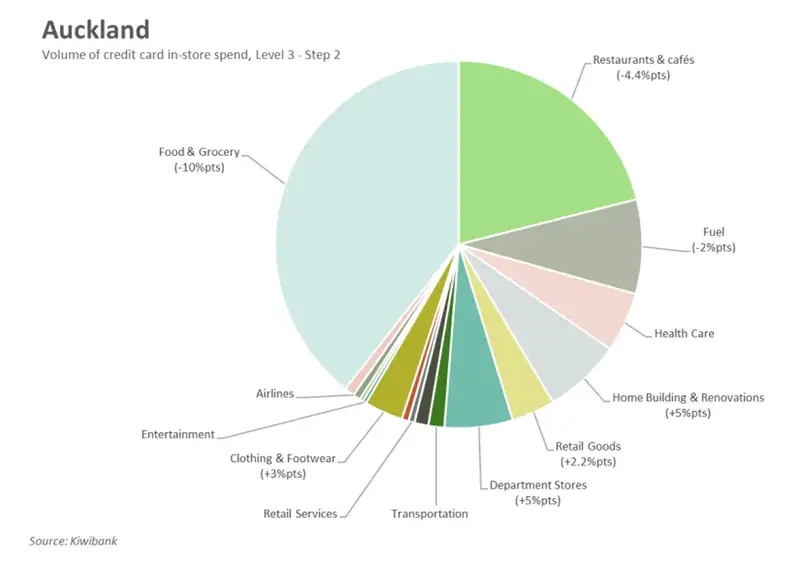

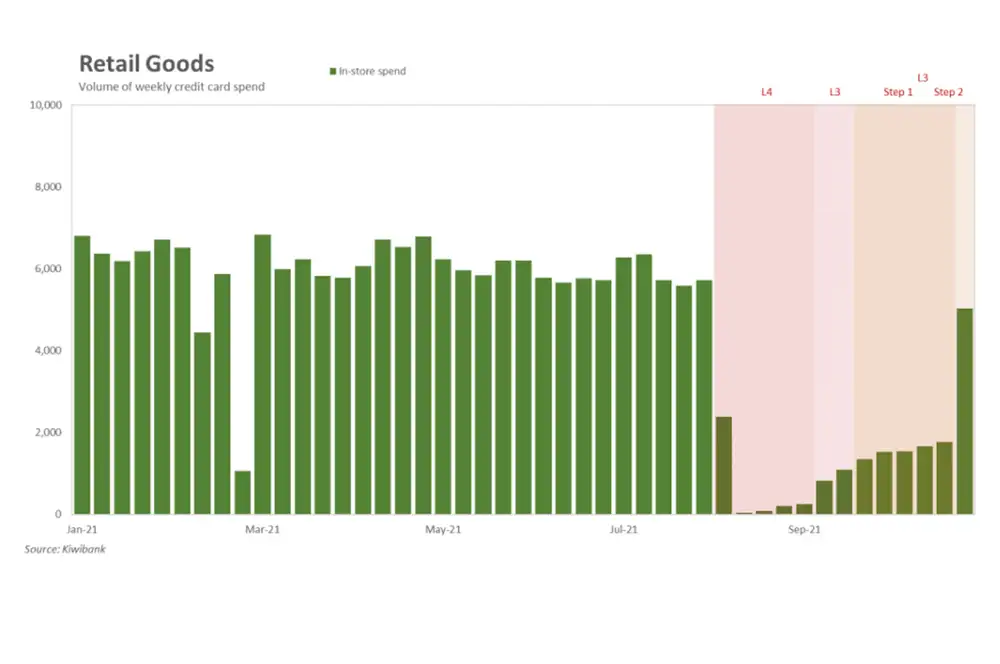

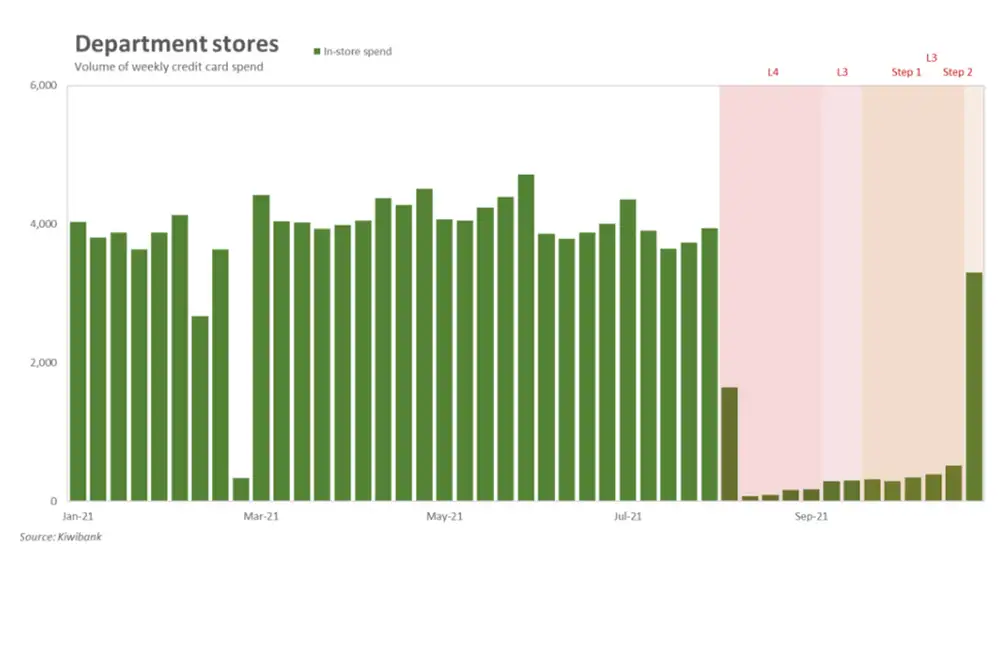

Department Stores were the big winners from the change, with the number of transactions rising 8-fold. Overall, retail goods have taken a bigger slice of the consumer spending pie.

