- We’ve been obsessed (and rightly so) with the conflict in the Middle East. Last week Trump gave Iran a 48-hour ultimatum to open the Strait of Hormuz, which turned into a 5-day negotiation window. The deadline then got extended, again. Now we are waiting for 6 April. We hear of de-escalation, then re-escalation, followed by de-escalation. But the war continues.

- Threats to the supply of diesel brings images of a Mad Max movie. And leaders are concerned. We will adapt and find solutions and reengineer supply chains. But there’s not a lot we can do in the near term, if South Korea decides to limit exports (for example).

- Last week RBNZ Governor, Anna Breman, delivered her speech. We like her messaging – she’s sending strong signals that the RBNZ will not be rushed into reacting to fuel costs and the (temporary?) spike in inflation.

- Beyond our COTW which covers the move (or lack thereof) in exchange rates, we are anxiously watching the diesel stores and hoping that we have enough to keep essential services going.

Last week, news agencies were reporting that peace negotiations were flowing both ways, and markets started reacting positively. But then there’s news that US troops have arrived in the Middle East. Iran is still acting, with attacks raining down on the region. Jordan, Oman, Kwait and Saudi Arabia are all fending off drone and missile attacks. Both sides are saying they won’t back down. The war is continuously winding down and gearing up. The risks to global supply chains are front of mind. Controlling the strait of Hormuz is the focus. It’s a revenue generator for Iran.

On Tuesday last week RBNZ Governor, Anna Breman, delivered a speech outlining the need to wait and assess the effects of the oil crisis on the economy. This will take time, something the rate market needs to adjust for. The RBNZ will keep a sharp eye on the second round effects of inflation (see our commentary on this for more). But it’s not just price changes, it’s also demand destruction.

Our view is un-changed, the Kiwi economy is soft, our labour-market has a lot of slack. For an inflationary spiral to really take hold it would need a lot of grip strength. The Kiwi economy is like wet soap, ready to slip and slide out of core inflation’s grip. RBNZ’s messaging has served to douse some of the wholesale market’s moves to price in hikes for 2026 – we saw a move down. From the market pricing in almost four rate hikes before Breman’s speech, to now only pricing in three. Still far too many in our opinion, but we are getting used to playing the contrarian to the markets.

Last week also saw oil prices bounce around, settling at $104USD per barrel for brent crude before the weekend. News of Trump’s continued negotiations with Iran battled news of the conflict ramping up and other countries beginning fuel rationing. Pessimism is winning out, the price of brent crude up to $114USD on opening this week. We expect that we are nowhere near at the peak of where prices will go.

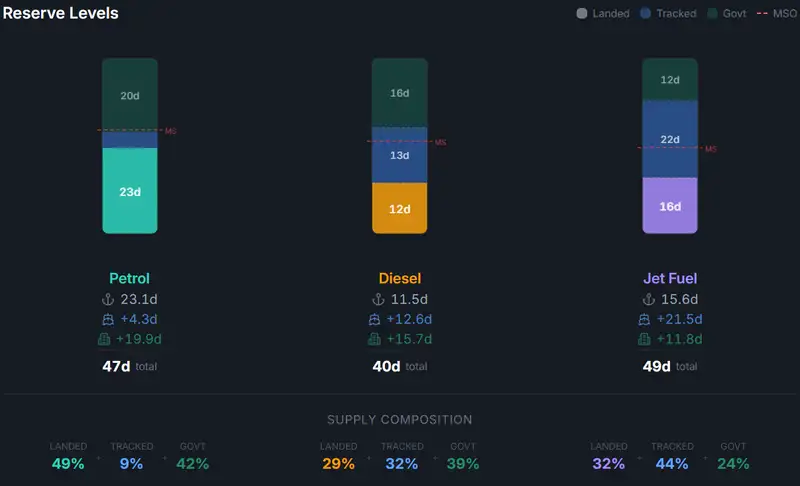

Domestically we are closely watching diesel supply. The economy runs on diesel, from most of our domestic freight, agriculture, rubbish trucks, emergency infrastructure, marine and fishing, construction and mining. We could grind to a halt if we run out of diesel. Without diesel farmers can’t harvest crops, and they can’t deliver milk. And costs are soaring for essential industries. Unlike Covid, where essential services could still run while everything else stood still, we could see a Mad Max style scenario where essential services go out first. Hence, there’s an urgency to get fuel supply and limit demand where possible. More to come.

Source: Fuel Reserve Monitor 30/03/2026

Financial Markets

The comments below were provided by Kiwibank traders. Trader comments may not reflect the view of the research team.

Rates – RBNZ notes patience on policy, but in reality, remains in a bind

A recurring theme of late, the New Zealand IRS market opened the past week higher, with the weekend event and headline-risk associated with the ongoing conflict in the Middle East playing out at the start of the week. In addition to this, we also noted the Fitch ‘outlook negative’ release as well that arrived late ahead of the weekend, where they noted delays in debt decline and fiscal consolidation. The resultant Monday activity saw the IRS curve marked higher with the implied path continuing to bring forward priced RBNZ tightenings, with the May meeting at one point priced as an almost certainty. With the activity resembling a rush towards a small exit, we noted 2-year IRS trading towards 3.70% before settling around 3.67% (+13) with 10-year at 4.555 (+15).

