Finally, a dovish tone. The RBNZ’s inflation forecasts and OCR track were lowered. Thoughts of rate hikes have all-but evaporated. And our call for a cut in November looks a little closer today. Traders agree.

Actually, traders are gearing up for two cuts by November, currently 5%, down from 5.25%. So there’s a chance of a cut being put (back) into August. As expected, the on-hold decision caused a sharp drop in wholesale interest rates, with wrong-footed bets on hikes forcefully reversed.

This is good news for Kiwi businesses and households.

“Do we hold, or do we do more? We held… It is a soft landing scenario” Adrian Orr, RBNZ Governor

Monetary policy is working

After a 3-month break, the RBNZ have come back to the drawing board and concluded: Monetary policy is working.

If we start offshore, central banks around the globe have done enough, by hike interest rates, to stifle growth and strange inflation. Global growth is below trend, and our trading partner growth is expected to slow further this year. The RBNZ sees downside risks to the global growth outlook. That points to softening commodity prices. And we’re a commodity exporter. Without a fall in our currency, our exporters may face another awkward year. The inflationary impulse reaching our shores is simply softer, with deflation in China, our largest trading partner. Yes, shipping costs have spiked with the skirmishes in the Red Sea. It will feed through (somewhere between 0.3-to-0.7% according to RBNZ). And these added costs, and time, will impact the bottom lines of exporter and importers. Offshore, all of the focus is around central banks, especially the Fed, cutting rates this year. They have done enough, and will need to cut rates in order to achieve anything close to a soft landing.

Locally, the RBNZ’s comments around migration and the labour market were key. Signs of a slowdown in economic activity are abundant. Whether it’s retail sales, construction, or manufacturing, tighter financial conditions are weighing on activity.

Household consumption is weak and business activity is subdued.

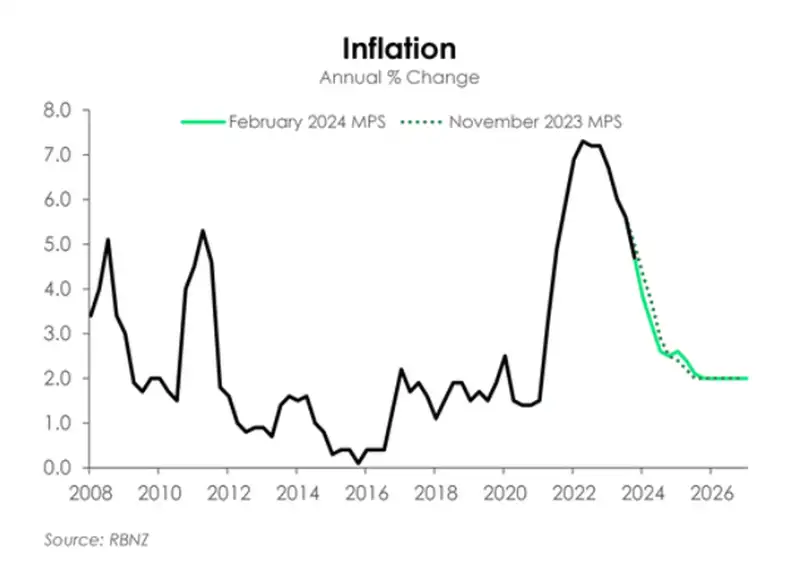

The RBNZ’s new forecasts were little changed and continue to paint a soft economy, continued rise in unemployment, and a (slightly) faster return to the RBNZ’s 1-3% inflation target band. The restrictive monetary policy settings is having the intended impact. The need for further pain is unwarranted.

The Kiwi economy is weak, at present. Economic growth is expected to have been flat in the final quarter of last year. And looking beyond, we’re in for a few more quarters of rather subdued growth. Restrictive interest rates and below-trend global growth is weighing on demand in the economy.

Rapid population is supporting aggregate output, and remains an upside to the economic and inflation outlook. The demand impact of strong migration is emerging in the form of rising rents. And retail sales volumes would be weaker still if not for population growth.

However, the supply-side impact of migration is being greater felt. With high migration and weaker demand growth, capacity constraints in the labour market have eased, and will continue easing. The unemployment rate may have increased by less than the RBNZ had expected, but wage inflation has been more subdued. It’s clear evidence that slack is building in the market. A softening in wage inflation is key in driving a continued slowdown in domestic inflation. Unemployment is still expected to rise, hitting a peak of 5.1% by the second half of this year.