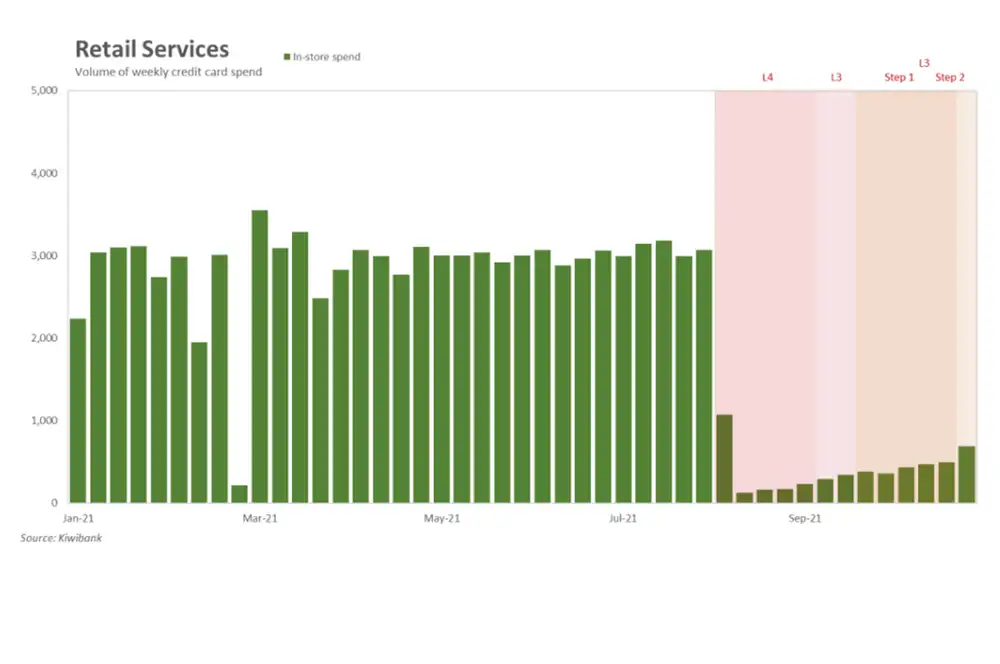

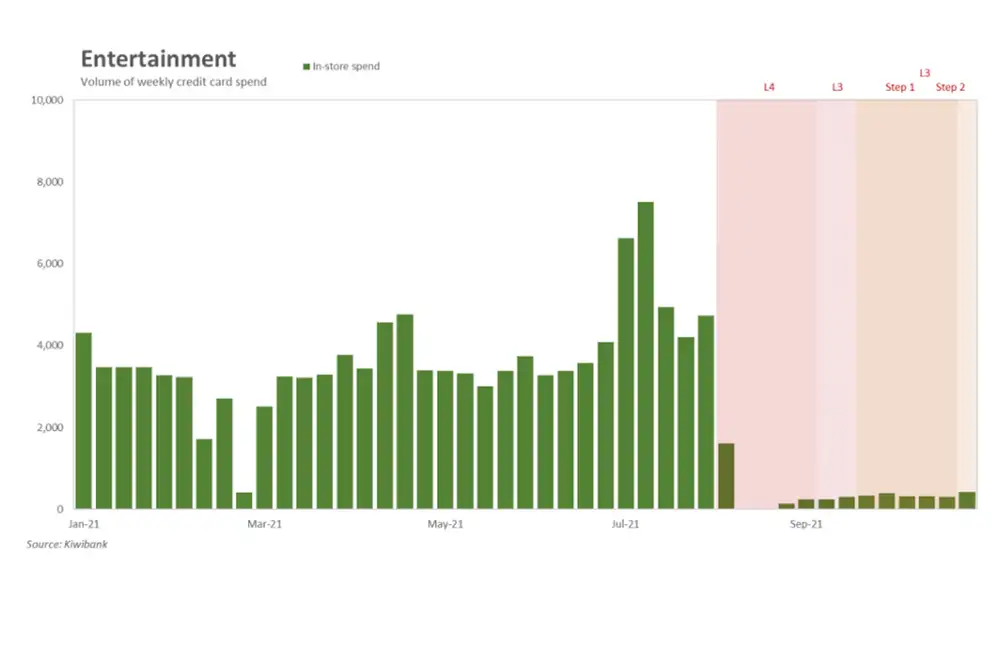

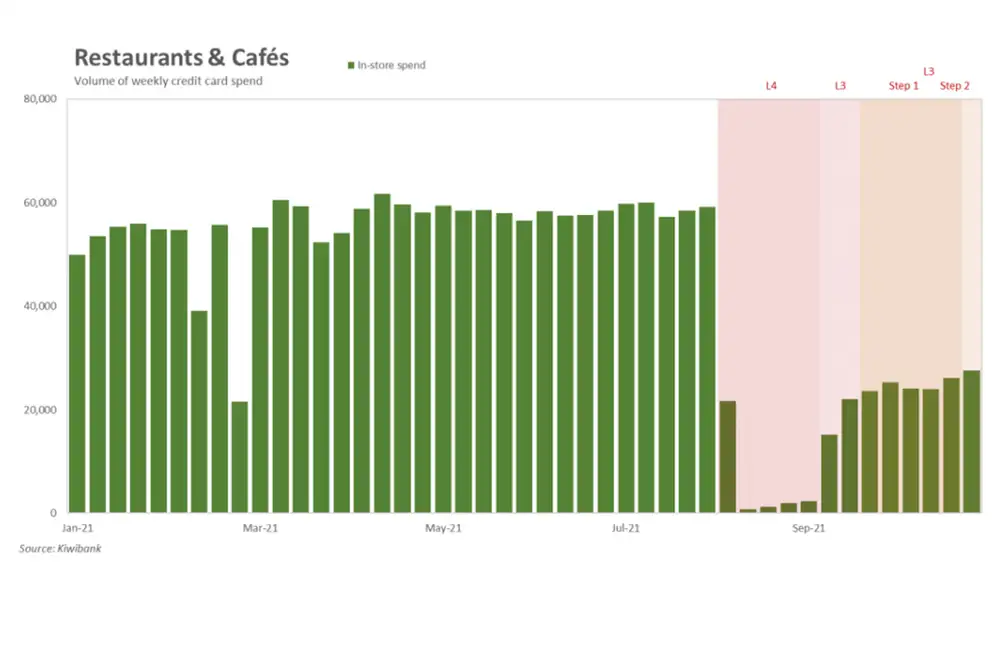

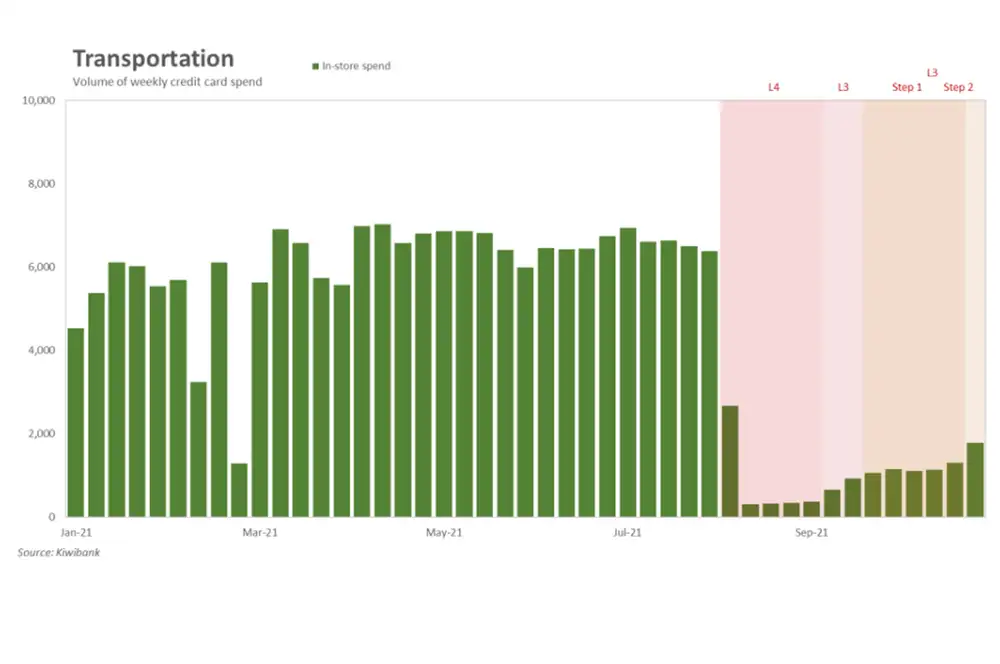

Retail services however are still struggling. The doors among