- Business confidence deteriorated in the June quarter. High interest rates are weighing on demand, with more businesses seeing a decline in trading activity. Weak-to-miserable growth remains the outlook.

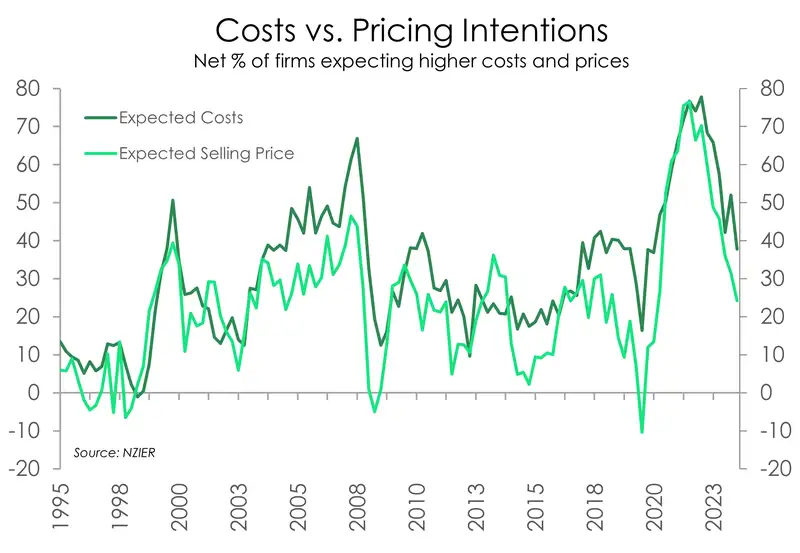

- The most important read in the report involves pricing. And it was all-round good news. Cost expectations have eased, and pricing intentions have softened.

- The most striking read was the deterioration in labour demand. The same proportion of firms as during the GFC are now cutting headcount. And more look to do the same in the coming months.

- The QSBO adds further support for our call for RBNZ rate cuts sooner rather than later. We’re sticking to our call for cuts to begin in November.

The NZIER’s quarterly survey of business opinion (QSBO), the best on the street, shows a clear deterioration in expectations. That’s not good. And business intentions point to a continuation of the weak-to-miserable economic data. We’re not yet out of recession. The QSBO supports our (unfortunate) forecast for another contraction in the second quarter. And we’re likely to record either more contractions or miserable growth for the rest of the year. The report adds further support for our call for RBNZ rate cuts sooner rather than later. Let’s go for November rather than February… with the RBNZ’s call for late 2025, twelve-to-twenty four months too long.

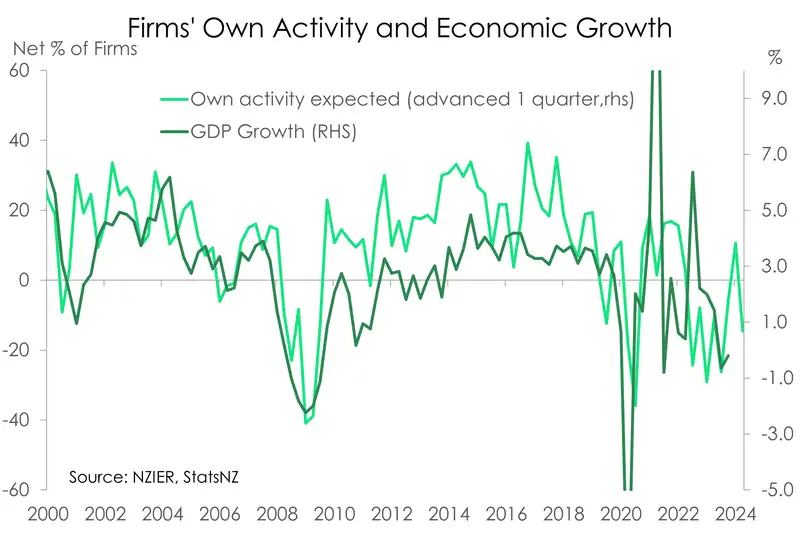

In the June quarter, a (seasonally adjusted) net 35% of businesses expect economic conditions to deteriorate in the coming months – much worse than the net 25% in the prior quarter. According to Kiwi businesses, navigating the current economic environment is still a challenge. The mood among firms remains downbeat as activity indicators deteriorate. A net 28% of firms reported a decline in trading activity. With activity still running below the long-run average, below trend growth remains the outlook.

The most important read in the report involves pricing. Cost pressures and pricing intentions improved substantially. A net 42% of firms experienced higher costs, far fewer than the net 70% last year. The improvement is feeding through into pricing. A net 23% of firms raised prices over the quarter – the lowest since March 2021. It’s great news for the inflation outlook. What’s even better is the shrinking proportion of firms looking to increase prices over the coming quarter – from a net 33% to a net 23%.

With weaker demand, capacity pressures continue to ease. Capacity utilisation – a measure of the intensity with which firms are using their resources – has markedly declined over the past year, after reaching record-highs in 2022. More firms are also reporting the ease in finding labour. Whether it’s unskilled or skilled labour, firms are no longer having to scrape the barrel. We’ve seen a rapid return of migrants, and their impact on the economy is clearly felt.

A deterioration in labour demand (as supply increases) was crystal clear. Increasing supply alongside decreasing demand, reduces the price. And the price is wages. There has been a clear mindset shift among business – from increasing headcount, to cutting headcount. A net 25% of firms reduced their workforce over the quarter, a big increase from last quarter’s net 11%. And a net 10% of firms are looking to do the same in the coming months. These are ugly numbers, reminiscent of the 2008-09 GFC.

