- Earlier today the RBNZ’s Monetary Policy Committee once again delivered a predictable and welcome hold “with full consensus” on the OCR. With the 2.25% OCR staying put for the next six weeks, all eyes will be on the Middle East and the worsening fuel crisis. Weighing up the pros and cons of any future moves, the RBNZ is showing both hawk or dove feather in our view.

- But weeks feel like an eternity when the war in the Middle East wages on and oil prices are creeping higher and lower and higher again. Price is only the first and glancing blow to our economy compared to the true knock out punch that would come from a domestic shortage. Especially of diesel.

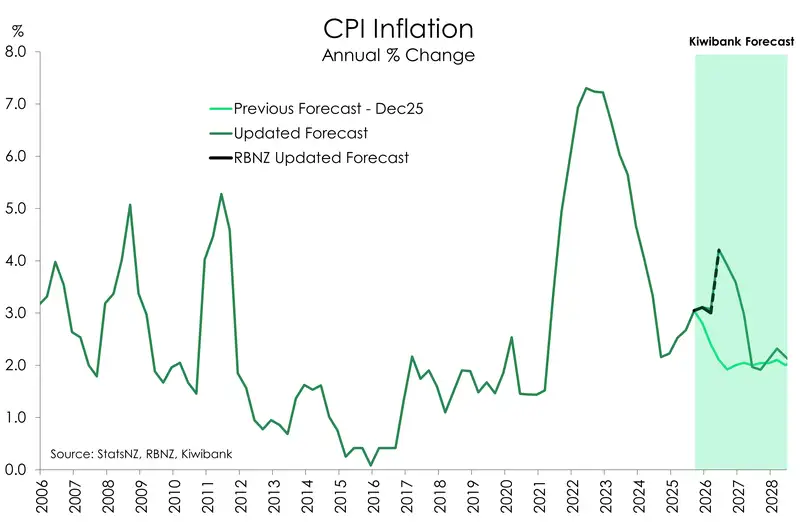

- In our view, any rise in the costs of essentials will feed into inflation growth in the short term, but cost increases in non-essentials will push demand down and put down-ward pressure on growth. In short, the inflation pressures from essentials is another kick in the guts to Kiwi businesses and consumers already weighted down by cost-of-living pressures.

The RBNZ has once again delivered a predictable and welcome hold “with full consensus” on the OCR. With the 2.25% OCR staying put for the next six weeks, all eyes will be on the Middle East and the worsening fuel crisis. Weighing up the pros and cons of any future moves, the RBNZ is showing both hawk or dove feather in our view. They don’t feel pressured to pick a move too early, and we agree.

We expected this ice-cold hold as Governor Anna Breman foreshadowed two weeks ago in her speech to the Business NZ CEO Forum. But two weeks is an eternity when the war in the Middle East wages on and oil prices are creeping higher and lower and higher again. Price is only the first and glancing blow to our economy compared to the true knock out punch that would come from a domestic shortage. Especially of diesel.

Take Covid and flip it on its head. The Kiwi economy runs low on diesel, our emergency services and key industries would be the first to shut down. If you’re fuelling up your regular petrol car and feeling bad for yourself (fair enough, same here), spare a thought for Kiwi farmers and logistics operators. The price of Unleaded 91 is up 25% in the last 28 days (according to gaspy), that hurts, but it doesn’t even hold a candle to the 64% increase in the cost of Diesel over the same period.

Already we are seeing some changes in behaviour from consumers. The Ministry of Transport has released data on public transport use, up almost 6% overall. Light vehicle use down 5-10% across the country. Commercial traffic is also down over 21% compared to before the war.

In their MPR today, the RBNZ showed a keen understanding of the downside risks. The increases in the price of fuel acts as a tax on consumers and suppliers, decreasing demand and spending on non-essentials. The cost of fuel, especially diesel, feeds into the costs of production of our primary industries and shipping and logistics of all goods around the country. There are also impacts on non-fuel oil by-products including plastic packaging and fertiliser, which feed into export and shipping costs as well as directly into the costs for our agriculture sector.

Our two biggest exports, and largest contributors to GDP growth in Q4 of 2025, dairy and tourism, are specifically vulnerable to the disruptions and downside pressures from increased fuel costs (especially diesel and jet fuel), shipping disruptions, and negative shocks to global growth.

Where possible, suppliers will be looking to pass on increased costs. We are already hearing from customers in the B2B sector who are passing on costs or seeing costs rise sharply. Given the soft position of the economy going into this crisis and the slack in the labour market, businesses will struggle to pass on higher costs to end-consumers. And the RBNZ is weighing this risk up carefully. In our view, any rise in the costs of essentials will feed into inflation growth in the short term, but cost increases in non-essentials will push demand down and put down-ward pressure on growth. In short, the inflation pressures from essentials is another kick in the guts to Kiwi businesses and consumers already weighted down by cost-of-living pressures.

We see little risk of inflation becoming imbedded in the economy through wages. This is largely due to the high unemployment rate, keeping downward pressure on wage growth. This is one of the key things the RBNZ will be keeping a close eye on in the coming weeks and months. If they see prices beginning to spiral up, they have warned that an increase in the OCR will likely follow.

Risk appetite is also heavily negatively impacted by geopolitical uncertainty. We are expecting a pull-back in business spending on non-essentials and we are already getting data on consumer confidence beginning to free-fall. This adds more downward pressure on demand and therefore growth. We are seeing demand destruction play out and any path to recovery will depend on oil supply being restored to pre-conflict levels.

View from the trading floor

In currencies, markets take a (potentially short term) risk on view:

The Kiwi dollar was trading around 0.5730 this morning, after a low of 0.5690 overnight in anticipation of a potentially volatile day in the lead up to Trump’s Iran ‘deadline’ at 12pm. The announcement around 10:30am that Trump had announced a two-week ceasefire with Iran, saw the Kiwi rapidly ascend to a high of 0.5819. For now, financial markets may remain somewhat appeased, with oil prices down ~15% and US Treasuries rallied with the US 10YR note down 4bp. Kiwi swaps have also reacted, with 2Y -5Y down 7-8bp. In the lead up to the RBNZ’s MPR the Kiwi held onto the 0.5805 level. NZDAUD was relatively unmoved with both AUD and NZD trading fairly instep against the Greenback, with the cross at 0.8220 (current time of writing sees intraday range of 0.8192-0.8231).

The MPR at 2pm saw the RBNZ leave the OCR on hold at 2.25%, a surprise to no-one. The full statement was very balanced; while the MPC are very wary of the impacts of the current conflict’s impacts on medium term inflation, the key takeaway for me was this statement: "The Committee’s decision to hold the OCR balances the potential benefits of responding pre-emptively to the risk of higher medium-term inflation against the cost of unnecessarily stifling the economic recovery". They do not want to take pre-emptive action that may not yet be required (fingers crossed). The Kiwi did slip and slide following the statement as market participants absorbed this detail against the backdrop of the ceasefire. Ultimately the 2-week ceasefire has some heavy caveats on the Strait of Hormuz opening, and missiles continued to be launched. However, for now financial markets have taken this as a time to pause and let the positive sentiment run for now. From here provided no further escalation, I see the Kiwi on an upward trajectory to 0.5850/0.5900 in the first instance. NZDAUD I’m tentatively positive that we see 0.8300 again. I see CFTC positioning, and potential unwinds combined with Aussie exposure to fuel supply issues providing a floor for the cross in the short term.

Mieneke Perniskie– Senior Dealer, Financial Markets.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.