hairdressers, gyms and cinemas remain locked, with close-contact service still off the cards. More lenient restrictions are required to see a revival in retail services spend.

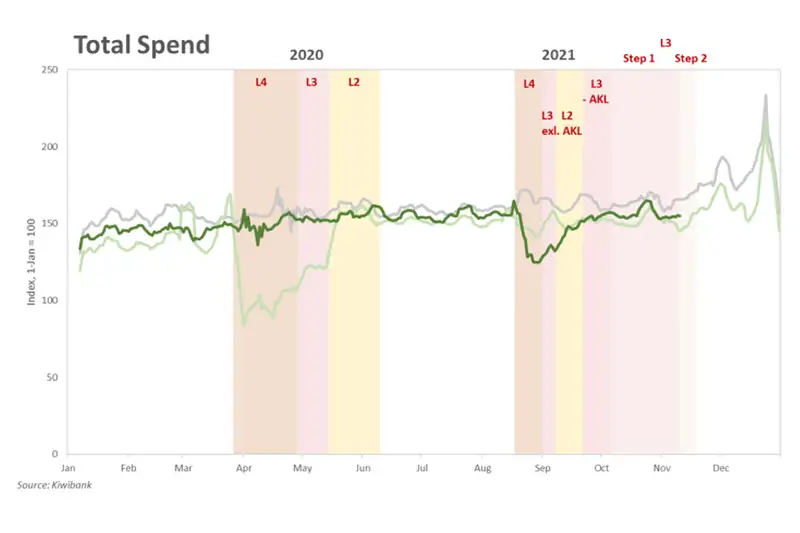

The anticipated shift into the Covid-19 traffic light system should help the recovery in services, especially. And overall spend should take another leg higher once Auckland’s drawbridge is let down. Mark your calendars – December 15 is D-day.

