Our forecast terminal cash rate of 5.5% remains the same as it always has been. Although The RBNZ is still signalling a 40% chance of a hike. It’s increasingly unlikely to be delivered. And we instead are calling for rate cuts in November.

The timing of rate cuts is one thing, magnitude is another. And we think the RBNZ has more cuts up its sleeve compared to its peers. A lack of meaningful interest rate carry vs its major peers and weak local economy point to downside for the Kiwi dollar.

Rate cuts on the horizon

After many months of fast and furious rate hikes, the next chapter of monetary policy is upon us: rate cuts. But the question is, who will be the first to turn the page? The answer will have big implications for currency markets.

Arguably, the European Central Bank (ECB) and the Bank of England (BoE) have the strongest grounds to be the first to lower rates.

- Inflation in the Euro area has fallen to 2.8%, from the 10.6% peak and inching closer to the 2% target.

- In the UK, inflation is running at 3.4%. At the same time, economic activity has stagnated.

But it's a different story across the pond

US inflation has fallen from the 9.1% peak, but has been bouncing along the 3% mark since June last year. The so-called final mile back to 2% is shaping up to be a long and bumpy one. All the while, the US economy and labour market are holding up well. Such resilience buys the Fed time to lower interest rates.

Most in the market follow the Fed, and reflect back to their local central bank. And many central banks, the RBNZ included, will want the Fed to act as an icebreaker. It’s more likely that the Fed will cut mid-year followed by the ECB and BoE in quick succession. The Aussies were late to the rate hiking party but could beat us (RBNZ) to rate cuts. While the RBNZ was among the first to start hiking rates, it’s likely they’ll be among the last to cut.

Kiwi inflation continues to moderate. We’ve gone from a peak of 7.3% to 4.7%. But that’s not enough for the RBNZ to commence the cutting cycle. More progress is needed. It’s not until the September quarter that we expect Kiwi inflation below 3%. But it’s not until mid-October that we see that in writing. So that leaves the November meeting as the earliest date to begin delivering rate cuts.

If the Fed leads, then the Kiwi currency should hold up against the Greenback – helping importers. It is only when the RBNZ comes into action, around four to six months later, that the Kiwi is likely to depreciate – helping exporters. Indeed, we see the Kiwi holding strong near-term before falling to 57c by year-end. We forecast a similar flight path for the Kiwi/Aussie (NZDAUD) cross. Interest rate differentials will widen in the near-term, supporting the cross, with the RBA cutting ahead of the RBNZ. But the cross will come under pressure once the RBNZ steps in.

Timing of rate cuts is one thing, magnitude is another

And it’s likely the RBNZ has more cuts up its sleeve compared to its peers. The RBNZ was aggressive on the way up (delivering 525bps of hikes), and they’ll be aggressive on the way down (potentially 300bps of cuts). It’s conceivable that the Kiwi cash rate will settle at a level below the policy rates of other central banks. The Fed’s latest dot plot projects a total of just 225bps of cuts to a median projection of 3% by 2026. If so, we see the Kiwi pushing down to 55c this time next year.

