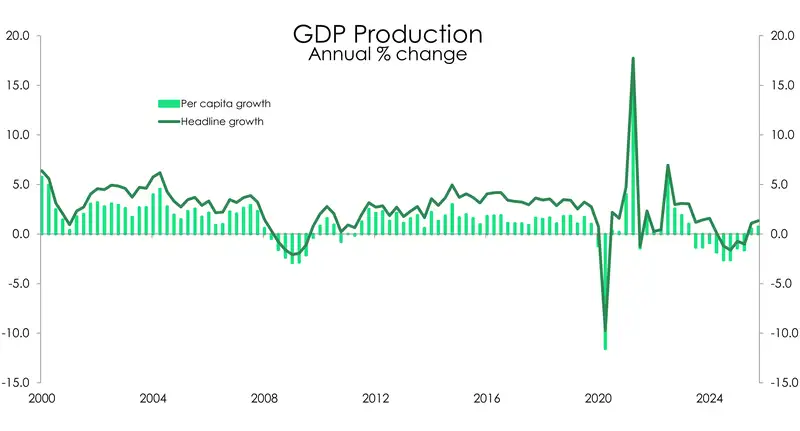

- The Kiwi economy ended 2025 with just a modest lift to growth. Economic activity lifted 0.2% over the December quarter, 1.3% over the year. The economy is simplly softer, and slightly smaller.

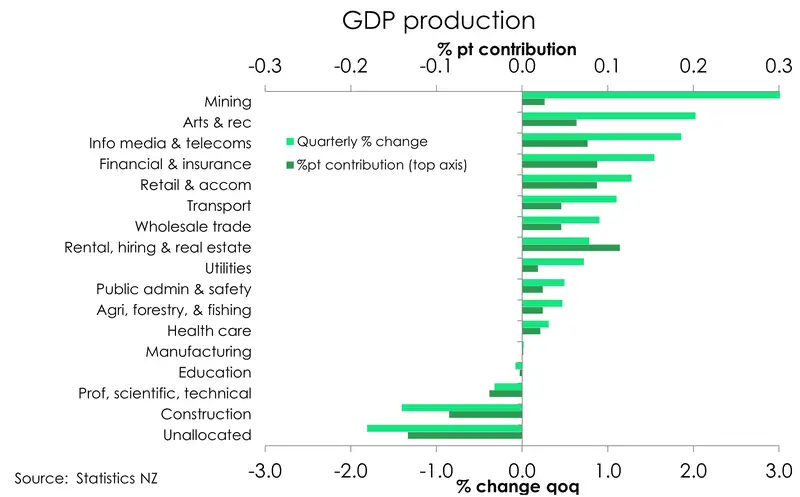

- Most industries saw an increase in output. But most of the strength in today’s report came from industries tied to the tourism sector. We knew that was coming. Just like we knew construction would remain a major drag on activity.

- But that was then, and this is now. And we’re now looking into some fierce headwinds. The escalating conflict in the Middle East, and the resulting lift in oil prices have added significant downside risks to growth (globally). Heightened uncertainty is likely to prompt businesses to pull back, rising fuel costs will further squeeze household budgets, and a global slowdown could weigh heavily on Kiwi exports. Our shining star, tourism, could come under pressure.

Today’s economic report card for the Kiwi economy came in broadly as we expected. Growth was modest, showing some signs of progress. But it was not enough to encourage much hope for uncertain recovery ahead.

Output lifted 0.2% over the December quarter, just shy of our forecasts for a 0.3% lift. Meanwhile, the impressive 1.1% lift in activity originally reported for the September quarter was revised down to a softer 0.9%. From the Reserve Bank’s perspective, the combination of softer‑than‑forecast quarterly growth alongside the revisions to historical data points to a weaker starting point for the overall size of the economy. In effect, the downward revisions leave December’s level of output virtually unchanged from where September was originally estimated. And that matters. A smaller‑than‑assumed economy implies weaker domestic inflation pressures, with the output gap closing more slowly than expected.

Other than that, today’s report card offers us very little new insight. The start of the tourist-heavy summer kicked off strongly. With international arrival numbers at their highest since Covid (97% of pre-covid levels), we saw an impressive 7.8% in our travel export services over the quarter, taking our export service volume well beyond pre-covid levels. And as such sectors tied to the tourism industry led most of the growth throughout the quarter. The rental, hiring, & real estate group led the charge. Though with no help really from the real estate component. The retail trade & accommodation group was also strong. But again, mostly thanks to the accommodation component. It’s nice to see tourism as a shining star. But we are wary of the best bit falling away again. We are wary of the potentially severe impact of the surge in oil prices... and airfares... emanating out of the Middle East. Airlines have slashed flights, and lifted airfares. That does not bode well for tourism. Although we hope we get some tourists wanting to get away from all the madness north of the equator. Somewhat optimistic we know.

On the other side of the ledger, construction continues to be a significant drag on activity, with the stale housing market still struggling to breathe life back into the sector.

Overall, we've managed to produce just 1.3% of growth over 2025, and just 0.7% on a per head (capita) basis. We're still struggling. And that’s before the sharp deterioration in the outlook over the past three weeks given the conflict in the Middle East.

Today’s data is old. It covers the last 3 months of last year... and we're 3 months into this year. So it's more about the starting point (weaker) and momentum into this year (weaker). This is not an economy demanding RBNZ rate hikes to fight off a supply-side shock to oil. The potential damage to demand outweighs the lift in inflation.

Construction drags behind

As expected, the construction sector saw a downturn of 1.4% compared to last quarter, and a 2.4% decrease compared to the same quarter in 2024. The downturn was predicted by a 3.1% decrease in building volume work for the December quarter.

Sentiment in the construction industry also forewarned the numbers, with experts warning that they didn’t expect construction to revive until late 2027 to early 2028. We talked to Dan Hayworth from Box Design & Build in our weekly podcast where he reiterated the point that builders are feeling substantial strain with no easing on the horizon for the next nine months.

Check out the podcast here

A quieter quarter on the expenditure side

On the expenditure side of GDP, we saw a more modest 0.1% lift in activity over the quarter following a (downwardly revised) 0.9% rise in Q3. The strong tourism season continued to play a supportive role, with export services once again doing the heavy lifting and driving that small gain in overall export volumes. In contrast, goods exports acted as a drag with volumes falling 2.6% over the quarter, driven largely by weaker dairy exports/

What stood out most to us, however, was the sizeable pullback in business investment. Gross fixed capital formation dropped 2.2% over the quarter. It’s a disappointing reversal after the solid lift of a similar magnitude that we saw in Q3 and that encouraged us for businesses re‑engaging in growth‑oriented decisions. Unfortunately, this looks more like a correction to the stronger‑than‑usual Q3 result, with investment falling across key categories such as plant and machinery, as well as transport equipment. And now with all the new uncertainty, we would expect business investment to come under pressure again in future months.

On the household side, consumption was essentially flat. Weakness in durables persisted, marking a third consecutive quarter of declines. In the December quarter, households spent 4.3% less on durables, were flat on non‑durables, and lifted spending on services by a modest 0.6%.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.