’s down from 10.7% a year ago, and the smallest annual increase since the March 2022 quarter. It appears food inflation has (finally) peaked. Adverse weather conditions early in 2023 resulted in double digit increases in prices for food, especially fresh produce. But prices appear to be well and truly normalising.

Similarly, declines were seen in the transport group, down 0.3%. Thanks to both a 2% decline in prices for vehicle purchases as well as softness in petrol and air fares. Over the December quarter petrol prices remained flat while airfares also continued to correct. Helped by growing airline capacity, international airfares rose just 2.5% over the quarter, while domestic airfares declined 7.5%. That’s an atypical move. Airfares usually spike over the December quarter given it is the holiday period.

Of all groups, it was the communications group, up 2.9%, that posted the largest quarterly rise. It was due to a surprising 16% lift in telecommunication equipment, which was attributed to a rise across cellphone and TV’s. But our focus was more on the housing and household utilities group.

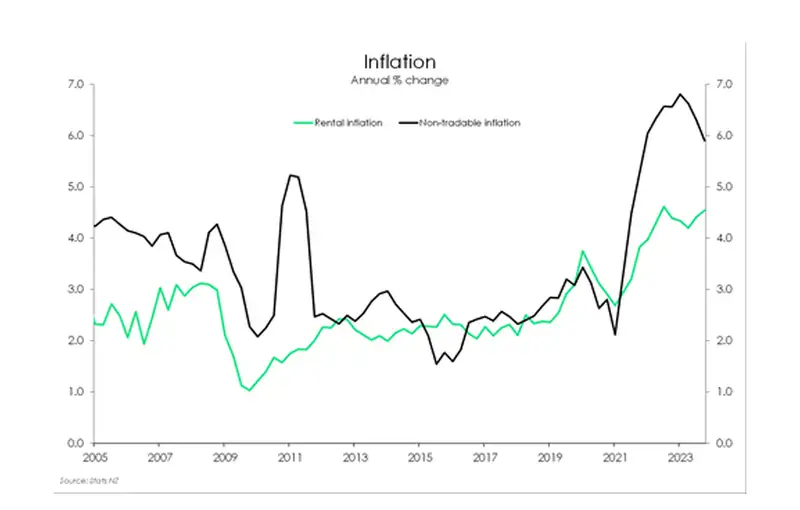

Following a 0.8% lift over the quarter, housing inflation was up 4.8% over the year. It’s the ripple effects of migration and poor housing stock. The surge in migration continues to drive rents, which are up 1.1% over the quarter. Over 2023, rental inflation has crept up to 4.5% - high above the circa 3% pre-covid rates. Meanwhile, we also saw a slowing in the rise of construction costs. Rising just 0.7% over the quarter, construction costs over the year are now down to 3.6%, from last quarter’s 5%yoy figure. A continued slowdown in home construction costs will likely provide some offset. Cost pressures remain strong, but are easing.

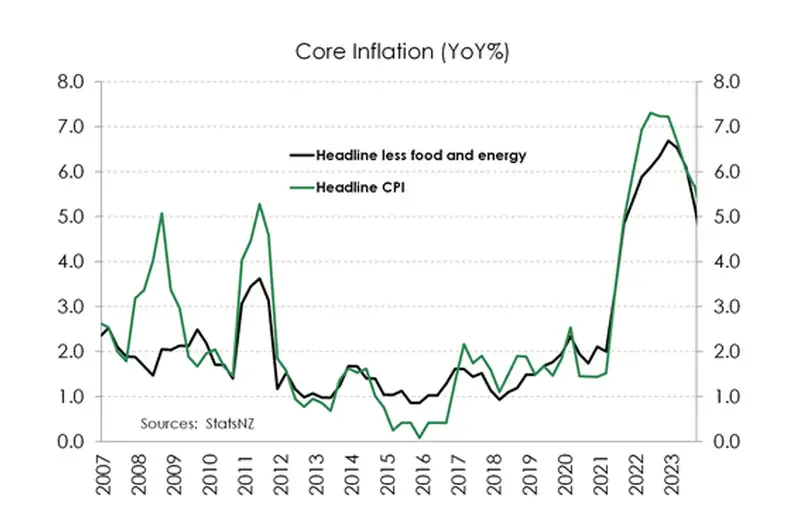

Core continues to cool

Encouragingly, core disinflation continues. Core measures of inflation – stripping out the volatile food and energy prices – have dropped from 5.2% in September to 4.1% now.

Although still an elevated rate, 4% is far better than the 6.7% peak in December 2022. Trimmed-mean measures of inflation (excluding extreme price movements) also eased to around 5% from 5.6% in September.

Overall, an easing in both of these data points shows a softening in the underlying inflation trend. Inflation is well past its peak and is falling at considerable pace.

Domestic inflation is still too strong

The RBNZ won’t be too cheery about non-tradable inflation coming in stronger than expected. Domestic inflation eased to 5.9% from 6.3%, against the RBNZ’s forecast of 5.7%. It’s not a huge miss, but a miss in the wrong direction. The ripple effects of migration is adding upside pressure, especially when it comes to housing. Solid lifts in rents and insurance remain the leading drivers. Although, when we exclude housing, domestic inflation looks to have turned a corner – falling from 7.3%yoy to 6.9%. That’s a small win. Overall, it’s encouraging to see the annual domestic inflation rate fall below 6% for the first time in late 2021. However, more progress is needed for the RBNZ to be comfortable that inflation is returning to 2%.

Tradable (imported) inflation was much softer than expected. Over the year, imported inflation has fallen from 4.7% to 3%, and further away from the dizzying heights of 8-9%. Weakening imported inflation continues to do most of the leg work in bringing down the headline rate. That’s great. But momentum can be easily disrupted. We’re keeping an eye on the what’s happening abroad. Houthis attacks on ships in the Red Sear are causing shipping rates to spike, and delivery times to lengthen. We are unlikely to see the same sort of spike cause by the covid crisis. But any spike in costs is unwelcome.

In a holding pattern, for now

Today’s CPI print was of great importance. The inflation numbers feed into the RBNZ’s February decision as well as the upcoming survey of inflation expectations. Since hitting the 7.3% peak in June 2022, inflation has been steadily decelerating. We’ve seen the headline rate fall from the 7s into the 6s, 5s and now, into the 4% range – that’s a big shift in mindset. Psychologically, we now have 4% in the back of our minds when it comes to setting prices. That's a big shift from 7%. Today’s move to 4.7% should reinforce the downward momentum in expectations. And given the self-reinforcing nature of inflation expectations, should drive further falls in inflation. We are winning the (psychological) war on inflation.

Today’s print showed that inflation continues to move in the right direction. And despite some hurdles ahead (including a red sea induced spike in shipping costs, and a migrant fuelled rise in rents etc.) we see inflation continuing to ease back towards 2%. We’re on track for inflation hitting the top end of the RBNZ’s target 1-3% target band by the second half of this year. Which means rate cuts are not too far away. Despite the RBNZ ending 2023 with a very hawkish message, and signalling another rate hike, today’s report should see a softening in the RBNZ’s tone in February. And we should get some good insights from Paul Conway's speech next Tuesday. As the RBNZ's Chief Economist, Paul needs to address the significant downside surprise in economic activity, with a very weak the GDP report, as well as today's inflation data. In fact, much of the other data to date have also been weak, and we expect the same going forward. The current state of play and the outlook should be sufficient to see the RBNZ pivot away from rate hikes. A prolonged on-hold stance has been the global norm. But 2024 should be the year central banks deliver rate cuts.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.