We’ve been fortunate to enjoy a strong summer of tourism, even if the weather didn’t fully cooperate. Over the December quarter, international visitor arrivals reached 97% of their pre‑Covid levels. And the latest monthly data from Stats NZ showed the same proportion in January. It’s the closest we’ve been to full strength post-Covid. And we’re expecting to see tourism spread across transport, arts & recreation, retail trade, and accommodation, with strong contributions to growth in this weeks GDP report.

The return to full strength has been a long time coming. That said, the initial rebound in arrivals straight after Covid was much stronger than anyone expected. Looking back, we still remember the wave of commentary warning the tourism sector might never recover. But in the end, it turned out all we had to do was reopen our borders. Tourists came flooding back. Arrivals sharply jumped to around 80% of pre-covid levels in no time at all.

Since then, we’ve hovered in the 80-90% range, slowly edging higher. A stronger return of US tourists has helped. But we’re still notably short on Chinese tourists. They’re the missing piece in the puzzle. For China, the soft post-covid economy, has meant weaker outbound travel demand.

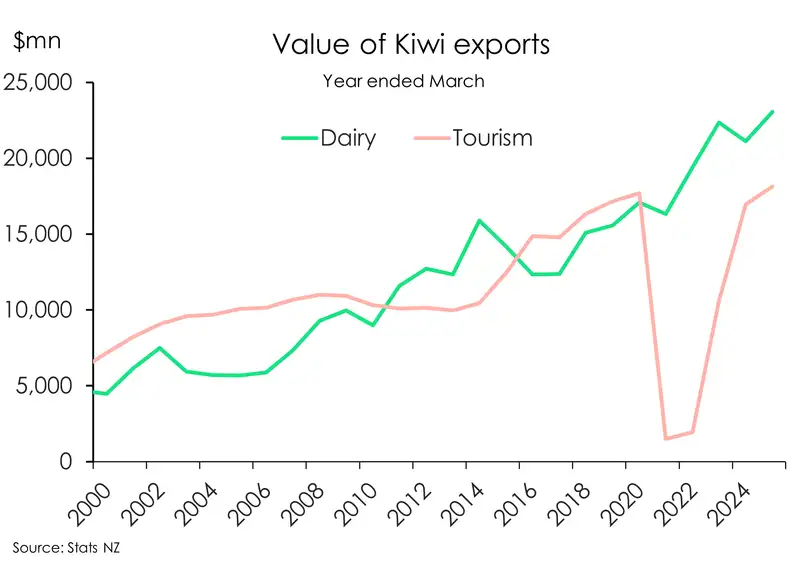

It’s worth emphasising just how important a tourism recovery is. People often forget that for most of our history, tourism, not dairy, has been our largest export. People naturally think about the physical goods we ship offshore. But tourism has long battled dairy for the top spot. Covid changed that. With borders shut, dairy surged ahead and remains well in front today thanks to strong global demand over the past year. Today there’s still a sizeable gap between the two industries, and it may be some time before tourism retakes the crown.

Frustratingly, the war in the Middle East adds fresh risks to the outlook. All our export industries are exposed to a global slowdown. But tourism is especially vulnerable to spikes in oil prices. More expensive fuel means more expensive flights, or simply fewer of them. We’ve already seen signs of this. Last week Air NZ cut 1,100 routes in response to the sharp rise in jet fuel prices. And if the conflict drags on and oil stays elevated, we’ll see more of the same. That could affect future tourist arrivals. Such a tourism shock poses big risks for our regional economies. Hopefully it doesn’t get to that.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.