Shipping traffic remains at a standstill at one of the world’s most strategically important oil choke points. Around a fifth of the worlds global oil and liquified gas passes through the narrow body of water between the Persian Gulf and Gulf of Oman, known as the Strait of Hormuz. And amid the escalating Middle Eastern conflict, passage across the strait has essentially come to a halt.

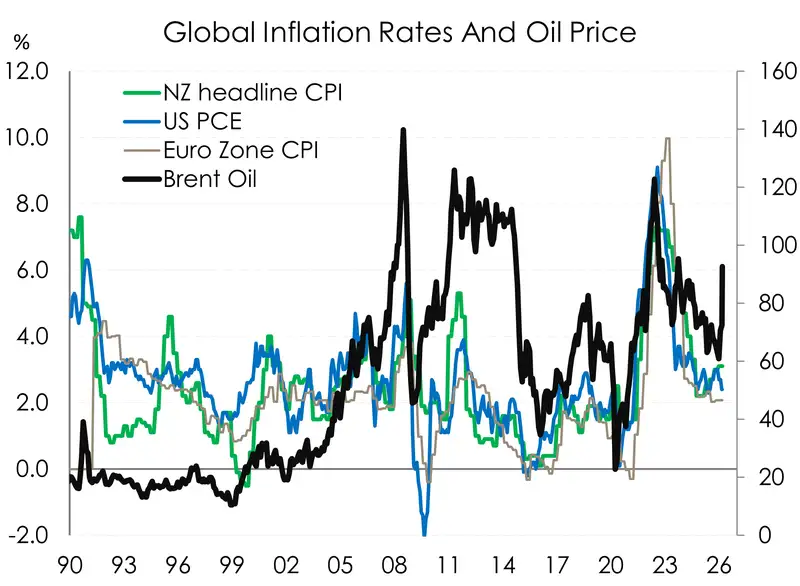

In response, oil prices have pushed higher, to no surprise. Brent Crude finished the week at $92.69 USD per barrel, jumping nearly 30% over the past week alone. Even so, the move was a touch slower than we might have expected. For most of the week, prices chopped around in the $80–$85 USD range—certainly higher than the low‑$70s we were trading at before the conflict, but still not particularly high in the context of broader oil market history.

But as the conflict has dragged on, we’ve seen a series of supply‑side pressures emerge. The UAE, Kuwait, and Iraq have begun reducing production due to storage constraints. And China has halted oil exports… fuelling the push higher in the Brent Crude price.

And unfortunately, we don’t think it’s over yet. Things are likely to get worse before they get better. A move above $100 USD, and potentially into the $115–$120 USD range, similar to the levels reached during the Russia‑Ukraine crisis, looks increasingly plausible in the coming weeks. Our hope is that, as with 2022, prices retreat quickly once tensions ease.

For now though, it's going to hurt households at the pump. And to add to that inflation pressure, the Kiwi dollar has softened. The NZD has slipped from the high‑59s/low‑60s into the mid‑58s to mid‑59s. It’s not a dramatic fall, but with oil moving the way it has, every cent counts.

Beyond oil prices, attention will also turn to what happens with shipping costs. Because higher oil prices is one thing, but we’re also likely to see supply‑chain pressures build from rising shipping insurance premiums, longer transit routes as vessels avoid the conflict zone, and broader delays as global logistics networks adjust. That’s where we’ll feel a second‑round bite of pain.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.