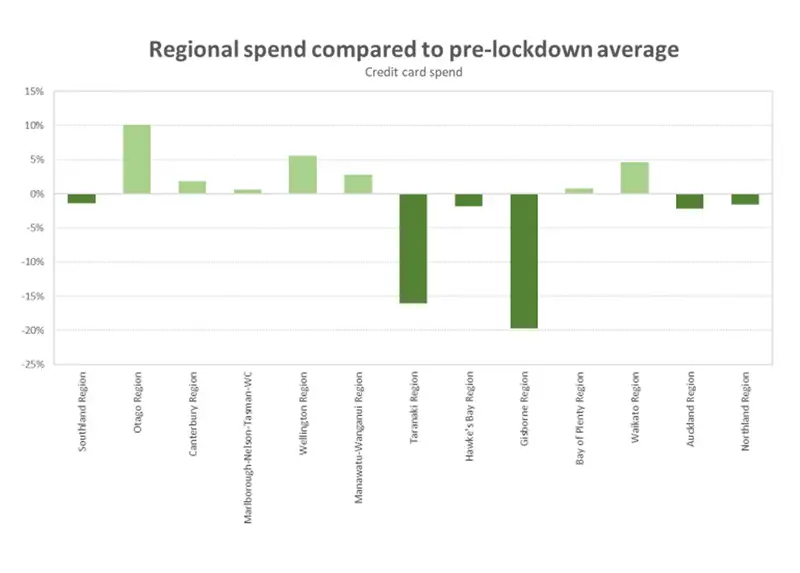

At the regional level, the picture is still mixed

Outside of Auckland, the Waikato and Northland, most regions are enjoying the freedoms of Level 2 and spend has lifted to above pre-Delta lockdown levels.