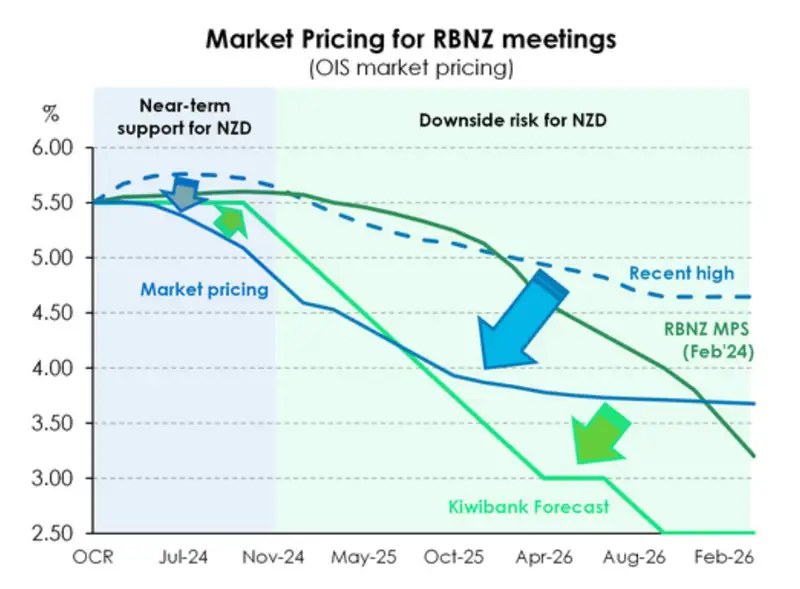

Barring a couple of short-lived spikes, the Kiwi has been losing steam since the beginning of the year. The Kiwi has gone from above 63c at the start of the year to 59.8c by the end of March. The Kiwi remains in a downtrend, but the unwind of market pricing may delay the eventual move to 57c. Kiwi rates markets are currently factoring in too much, too soon in the near-term, but not enough over the medium-term. If we look at the OIS (overnight index swap) curve, traders are placing some handsome bets on cuts as early as August (-24bps at 5.24%). There is 68bps of cuts priced by November (at 4.82%) which compares to our 25bps. Out to February next year, 91bps of cuts are expected which implies a cash rate of 4.59%. That’s well ahead of our optimistic estimate of two cuts to 5%, and the RBNZ’s path of unchanged (5.5%). Cuts are expected to continue over 2025, and into 2026. But the terminal rate around 3.8% in 2026 is well above our expected move to a neutral setting of 2.5-3%. It’s here we believe there is not enough priced in.

The chart above plots the RBNZ’s OCR track, our forecasts, and current market pricing. We, along with the market, are miles ahead of the RBNZ. That’s not unusual. Markets turn much faster than central banks. And market pricing has moved from sitting close to RBNZ estimates, to below our estimates near-term (blue arrow). We think the market is getting a little ahead of itself, near-term (blue shaded area). The cuts priced into July, and out to February, are likely to be pushed back. If we’re right, (paying) the 6-month to 1-year rates will grind higher, as the RBNZ under-delivers on over-priced cuts. For the Kiwi, downside risk is limited as rates remain at levels higher than hoped and for longer than hoped. We don’t believe a recalibration of rate expectations will send the Kiwi flying, but it may prevent it from sliding deeper than otherwise. Any short-term upside will be within current ranges capped at around 62.5-63c.

Further out, pricing becomes a little too light (green-shaded area). We forecast 25bp cuts in each meeting from November, until we get back towards neutral. From a trader’s point of view, that’s a front-end flattener. Pay 6-month to receive further out, maybe 3-year. And for the Kiwi, that points to downside in the medium-term. With the RBNZ likely cutting by more than expected, a 55c would be within sight.

If we’re right, big if, then the interest rate curve should move as follows. We forecast the pivotal 2-year swap rate to hold below 5% for the next quarter. And then we expect the 2-year to ease down to 4.0% by year-end. Over 2025, as the RBNZ cuts below 4%, the 2-year will fall towards 3.0%. So we could see a fall in interest rates of around 250bps. Such a move should see similar falls in mortgage and business lending rates, but also term deposit rates. Good news for many, bad news for some.

The lowering of interest rates will provide much needed relief for indebted households and businesses. And it is the expectation of these rate cuts that has us in the more “optimistic” camp when thinking about economic growth, household wellbeing, business expansion, and the recovery of the housing market.

Trading view, what’s next?

In previous editions of our FX Tactical, we continued to call for a lower Kiwi dollar. We maintain this view. The headwinds for the NZ economy are real, as we have seen in the last GDP prints. And finally, the Kiwi dollar is starting to take this on board. For the last few months, currencies have largely been driven by interest rate differentials, or more so the expectation of said differentials. Now it’s getting a little more nuanced, down to timing. For now, we definitely think that the Fed is going to cut rates well ahead of the RBNZ.

BUT… we think that the market is getting somewhat ahead of itself – as is always the case when it comes to the Fed.

When the Fed cuts rates, it may be executed over fewer meetings over the next 18-month period than what traders are currently thinking. This means that the US dollar still has some carry for the time being. And not only that, but the fundamentals of the US economy are strong, and remain strong. The US is currently streets ahead of other G10 economies on multiple counts, and that optimism has shown in the US dollar of late. We think that this rhetoric will continue for the time being.

For the Kiwi dollar, higher for longer interest rates may not be such a driver. We see plenty of risk to the Kiwi economy in keeping rates higher for longer…but there is little choice given the lack of clear data points for the RBNZ between now and November. We think that the Kiwi economy may end up somewhat ‘cooked’ by high rates. Unemployment is expected to tick up and GDP forecasts for the remainder of 2024 are less than flash. All of this has to weigh on the Kiwi, even if we cut rates six months behind other major central banks.