Both the improvement in capacity utilisation and labour availability point to a considerable easing in capacity pressures in the economy. That’s good news for domestic inflation. A capacity-constrained economy for the last three years created a breeding ground for inflation. But the narrative is shifting. And as capacity pressures ease, downside risks to domestic inflation are building. The steep rise in interest rates is squeezing household incomes, and demand is slowing. Since the beginning of 2023, sales have eclipsed labour as the main constraint for businesses. And a year later, even more firms are experiencing the same. Of the firms surveyed, a clear majority (61%) reported sales as their top constraint.

A further deterioration in activity indicators reminds us that we’re not out of the woods yet. A net 25% of firms reported a decline in trading activity, up from 23% last quarter. Given the clear correlation between trading activity and growth, the economy seems to be shaping up for another contraction in the June quarter. Looking ahead, the outlook is not much better, hence our downgraded growth forecasts. As pointed out in our latest outlook note “Survive ‘til 25: it’s a white-knuckle ride” we now see the economy growing just 0.1% this year. That’s well below the long-term average of 2.5%. The RBNZ has the economy in a chokehold, and the pulse will only strengthen once rates are reduced.

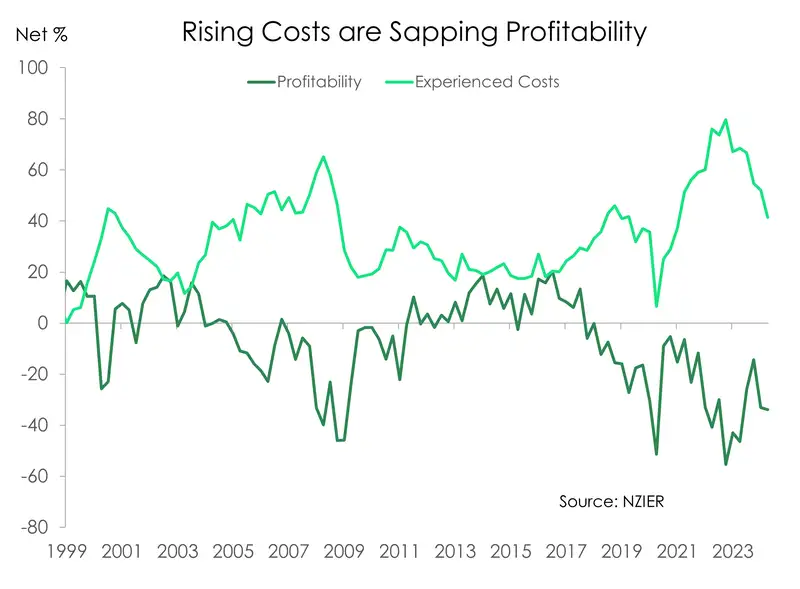

The ”good news” in the report was the fall in experienced ‘costs’. The inflation dragon has been slain, we’re just waiting for it to hit the turf. This is good news for businesses, who have had to deal with rapid inflation in parts. High inflation, coupled with weakening demand, has hurt profitability. And it appears ‘profitability’ is not looking too good. It’s hard to invest for future growth when your profitability is in decline.

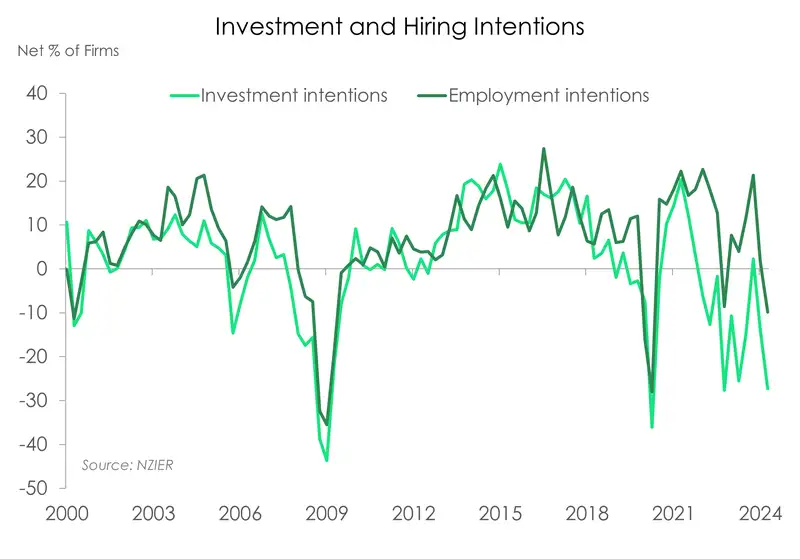

When businesses stop investing for the future, that kills growth. When businesses tell us they’re unwilling to invest in more staff, equipment, buildings and all that good stuff that generates growth, well, we take a red pen to our forecasts. Yes, the RBNZ’s actions are designed to rein in business intentions, from the rapid rebound out of Covid. But enough is enough. The risk here is severe economic scarring, from overly restrictive monetary policy.

Fewer firms reported increased costs and raised prices over the quarter. A net 42% of firms experienced higher costs, far fewer than the net 49% of firms last quarter and net 70% last year. The improvement is feeding through to an easing in pricing. A net 23% of firms raised prices over the quarter – down from the last print of a net 35%. That’s the lowest since March 2021. And looking ahead, the proportion of firms expecting to raise prices is also shrinking.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.