Tuesday, conflict-related headlines indicating a delay in strikes while reported discussions were underway, although denied in some sectors, did provide rates markets with a reason to open lower, with our IRS curve opening around 5.5-points lower in a generally parallel shift. The morning also saw the RBNZ Governor deliver a speech entitled: The impact of the Iran conflict on New Zealand. We had noted in prior weeks that there was the potential for the RBNZ to update the market as to their thinking, particularly as the market had moved to rapidly reprice increased near-term tightenings far beyond those anticipated in the February MPS. In general terms, the speech noted the current environment and set out how the ongoing conflict in the Middle East could impact the outlook for the New Zealand economy. It also provided some insight to their current thinking and how the RBNZ sought to take into account the medium-term aspects of the 1% to 3% CPI band and the balance between potentially higher inflation expectations against that of a potentially weaker growth outlook noting that getting this judgement right was the key to avoiding reacting too early to near-term inflation pressures that monetary policy can do little about. In summary, it was viewed there was a willingness to maintaining a degree of patience until there was greater clarity or confidence of the impacts through the economy. Reaction saw the curve add to initial gains, with the implied OCR path paring back the May meeting tightening probability from fully-priced to around 50:50, with 2-year IRS marked at 3.56% some 10-points lower, 5-year at 4.11% (-9), with10-year at 4.47% (-8). Though as evidence of how far and quickly pricing had moved of late, the implied path still maintained its three-tightening case for 2026. Further de-escalation type headlines and perhaps a further slow-burn reaction to the RBNZ update did see additional gains in swaps on Wednesday, with receiving activity evident, though this activity couldn’t sustain into the end of the week. Comments from the RBA Assistant Governor on Thursday that reiterated the focus on inflation and the desire to avoid a lift in long-term inflationary expectations, and as you would expect, some scepticism around the likelihood of any resolution to the conflict saw the curve finish the week unchanged – 2-year at 3.54% (-), 5-year 4.05% (-), and 10-year at 4.40% (-).

So, does that leave the disconnect between policy and market rates we discussed last week still in play? The RBNZ update may have provided a little support to those prepared to run their calculators through their paces, assessing the gap between short-swaps and cash/bills and the accrual calculation through rate-sets, and can afford a degree of patience, particularly with our implied curve still pricing three 25-point tightenings by year-end. Weekend events too may also support the application of greater scrutiny on the shorter parts of the curve and potential policy outcomes, with the most recent pivot in the US curve perhaps an indication that attention may be shifting past the immediate associated inflationary impacts of the conflict to the broader economic consequences that this action may impart, including further stressing some sector issues, such as private credit markets, that have been simmering. Graham Hughes, Trader – Financial Markets.

In currencies, risk sentiment is starting to drag

Last week we opened with some upside views on how long the Iran war is likely to drag on, and the US dollar index was trading around 99.20. Over the week, the DXY traded slowly but surely higher as risk sentiment continued to drag, closing the week at 100.19. The Kiwi dollar traded in step, opening the week at the key 0.5770 support level, quickly to a high of 0.5880, and then spent the remainder of the week dragging lower, ultimately closing the week sub 0.5770 at 0.5746. We are currently sitting on key support levels, and the outlook for the Iran situation has largely darkened, with the growing likelihood of drawn-out conflict, and crucially control of the Hormuz Straight is the key here. With Brent Crude currently still trading at US114 pb, the more this rises the worse the outlook globally on inflation and growth outcomes. If the Kiwi continues to trade below 0.5770, 0.5710 is the next key level and we may end up in the 0.5600 levels this week. Our view for the Kiwi is that we will head lower as the conflict continues.

The Yen was lower over last week, hitting 160 Yen to the US dollar to close the week, and there was subsequently some rhetoric from Japanese officials on Friday that warn of potential intervention, although the effectiveness of this may be side-lined by global factors. The NZDAUD appears to have found some support, trading between 0.8310-0.8370 last week , with the Aussie dollar underperforming. The Aussie CPI print was slightly softer than anticipated, taking some of the sting of the hawkish RBA outlook. For now the 0.8300/0.8350 levels hold firm. Mieneke Perniskie– Senior Dealer, Financial Markets.

Weekly Calendar

- Domestically the February Building report out Wednesday is expected to paint a grim picture of the construction industry. This is going to give us a very good indication of how the construction industry was fairing right before the oil crisis and subsequent supply chain disruption and cost pressures exploded.

- Offshore, we’re all waiting for Trump's second go at making the 2nd of April a memorable date. With the US's pause on attacks on Iran's major domestic and shipping infrastructure on pause until then. The outcome of any negotiations between the two nations could mark a significant turning point in the conflict.

- Most of the world is releasing their February data, but US trade ban]lances and unemployment will be in the spotlight a the end of the week. Domestic sentiment in the US is turning sour, as more voters taking a negative view of the war with Iran.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.