Recently we have tested the 0.5950 level, and we see the next rung lower at 0.5910. From there we are looking at the high 0.5800s and ultimately, 0.5700. This is already reflected in the NZDAUD cross, which is trading in similar range ratios, only a cent lower now in the 0.9100 – 0.9200 band.

- Mieneke Perniskie, Kiwibank Trader – Financial Markets

Kiwi crosses in the months ahead

NZDUSD (5-year daily)

Things are getting real and local economic conditions are becoming recognised in the currency. As the anticipated start of Fed easing gets kicked out further and the reality that RBNZ rate cuts will need to come sooner than Q2 2025, price action across the past quarter brings NZDUSD towards significantly key downside levels. The intersecting 0.5900 / 0.5920 triangle support zone and 0.5904 61.8% Fibonacci retracement level will be key to watch in coming weeks. Momentum indicators argue for a period of consolidation or even short retracement of the recent downside move below 60 cents. It is these short rallies of which we have consistently argued and continue to argue that USD buyers take advantage. Until both interest rate differential expectations and the broader economic fundamentals of NZ Inc improve - both seemingly unlikely in the foreseeable future – NZDUSD will remain capped at its current downtrend resistance level circa 0.6250.

Ultimately, it’s the downside risk which is now becoming more and more apparent. A break of the pre-mentioned 0.5910 zone opens up moves to 0.5750/70, and then a re-test of the 55c double bottom would become a reality from this point.

NZDAUD (5-year daily)

The classic Kossie headfake. Calling NZDAUD is a tough task at the best of times, and the break above the long-term channel resistance around 0.9380 in Feb was somewhat of a head scratcher for us. Perhaps driven by optimism of earlier than expected RBA easing, recent economic data prints out of the lucky country will likely see the RBA continue on its rather tortoise-esque strategy – slow, boring but controlled monetary policy path. The RBA was never in a hurry to hike and probably won’t be in a hurry to cut either.

Economic and interest rate fundamentals argue for a lower NZDAUD and now the technical picture is beginning to support that outlook. The false break above 94c and reversal is technically a bearish move, which perhaps has already played out to an oversold level (RSI) from short-term perspective. From this point, a period of consolidation and move back towards 93 cents cannot be ruled out, but ultimately a move back towards 0.9150 initially, and then 0.9030 is the path of least resistance in the coming quarter.

NZDEUR (3-year daily)

An underperforming European economy and anticipated ECB easing from June sees some potential upside performance in NZDEUR in the near term. A muted trend support break out of the recent 6-month shallow-upside channel comes following a period of weakness from 0.5750. An oversold RSI may inhibit further weakness especially if US Dollar driven fundamentals continue to dominate. Continue to expect largely sideways price action between 0.5400 and 0.5750 in the coming quarter.

NZDGBP (3-year daily)

The remaining hawks at the BoE appear to have finally conceded. At the most recent policy meeting in March, all voting members ruled out the need for further rate hikes. In effect, the door for easing the second half of 2024 has been opened. Despite the BoE’s dovish pivot, NZDGBP has largely underperformed over the past quarter. A failure to break back above 0.5000 now provides a clear cap as rate easing cycles of both the BoE and RBNZ comes into alignment. Ultimately, the medium term direction (above 0.5000 or below 0.4630) will be determined by the length and size of forthcoming RBNZ and BoE easing. For now, continue to expect a broader 0.46–0.50 pence range play.

NZDJPY (5-year daily)

History will be told over a period and not a moment of time. Despite the momentous 20bp rate hike at the BoJ’s March meeting along with the abandonment of yield curve control targeting, cautious commentary from BoJ members – “don’t expect further imminent tightening” – largely saw a muted financial markets reaction – an outcome that perhaps BoJ officials were trying to construct in the near term. With most major G10 currencies still yielding 300-500bps of positive carry over the JPY, significant moves lower in NZDJPY won’t happen overnight. Markets now largely discount further BoJ tightening – reflected in 2 year OIS sitting at 0.3% along with 10 year OIS still trading at a miserly 0.85%. Just like the past 17 years of easy monetary policy in Japan, the next period of monetary tightening could be a long and drawn out affair.

However, any further hawkish surprises in coming months may speed things along in a relative sense. As the RBNZ and other major central banks ease policy settings over the coming year, the negative carry vs G10 currencies will continue to narrow. This should see NZDJPY eventually break lower out of its multi-year up trend channel. A top at 93.45 may have already being formed.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.