- The Kiwi economy has (under) performed largely in line with our forecasts. And the RBNZ has kicked off. We expected the Kiwi to be closer to 57c, given the data released. But it’s not even close, at 62c. The USD has weakened, falling about 4.5% in two months. It’s hard for the Kiwi to fall against a falling dollar.

- The RBNZ has been leapfrogged by the Fed. Although the RBNZ started cutting a little earlier, the Fed has cut by a little more. The Fed kicked off their cutting cycle with a bold and beautiful 50bps move. And they’ve outdone the RBNZ.

- We think 50bp moves will be on the table when the RBNZ deliberates in October and November. We’d need to see at least one 50bp move to match market pricing and see a fall in the Kiwi. We still forecast relative underperformance in the Kiwi economy, eventually leading to a lower currency. But we’ve recalibrated our call to 59c from 57c.

We came into 2024 forecasting a weakness in Kiwi, a deterioration, a downward glidepath. Our call was 57c by year end. Because we expected the economy to remain in recession for most of the year. And here we are. The economy remains in recession, the unemployment rate is rising in line with forecast, and the RBNZ has started cutting sooner than initially expected. Looking at the developments in the data, and the RBNZ’s response, we’d expect the Kiwi to be closer to 57c. But it’s not even close.

At 62c, the Kiwi dollar has outperformed. Because the dollar, in Kiwi / Dollar, has fallen. The US dollar has fallen 4.5% in the last two months, helped along by a dovish Fed and their 50bp kickstart to cutting.

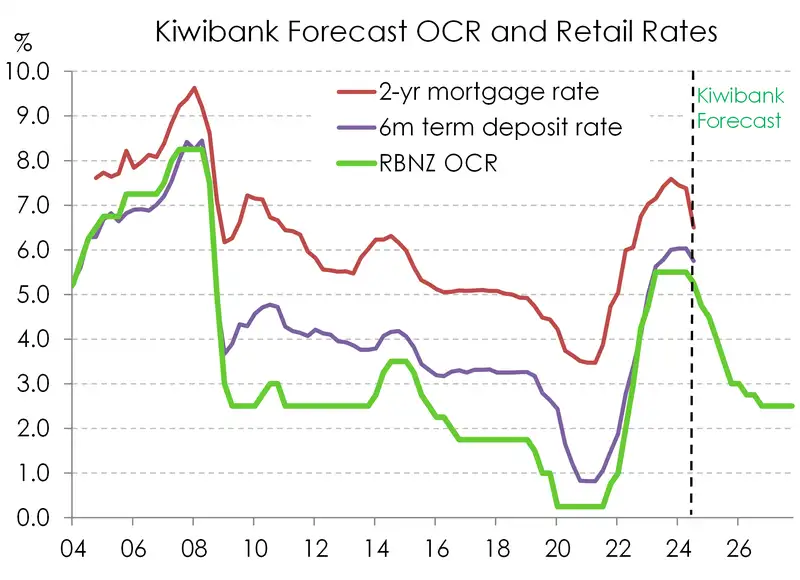

It’s worth noting that the US economy has outperformed the Kiwi economy. And with these cuts, the US economy will continue to outperform. So, the question amongst traders and strategists is: if the Fed sees the need to cut 50bps with a stronger economy, will the RBNZ do the same? Yes, they should. Both central banks are aiming to get their cash rates below 4%, quick, and looking towards a neutral rate of 2.5-to-3%. In our opinion, the RBNZ are responding – late, but in earnest. A rate cut in October is as close to a done deal as you get. In fact, we’d argue the only discussion should be on delivering 25 or 50. We’d advocate 50. And again, 50 in November. The RBNZ’s first 25bp cut in August marked the start of a move towards 2.5%. That’s 300bps. We argue the RBNZ needs to get the cash rate below 4%, asap. It takes up to 18 months for rate cuts to filter through the economy. We all love fixed rates. And fixed rates need time to roll off. Effectively, the RBNZ are cutting today for an economy at the end of 2025, the start of 2026. Get moving… and get the Kiwi lower.

Trading view, what’s next?

In our previous FX Tactical we argued that we saw the Kiwi dollar heading lower, likely into the 0.5700 level. This time we are making some tweaks to that view, given the Kiwi’s apparent reluctance to trade down to these levels. Our view is that Kiwi should arguably be lower, but we are not too proud to admit that the 0.5700 level is now looking less likely, and so we tweak our expectations as the facts change. Our view is that 0.5900 is probably the more reasonable level at this juncture. We have had both the RBNZ and the Federal Reserve officially kick off their monetary policy easing cycle, and now we are focusing on the magnitude of cuts going forward. The timing of said cuts is also a key point. With the RBNZ set to drop rates, we think the Kiwi should head lower. Also the fundamentals around our relative economic performance versus other G10 economies mean that we still think that the RBNZ will be forced to cut rates more aggressively than the Federal

Reserve, especially once we kick into 2025. For the next couple of months however, the challenge facing a significant move lower in the Kiwi will be current market pricing vs the timing and run of sufficient data to give the RBNZ enough confidence to necessarily deliver 75bp of cuts by year end. With circa 41bp of easing priced for October’s MPR and then a further 45bp for the November MPS (making a total of 86bp for an early Xmas present to borrowers), the timing of Q3 CPI between the October and November meetings may throw a spanner in the works of the RBNZ delivering this sort of priced outcome. Whilst we fundamentally believe the RBNZ should simply get on with cutting rates to the tune of 100bp by the years end (which would support a strong move lower in the currency), data timing may only result in a 25bp and then an insurance 50bp reduction over the extended RBNZ summer holiday.