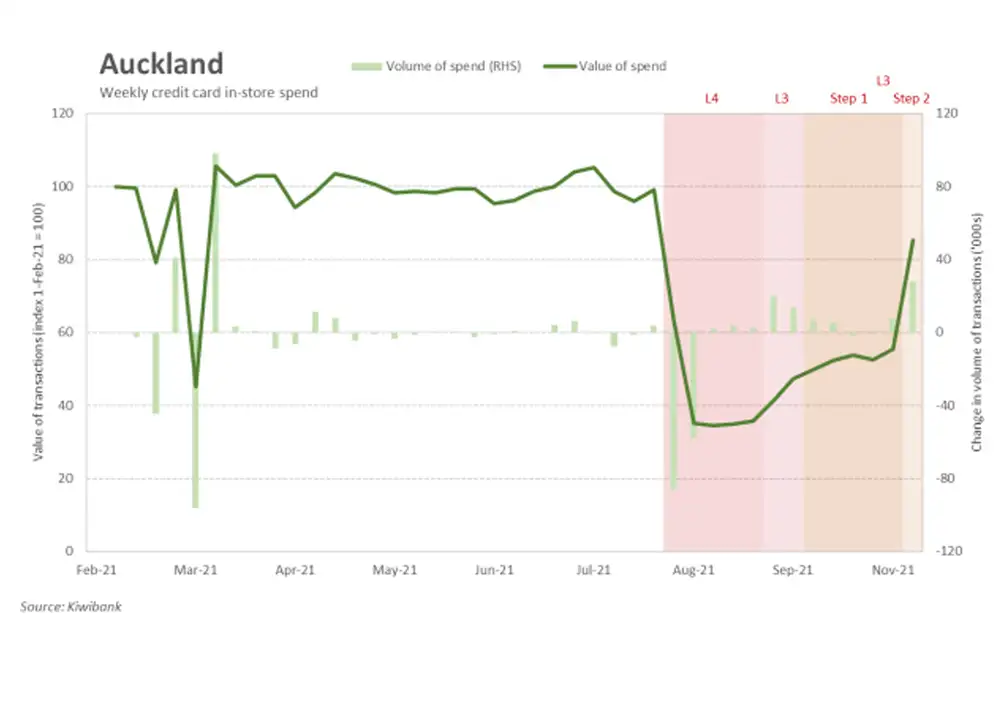

Spend in Auckland is still down 2.2% as restrictions have dragged on. However, the move to Level 3, Step 2 has allowed more activity to take place. And down 2.2% is a considerable improvement from being down 14% while at Level 3, Step 1.

Northland and parts of the Waikato have also both experienced a tightening in restrictions. Spend in Northland is down 1.5%, however spend has increased to above pre-Delta lockdown levels in the Waikato region.

Back in action

In -store consumer spending in Auckland was jolted back into action once the region stepped down into Alert Level 3, Step 2. After three months, the malls are open for business, but still with restrictions in place. Masked shoppers are keeping their distance and the smell of sanitizer permeates the air. The loosened restrictions have seen an immediate increase in in -store spending. Within Auckland, the number of credit card transactions rose 35% over the first five days at Step 2, with the value of spend rising 62%. And as expected, Department Stores were the big winners from the change. The doors among retail services however remain locked, with close -contact service still off the cards.

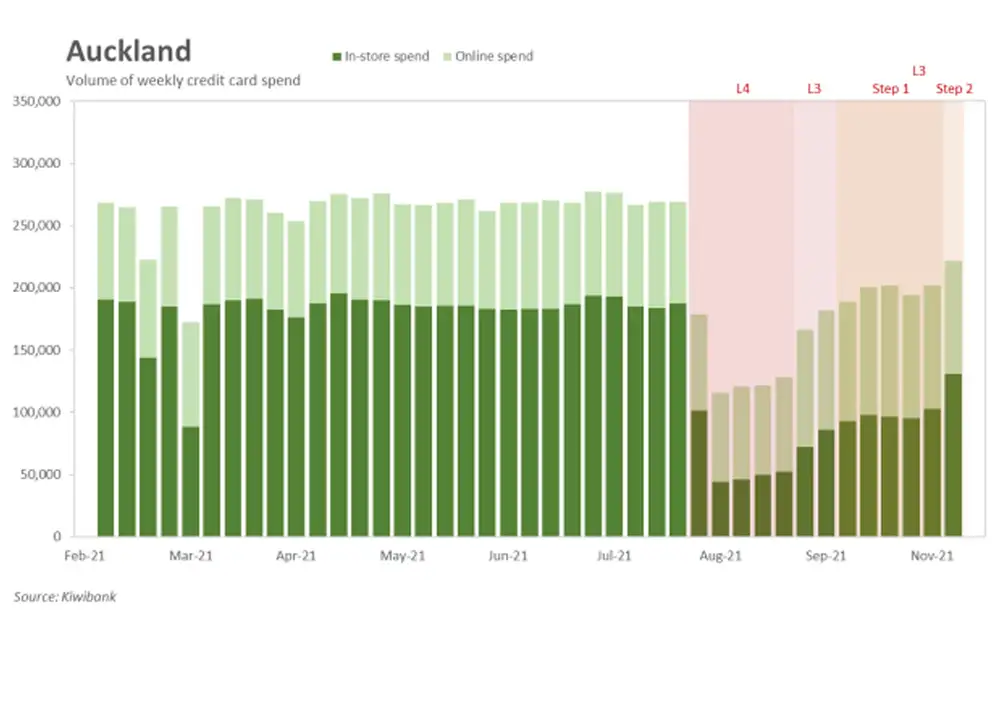

The rise in in -store spend however was slightly offset by a drop in online spending (10% drop in both vol and val). For some respite from endlessly staring at screens, shoppers have taken their shopping to the streets. In aggregate, the value of total credit card spend in Auckland is up 14%.