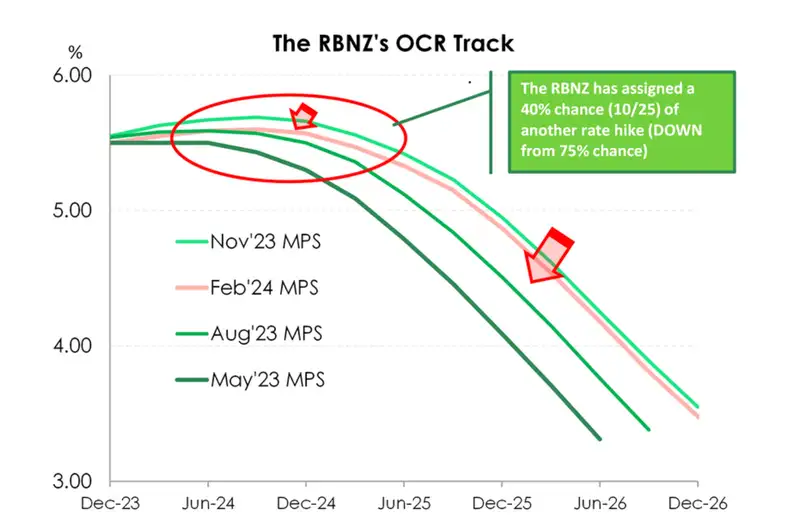

Encouragingly, the RBNZ’s near-term inflation forecasts were revised lower. It follows a series of significant downside surprises to the RBNZ’s expectations. Compared to the November MPS, a slightly faster return to the RBNZ’s 1-3% target band is expected. Inflation is forecast to hit 3.2% by the middle of year, down from 3.7% estimate. But they aren’t letting their guard down just yet. With only a gradual loosening in the labour market to date and sticky domestic price pressures, the RBNZ is maintaining a hawkish front. The OCR track still signals a bias toward further tightening near-term. The RBNZ requires more evidence – specifically inflation prints – before we will see them pivot. But the pivot is coming. And expectations are shifting. Expectations for the OCR this time next year have fallen from 5.56% to 5.47%. We’ve moved from chances of hikes to chances of cuts.

In a slight surprise, the RBNZ also lowered their near-term house price forecast. Previously expecting gains of around 5% by late this year, the RBNZ now doesn’t see these gains until mid-2025. Record high net migration continues to add additional demand to the housing market. But the RBNZ’s mind is on the lagged impact of monetary policy tightening which continues to wash through the economy.

Despite some minor falls in lending rates, mortgage rates remain high and dry, weighing heavily on the housing market. In the medium term (the two-year sweet spot) however, a lagged impact of high net migration and lower interest rates has the RBNZ seeing house price growth of around 6% per year. We in comparison see house price gains of about 6% in 2024.

Blue blood on the trading floor

Leading into today’s announcement, the pivotal 2-year swap rate was trading at 5.21%. That rate was poleaxed to 5.0%, a full 21bps lower. That’s a big move. Blue blooded traders were stopped, and the market ran in the other direction. Before the announcement, the OIS strip had 7bps (5.57%), 30% chance of a hike, priced in for today. Further out, the May meeting had 15bps (5.65%), 60% chance of a hike. The first full 25bp cut was priced for November (5.25%). There was 100bps of cuts priced to the middle of next year (4.5%). NOW, the May meeting has 4bps (down from 15bps), and there are TWO full cuts priced by November, at 5.01%. As we saw in December, the market is now pricing in more cuts than we expect.

The Kiwi currency was at 0.618 against the greenback and 0.943 against the Aussie. We saw some frenzied trading for a bit, as the Kiwi fell against the greenback to 0.6108 and down to 0.9365 against the Aussie. We expect the Fed to cut before the RBNZ, and the RBA may sneak in before the RBNZ also. So the outlook for the Kiwi is still mildly supportive near term, but we expect bigger falls later in the year. We’re picking 0.57c against the greenback.

Special Topic: Shipping costs as short-term risk

Behind the usual number one question of ‘where are interest rates going?’, our year commenced with a number of questions on what the Red Sea attacks meant for the inflation outlook and the economy. Unsurprisingly the RBNZ have also asked themselves that same question and had a closer look to the potential impacts. Not differing from our own view, the red sea attacks are just another inflationary headache. A further set back in the near term. But less so in the medium term. And that’s what monetary policy is about. Focusing on the medium term and looking through relative price and supply shocks. So, as it stands the red sea attacks has little-to-no impact on the OCR and its projections.

Nonetheless, as the RBNZ has rightly pointed out, the Houthi attacks on ships in the red sea is an issue to remain vigilante of. Since the attacks started, delivery times have lengthened, and shipping costs have spiked. According to Veson Nautical, it takes an extra ~9 days at sea to avoid using the Red Sea and Suez Canal and chugging around Africa. Or as the RBNZ points increasing journey times by around extra 30 to 50 percent. Already a number of shipping freight indices have doubled. And according to the RB’s research, a sustained doubling in shipping costs could add about 0.3 to 0.7 percentage points to annual inflation over a 12-month period. It’s an unwelcome spike to the inflation outlook, but still a long way from the same sort of shipping spikes during the covid period.

RBNZ statement

“The Monetary Policy Committee today agreed to hold the Official Cash Rate (OCR) at 5.50%.

Over the past year or so, the New Zealand economy has evolved broadly as anticipated by the Committee. Core inflation and most measures of inflation expectations have declined, and the risks to the inflation outlook have become more balanced. However, headline inflation remains above the 1 to 3 percent target band, limiting the Committee’s ability to tolerate upside inflation surprises.

Restrictive monetary policy and lower global growth have contributed to aggregate demand slowing to better match the supply capacity of the New Zealand economy. With high immigration and weaker demand growth, capacity constraints in the New Zealand labour market have eased.

However, recent high population growth is supporting aggregate spending, as evident in upward pressure on dwelling rents, for example. Internationally, global economic growth remains below trend and is expected to slow further during 2024. This subdued environment will support a further moderation in New Zealand’s import price inflation.

The outlook for the China economy remains particularly weak relative to recent historical norms, with structural factors constraining longterm growth. A more general risk to global growth is that central banks may need to keep policy interest rates at restrictive levels for longer than currently reflected by financial market pricing, to ensure that inflation targets are met.

Heightened geopolitical and climate conditions remain a risk for inflation. The recent rise in global shipping costs is one manifestation of these risks. The Committee remains alert to these relative cost pressures and will act to limit spillovers into general inflation if necessary.

The Committee remains confident that the current level of the OCR is restricting demand. However, a sustained decline in capacity pressures in the New Zealand economy is required to ensure that headline inflation returns to the 1 to 3 percent target. The OCR needs to remain at a restrictive level for a sustained period of time to ensure this occurs.”

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.