Market expectations of 71bp of Fed easing by Xmas post “the catch-up” 50bp cut last week does have some risk of tapering back towards 50bp with the Fed’s updated dot plot indicating a remaining 2 x 25bp cuts for 2024 and then a further 4 x 25bp throughout 2025. 2024 has certainly proven to be somewhat of a challenge in believing central bank forecasts (particularly of the RBNZ), but if we do take both the Fed’s Dot Plot and RBNZ’s OCR track as some sort of guidance for the glide path towards a neutral rate through 2026, we believe current economic conditions (i.e. the US needing a pacemaker, whilst NZ needing the defibrillator) means ultimately the RBNZ will either have to cut faster or possibly even deeper than the Fed. So for now, whilst there is a good possibility for the Kiwi to keep trading close to current levels around 0.6200, further out into 2025 conditions still look very challenging for the Kiwi to find any oxygen above 65c. Shorter term, looking at the technical charts, we think the Kiwi is likely capped at 0.6300 for now, but needs a definitive break below 0.6080 before it tracks lower back towards the 0.5900 – 0.6000 region.

For the NZD/AUD cross we have a similar view. The interest rate differentials should see the cross trade lower. The RBA are comfortable to hold rates at their current restrictive levels for now, as they wait to see inflation put to bed. Their economy is also in a much better position than ours, with the Aussie labour market remaining resilient. Once the cross breaks through the 0.9100 support level it opens up the 0.8900 level, which is where we see the cross belongs in the current rate environment – Mieneke Perniskie (Trader) & Hamish Wilkinson (Senior Dealer) – Financial Markets

Markets, Mystics & Mayhem podcast

Episode 2 of the Markets, Mystics & Mayhem podcast presented by the Kiwibank Economics team, features Mieneke Perniskie as a special guest. Mieneke talks through about what she does as an FX trader, and why we’re all scratching our heads at the Kiwi dollar.

Jarrod Kerr and Mary Jo Vergara from the Economics team also discuss recent migration flows. A surge in migration over 2023 has led to a rapid increase in population. The boost to labour supply was embraced with open arms. But the stress placed on the rental market is exposing our failure to invest in infrastructure – a decades long issue.

You can stream the podcast on Spotify, or watch the episodes over on the Kiwibank YouTube channel.

Modal to play video

The recession continues… with a triple trough

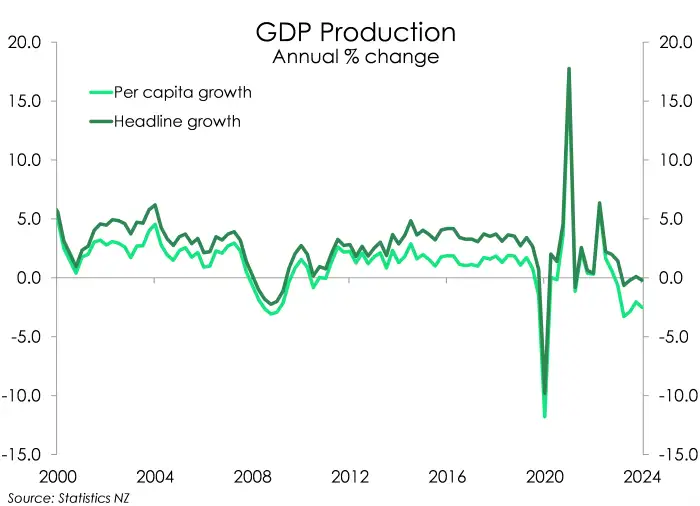

On a per capita basis, the economy has been in recession for two years. Activity per head is down 4.6% from September 2022 – far worse than the cumulative 4.2% decline during the GFC. There is light at the end of the tunnel, and it’s burning brighter. We think the RBNZ’s decision to cut the cash rate in August, marks the turning point in this cycle.

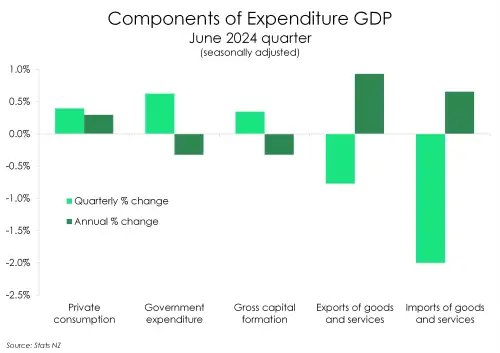

Scratching beneath the surface of the Kiwi data, there is some bad news. Dairy exports are down, with the primary sector underperforming, and spending throughout the economy remains soft, super soft. The large contraction in imports highlighted the softness of local demand. If we’re not buying stuff, we’re not importing stuff.