With Delta continuing to spread within the community, some may still be feeling anxious to step outside. Physical shopping may also be less attractive given our strengthened familiarity with ecommerce. Throughout lockdown, online spending surged, and is the main reason why the drop in overall spend was much shallower. However, it’s still early days. And footfall will likely increase over the coming months, especially with Christmas fast approaching. The sparkle of tinsel, sound of Sinatra and photo op with (a masked) Santa may entice more to shop in person.

A bigger slice of pie

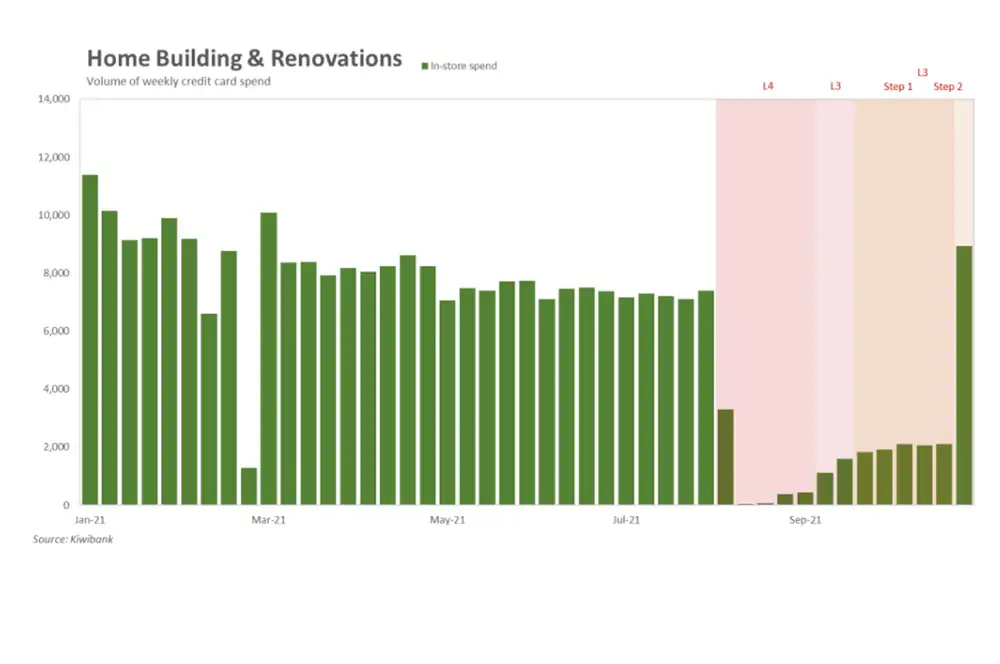

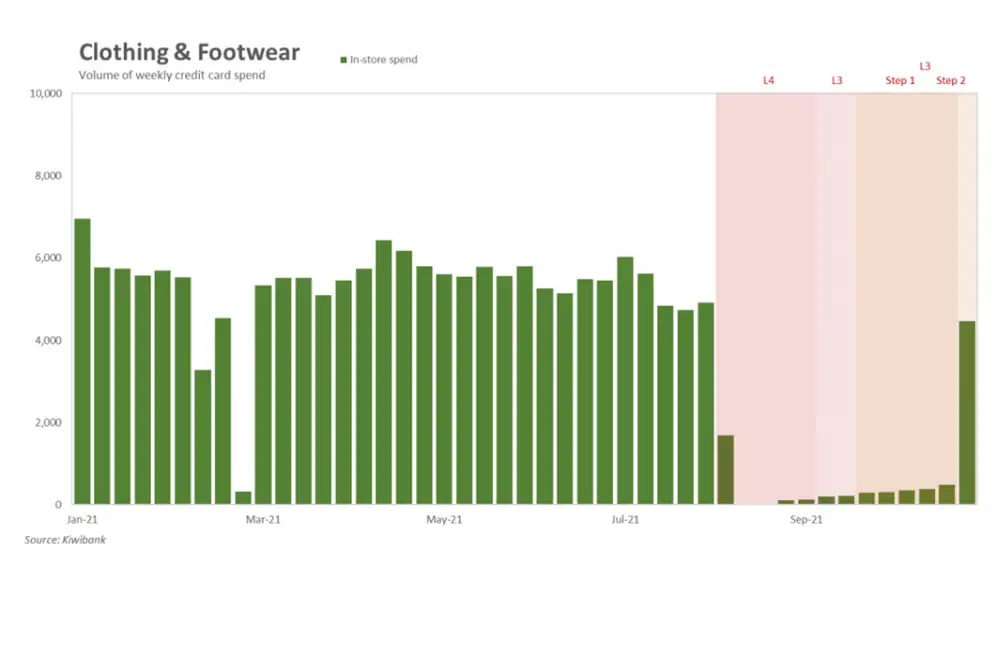

As expected, Department Stores were the biggest winners from the change in restrictions. The number of credit card transactions made in -store rose 8 -fold, with value rising by a similar magnitude. The dramatic rise in transactions is a consequence of spend flatlining throughout the lockdown period. Spending inside Clothing and Footwear stores also spiked, with those holding off their purchasing until the doors opened, preferring to try before they buy. Step 2 also saw another leg -up in home improvement spend. Springtime means more garden time. Mitre 10 reports potting mix has been the most popular purchase. Click and collect saw a lift in home reno and hardware spend, but not having to wait bumper to bumper is drawing more to visit the store. Overall, retail goods have taken a bigger slice of the consumer spending pie.

Retail services however are still struggling. For 90 days now, hairdressers have been out of action, cinemas empty, and wait staff waiting on no -one. Transport -related spend too is yet to return to pre -Delta levels. With many still working from home and the Auckland border still in place, there’s little need and ability to travel. Retail services requires more lenient restrictions to see a revival in spend.

Big winners – Auckland spend

Still struggling – Auckland spend

A mixed picture

At the regional level, the picture is still mixed. Outside of Auckland, the Waikato and Northland, most regions are enjoying the freedoms of Level 2. Spend in most regions has lifted to above pre -Delta lockdown levels.

Spend in Auckland is still down 2.2% as restrictions have dragged on. However, the move to Level 3, Step 2 has allowed more activity to take place. And down 2.2% is a significant improvement from being down 14% while at Level 3, Step 1.

In early November, Northland moved to Alert Level 3 as Delta cases spread up north. The recent move back to Level 2 should see a rebound in spend in the coming weeks.

Impressively, spend in the Waikato region is above pre - lockdown levels despite parts of the region experiencing the same restrictions as Auckland.

Covid’s calling the shots

Greater spend in Auckland and continued spend elsewhere has seen a lift in overall spend. Total Kiwibank credit and debit card spend rose 8% since Auckland’s move to Step 2. Spend on goods has increased 10%. But given depressed spend on services in the largest city, total services spend is also yet to return to pre -Delta lockdown levels, down 13%.

The anticipated shift into the Covid -19 traffic light system should help the recovery in services, especially. Sometime after November 29, Auckland is expected to move into the Red setting. Hairdressers and gyms can open their doors, dine -in service may resume and events may occur, however with limitations on people gatherings and provided vaccination certificates are used. Most other regions are expected to move into the less restrictive Orange setting.

Overall spend also should take another leg higher once Auckland’s drawbridge is let down. Mark your calendars – December 15 is D -day. After being cooped up for 90 days, Aucklanders are itching to drive/sail/fly past the border. Fair warning to neighbouring regions, prepare for some excited Aucklanders.

After a sharp drop in Q3 GDP, we’ve pencilled in a rebound of around 8.5% in Q4. However, with Auckland spending all of October in some form of lockdown, there’s growing downside risk to our forecast. While our spending data and several leading indicators suggest that underlying demand is solid, Covid is still calling the shots for the economy, near -term. So long as lockdowns are part of the playbook, large swings in economic activity are to be expected.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.