Household consumption remains weak. Spending on durable goods declined a chunky 3.4% over the last quarter. And compared to last year, durable spend is down almost 10%! Households are reining in their big-ticket spending as tight financial conditions weigh on wallets.

Beyond households, business investment picking up, slowly. Investment in plant and machinery lifted almost 2%. Similarly, the downtrend in building consents has seen a 5.8% decline in residential buildings compared to a year ago.

Household spending, government spending and business investment were all up over the last quarter. But the gains made across these three components were offset by the 0.8% decline in exports. And leading the decline was the 4.4% fall in goods exports. The 1.4% decline in agri production was mirrored by falls in exports of dairy and forestry products.

See our latest economic overview.

Kiwi crosses in the months ahead

NZDUSD (5-year daily)

The triangle breaks: significantly for longer term downside risk, as the Fed prepared the market for last week’s 50bp rate cut decision. Last quarter saw NZDUSD break out of its multi-year converging triangle picture. Whilst arguably the technical picture now looks a little more positive than back in June, we believe the economic fundamentals do not support a sustained rally to the upside. A key upside level exists: back at last December’s 0.6360 high and from there 0.65 cents. Should these levels break then the driver would ultimately need to be a dramatic change in expected interest rate paths in both NZ and the US. For now, for the underlying belief that risk still lies with the RBNZ needing to do greater or faster easing than that the Fed, NZDUSD can trade back into the 0.5900 / 0.6000 zone once more. The turnaround in domestic economic activity won’t be an overnight story, and until evidence arrives of the potential for any form of positive NZD carry, the Kiwi continues to remain within recent ranges.

NZDAUD (5-year daily)

Last quarter witnessed the breach of what we thought would be a key 0.9030 – 0.9050 support zone as the RBNZ flipped on its policy stance. A move to 0.8960 evolved and further downside looked likely. But “the Cross” is hard. Once again, it is defying any form of fundamental logic of relative economic performance and expected interest rate paths of both NZ and Australia. NZDAUD has instead reversed paths to rally back into a familiar resistance zone between 0.92 and 0.93 cents. Last quarter, we called a “retest of levels below 90 cents” and for AUD buyers to be active for rallies into 0.9250/0.9330…so, we will take that! But we still feel there is more downside to eventuate, especially if our view of sustained RBNZ easing comes during a period of relative inaction from the RBA. Should NZDAUD squeeze through near-term support around 91 cents, then retest of the 2024 low becomes the next big target.

NZDEUR (5-year daily)

Confirmation from the ECB that its easing cycle looks likely to be a gradual approach saw limited impact on the EUR. Other central banks, including the RBNZ, are playing catch-up and markets have priced aggressive easing in both the US and NZ. This combination of factors saw NZDEUR last quarter reject the strong intersection of long-term channel and multi-month resistance (circa 0.5750) and resume further weakness into a new post-covid low of 0.5363 – a risk we highlighted in our previous FX tactical update. From this point, the development of expected Fed easing flowed through to ECB easing expectations with an average of 20bp rate cuts priced across 8 meetings over the coming year – seeing NZDEUR recover back into its former channel resistance zone. Given the ECB’s continued tentative approach (i.e. not 25bp at each meeting date), and our expected need for the RBNZ to deliver more, we expect to see NZDEUR resume a move lower once again to ultimately retest the multi-year low once more.

NZDGBP (10-year daily)

Why history matters. Last quarter, saw NZDGBP touch on a post 2016-Brexit low of 0.4653. Putting interest rate differentials aside, the longer-term picture continues to argue for NZDGBP weakness. The pair continues to make lower-lows within its current downtrend channel since the middle of 2022. The new (UK) labour government is starting to find its feet with left leaning policy arguably leading to inflationary outcomes over time. Last month saw investors take stock of the potential risk of the BOE adjusting policy at a slower rate. Because UK inflation rate popped from 2% to 2.2% in July and held there in August also. Similar to our argument for NZDEUR, we remain wary of further downside risk in NZDGBP. Key resistance is examined at 0.4770. But a move below 0.4653 and perhaps into 0.4550 is our preferred course of direction should the RBNZ get moving in 50b clips before Xmas.

NZDJPY (5-year daily)

Well, we told you it would happen at some point – and it finally did! The multi-punch combo of a further 15bp BOJ rate hike (taking its policy rate to 0.25%), the RBNZ’s dovish pivot in the July MPR, and the manic Monday August selloff, saw carry trade investors scramble for cover big time. Across a 30-day run from early July into early August, NZDJPY witnessed an near-16% decline at one point – falling from a high of 99.02 to 83.07. From there, a full 50% retracement back into the previous multi-year channel support zone evolved as NZDJPY looked for some form of stable footing. How about that for volatility! From this point, upside resistance will be tested back into both the former channel support zone and 61.8% Fibo at 92.93. However, as per our broader downside Kiwi view, we think NZDJPY still has room to run lower as interest rate differentials continue to narrow over time. The ultimate test in NZDJPY will be around the 80.50 mark.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.